While we are confused about making a life decision, what our elders usually say is “It’s better to bag some advice from the experts”.

But that reminds me of one of the famous Warren Buffett’s ‘advice on taking advice’ –

“Never ask a barber if you need a hair cut”.

Isn’t it obvious? If you ask a barber whether you need a hair cut. Almost every barber would say “Of course yes, a little cut with my scissors would make you look like Shahrukh Khan” even if you have a 2 week shaved head.

Just like that, if you think you need insurance, don’t ask an insurance agent or a bank relationship manager which insurance plan should you choose.

That being said, if you speak to a few insurance agents or the Relationship Manager of your Bank about taking a life insurance policy, you could easily find a pattern. Almost all the insurance agents and even your Relationship manager would try to convince you to choose a policy with a longer-term period, and high premium insurance plans (endowment policies and ULIPs). Also, your bank relationship manager would insist you choose an endowment plan or ULIP because that type of insurance is also an investment!! Now you would wonder why all these insurance agents are trying to manipulate you to go with only some specific

That being said, if you speak to a few insurance agents or the Relationship Manager of your Bank about taking a life insurance policy, you could easily find a pattern. Almost all the insurance agents and even your Relationship manager would try to convince you to choose a policy with a longer-term period, and high premium insurance plans (endowment policies and ULIPs). Also, your bank relationship manager would insist you choose an endowment plan or ULIP because that type of insurance is also an investment!! Now you would wonder why all these insurance agents are trying to manipulate you to go with only some specific(investment plans and long term period) type of plans. Is it because that, these plans could really bring you fortune?? I hope you are not that absurd to believe it!

Table of content:

1) Why does your Relationship Manager want you to choose Investment cum Insurance Policies?

2) How much commission is earned by Insurance agents & Relationship managers?

3) Relationship managers’ justification to sell Insurance Investment plans

4) Why should you avoid Traditional and ULIP plans?

5) Final verdict

Why does your Relationship Manager want you to choose Investment cum Insurance Policies?

Insurance agents are the salesmen of an Insurance Company. As you know, their job is to sell the insurance policies of an Insurance company. They do not get a regular salary. Insurance agents are paid with a percentage of commission for the policies they sell. So obviously he will try to sell a product that earns a big commission to him; not the one that is beneficial to you.

A bank Relationship Manager is assigned by the bank to a customer who has comparatively more money. Your bank would’ve told that a relationship manager is supposed to help you and give advice regarding your finances anytime. But a relationship manager is merely a salesman in the bank, whose job is to sell the services available in a bank to the existing valuable bank customers like you.

Unlike insurance agents, a bank relationship manager receives the regular salary, but they have to earn the commission which is at least 5-times of his regular salary. For example, for the relationship manager to get the salary of Rs.1,00,000, he is supposed to sell the banking products and services worth the commission of Rs.5,00,000!!

A bank offers only a limited category of financial products like Mutual Fund Investments, Insurance plans, and Investment Insurance plans. Mostly a Relationship Manager would not pitch a Mutual Fund since the percentage of commission of a relationship manager will be merely in the range of 0.5%-1%, due to SEBI’s strong regulations. For example, let’s take 0.5% as the percentage on commission earned by a relationship manager on selling each Mutual Fund value. It means, to achieve the sales commission target of Rs.5,00,000, relationship manager has to sell,

5,00,000/0.5×100 = 10,00,00,000; that is, 10 crores (or 100 Million) value of Mutual Funds.

In other words, he will get his salary of Rs.1 Lacs; only if he sells 10 crores value of Mutual Funds. A pretty laborious task, right?

Therefore, relationship managers or insurance agents look after the policies, which causes them to earn higher commissions per sale. This problem is solved by Investment-cum-insurance policies, where the percentage per sale is 15%-35% depending on the duration of the policy. Now let’s retake the previous example, the commission percentage for Relationship manager now is 35%; so to achieve the same sales commission target of Rs. 5,00,000, now he has to sell,

5,00,000/35×100 = 14,28,572; that is, approximately 14.3 Lacs premiums from ULIPs, endowment plan or some money back policies; it is quite achievable for them.

So, have you noticed the reason – why they pick expensive and unworthy Insurance cum Investment schemes like Endowment insurance policies, Money-back plans, and ULIPs? It gives a bulk sum of commission to themselves and a good profit to the banks, as well.

An insurance agent tries to sell expensive insurance investment plans to get a higher commission. A Relationship manager works in a slightly different way, he gets his salary from the bank, which depends on the policies he has successfully sold to the customers! The customer (investor in insurance cum investment policies) simply becomes a victim of a relationship manager who is sincere in achieving his assigned target. However, the customer will come to know that he is been mis-sold at one point, and by then the relationship manager would have jumped to a different bank to focus on a different group of customers to achieve his given target.

How much commission is earned by Insurance Agents & Relationship Managers?

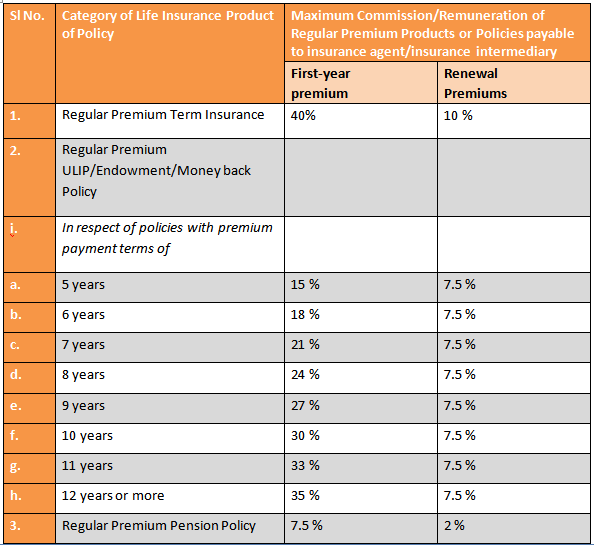

The commission percentage through the policies sold by the insurance agents and relationship manager depends on the type of policy (term, endowment, money-back, and ULIP), the overall duration of the policy, and method of payment (single premium/regular premium). If you choose a cheap and best term life insurance plan the commission will be lower, if you choose an expensive endowment plan then the commission will be much higher. Likewise, the commission for a longer-term period plan will also be higher. The commission earned by insurance agents is regulated by IRDAI (Insurance Regulatory and Development Authority of India). It draws the maximum margin for the percentage of commission that an insurance agent can get on selling an insurance plan.

I. Single-Premium

II. Regular Premium

The commission percentage to brokers given in the above table is the latest. This clearly shows that if you go with a longer-term period policy, mis-sold by your insurance broker or relationship manager, it would get a higher commission for them or their bank.

The commission percentage to brokers given in the above table is the latest. This clearly shows that if you go with a longer-term period policy, mis-sold by your insurance broker or relationship manager, it would get a higher commission for them or their bank.

I hope now you have got an idea of why insurance agents pester you to go with long term period insurance policies. It would be easier to understand how much commission an insurance agent exactly earns with an example. Let’s see one.

Example:

Let’s take a recently launched endowment plan like HDFC LIFE SANCHAY PLUS ENDOWMENT scheme (reviewed here) for example. If you choose this endowment plan with an Annual Premium of ₹ 1,00,000 for a term period of 15 years, it will give you a life cover of ₹ 15,00,000 or maturity benefit of around ₹ 22 Lakh.

The commission earned through the policies sold by your bank relationship manager or insurance agent if you choose this endowment plans is given below,

The commission earned through the policies sold by your relationship manager/insurance agent, if you choose a ULIP plan like the latest ICICI PRUDENTIAL SIGNATURE ULIP scheme (reviewed here) is calculated here. A high Annual Premium of ₹ 2,50,000 for a long term period of 20 years, will get you a life cover of ₹ 50 Lakh or maturity benefit of around ₹ 1 Crore. This plan gives a commission as per the policies sold by your relationship manager or insurance agent with the yearly breakdown of the commission, as shown below;

The commission earned through the policies sold by your relationship manager/insurance agent, if you choose a ULIP plan like the latest ICICI PRUDENTIAL SIGNATURE ULIP scheme (reviewed here) is calculated here. A high Annual Premium of ₹ 2,50,000 for a long term period of 20 years, will get you a life cover of ₹ 50 Lakh or maturity benefit of around ₹ 1 Crore. This plan gives a commission as per the policies sold by your relationship manager or insurance agent with the yearly breakdown of the commission, as shown below;

This huge sum of commission is the main reason for your relationship manager to pester you to go with an endowment or ULIP plan which is called an insurance cum investment plan or investment insurance.

This huge sum of commission is the main reason for your relationship manager to pester you to go with an endowment or ULIP plan which is called an insurance cum investment plan or investment insurance.

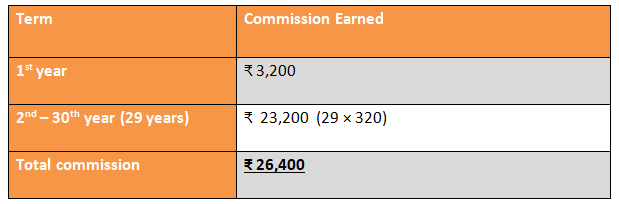

Whereas, if you choose to buy a pure life insurance product like Term Life Insurance plan with a low annual premium of ₹ 8,000 for 30 years, it can give a life cover of ₹ 1 Crore to your family. Which is comparatively a much better deal when compared to any ULIP, where you have to pay the huge sum in order to get the same life cover benefits.

Also, have a look at the hefty commission earned by the Insurance agents or Relationship managers by selling a ULIP product; it is Rs.4,43,250, as discussed above.

Whereas, notice the commissions earned by insurance agents for selling Term Insurance plans, as given below.

So, have a closer look and appreciate the fact- why ULIPs or Endowment policy are favorite products among various Insurance agents and Relationship managers!!

This would be the total commission earned by an insurance agent if you choose a low cost and high life cover policy which is a pure insurance plan like a Term Life Insurance policy.

This would be the total commission earned by an insurance agent if you choose a low cost and high life cover policy which is a pure insurance plan like a Term Life Insurance policy.

Commission of Rs.4,43,250 with ULIP, over the period of 20 years; versus, the Commission of merely Rs.26,400 with Term Insurance Policy, over the period of 30 years!!

I hope you have got the idea behind the biased-ness of your insurance agents or relationship managers!

Concept of non-monetary benefits or Rewards to Insurance Agents and Intermediaries

Apart from all these hefty commissions, Insurance agents and Relationship managers also enjoy non-monetary rewards from the companies, for selling their traditional plans (ULIPs, endowment, money-back policies).

Rewards refer to incentives in the form of term insurance cover, mobile phone charges, office allowance, sales promotion gifts, competition prizes, international tour packages, and other such stuff.

It adds up an additional 8% non-monetary commission on top of 35% monetary commission benefits, that relationship managers or insurance agents were already pocketing.

So, beware of any misselling or justification provided by your Relationship managers to invest in insurance policies.

Now, what are the justification made by your Relationship Manager in order to sell insurance policies? We will look at it in the next section.

Relationship managers’ justification to sell Investment-cum-Insurance plans

The relationship manager or an insurance agent would try to mis-sell a traditional plan or a ULIP to you by giving a couple of justifications that they always keep prepared. They would first devalue a pure insurance plan (Term plan) like this,

- A term plan will only give you life cover only in case of your demise during the term period and if you survive the term you will not get anything. It means your family gets money if you die and you get nothing if you survive!

- So, all the money you spend as a premium will be wasted if you don’t die within the tenure.

The basic purpose of a Life Insurance is to give life cover for your family in case of an unfortunate situation. Even though a pure term plan fulfills the purpose (₹ 1 Crore life cover for a total premium of ₹ 1.5 Lakh) these insurance agents will try to change your view on pure plans like they are useless.

Then the agents will exaggerate the cheap benefits of an investment insurance plan like this,

- Unlike a pure insurance plan, a traditional plan will give you a life cover in case of your demise and also if you survive the term period then you will get an assured sum as maturity amount. So, if you choose an investment insurance plan like traditional plan, your total premium money will not be wasted and will be given back to you along with an additional benefit amount (for a total premium of ₹ 30 Lakh if you die you get life cover of ₹ 50 Lakh; if you survive you get ₹ 70 Lakh on maturity).

To sell a ULIP plan, an insurance agent will tell you these points that they are taught during their training given by the insurance company,

- In ULIPs a part of your premium will be allotted for life insurance and a part of the premium will be invested across investments like equity and debt.

- You can also check the performance of your investment by the report which will be sent to you regularly.

- In case of your demise during the tenure, you will get an assured life cover or the NAV of your investment whichever is higher.

- In case you survive the tenure, you will get the returns of your investment.

These are the benefits of ULIP and traditional plans which an insurance agent could probably say to you to sell an insurance investment. But the only question you should ask is at what cost?

Why you should avoid Traditional and ULIP plans?

The basic purpose of a Life insurance plan is to give financial security to your family on your untimely demise. It is well served in a Pure Term Life Insurance plan where the life cover is nearly 100 times of your premium. As we have noticed in the previous section that the small annual premium of ₹ 8000 will give your family ₹ 1 Crore life cover.

But the insurance agents would suggest you to ‘invest in an insurance plan’ like a traditional plan (endowment/money back) or ULIP because it could give you an assured sum as life cover (which is nothing but the total payable premium) on your untimely demise and also an additional bonus (5-8% return)at the end of term if you survive.

But what actually happens is this. Both the term plan with a low yearly premium of ₹ 8000 and an endowment plan with a huge yearly premium of ₹ 1 Lakh will give you the same death benefit of ₹ 1 Crore! To be more precise, an endowment will give you a much lesser death benefit than a Term plan.

Insurance agents will try hard to sell investment cum insurance plans like traditional plans and ULIPs to you not because you could get a little more benefit, but because they could get a huge commission.

You will lose one important thing if you choose investment insurance. It is the ability to give financial support to your family with an efficient life cover, which is much needed in the time of your absence. This large life cover can be purchased at a very reasonable price through a pure insurance plan like a Term Insurance policy.

You should watch this video and understand why the combination of “Mutual Fund + Term Insurance” is a far better deal as compared to INVESTING in the insurance schemes such as ULIPs, endowment schemes or other money-back policies:

Final verdict

The insurance agents will most likely try to sell you a product which is a combination of investment and insurance. But what I suggest is this, “why can’t you insure and invest separately?!” If you insure your life with a low cost and high cover Term Life Insurance plan and invest the remaining sum in a safe investment platform like Mutual fund, the benefits you get will be the maximum. You should read this in-depth article on Mutual Funds and find out all the essentials in order to generate higher returns.

You can also read our article on Traditional vs. ULIP vs. Term+mutual fund to get a detailed insight into the cost of buying these plans and the benefits you actually get. If you have any specific query based on the points discussed in this article, OR you want to share any of your personal experiences, you can leave them in the comment section.

For building up your comprehensive Financial Plan, you should register for our FREE Complimentary Consultation call, by clicking the link below:

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘Book Now’ button below.

This is an eye opener. Protect this article and show to everyone who opts for ULIPs

Exhaustive article stating true commission of insurance policies .People need more awareness about this as banks earning huge commission on insurance and sharing none with customers.