Are you an NRI who is making most of your investments during your short visits to India?

Are you forced to make quick investment decisions because of the tight-packed agenda during those short visits?

Remember, those quick investment decisions will have long-term commitments. Are these investments aligned with your actual financial goals?So to help you cross all those investment barriers you need the assistance of an NRI Financial Advisor.

Is there any need for a Financial Planner in India for an NRI?

- Also, instead of making investment decisions based on the rules and regulations by yourself, or you may feel the need to hire a professional to manage your finances.

- Also, instead of making investment decisions based on the broad views you get from your relatives and friends in India, it is better to have a financial planner who can give you a complete and comprehensive financial plan even when you are abroad.

- As an NRI, instead of making investment decisions based on general opinions from relatives and friends in India, it is preferable to hire a financial planner who can provide you with a complete and comprehensive financial plan even if you are not in India.

The following reasons justify why a Financial Advisor for NRI is important.

When choosing a Certified Financial Planner (CFP) in India for personal financial services, NRIs should consider these 12 factors to protect their wealth and to earn better returns.

As a result, the Financial Planner that you choose should be able to facilitate you with expert NRI services for your Financial Needs.

Table of Content

Expertise in advising NRI clients requires the financial planner to be aware of

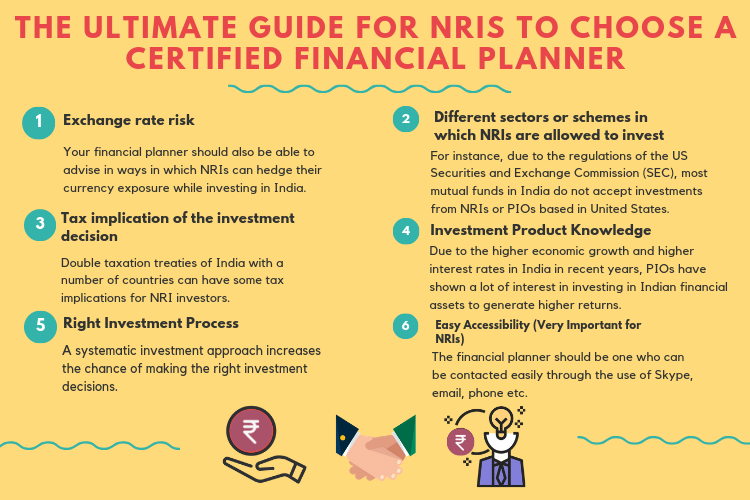

1.)Exchange rate risk

2.)Different sectors or schemes in which NRIs are allowed to invest

3.)Exposure to the right investment opportunities

4.)Tax implication of the investment decision

5.)Investment Product Knowledge

6.)Right Investment Process

7.)In-depth Requirement Analysis

8.)Macroeconomic Risks for NRIs

9.)Having adequate funds for Retirement

10.)Investment Transaction Execution for NRIs

11.)Easy Accessibility (Very Important for NRIs)

12.)Online Access

NRIs Specific to a Country

Expertise & Experience in handling Non-Resident Indians (NRIs)

As an NRI you need to select an experienced financial planner, who will be able to understand the needs and constraints of NRI customers in a better way than the ones who have no experience in handling NRI clients.

Like the other NRIs, you should not make the mistake of choosing a generic financial planner who has no experience with NRI clients.

Expertise in advising NRI clients requires the financial planner to be aware of:

12 Factors to Consider For NRIs Before Choosing a Financial Planner In India

1) Exchange rate risk for NRIs

Your financial planner should understand the impact of currency movements on the value of investments made by NRIs.

While giving investment advice, your financial planner should clearly explain to the NRI clients like you, the impact on the value of their investments of any adverse currency movement.

When the Indian currency depreciates against the currency in which an NRI earns, then the after-tax return generated from investment in India will be lower in terms of the currency of income of the NRI. This knowledge and awareness can only be gained by serving as NRI Financial Advisor over time.

Your financial planner should also be able to advise on ways in which NRIs can hedge their currency exposure while investing in India.

Hedging can ensure that the value of investment remains the same despite adverse exchange rate movement.

If you wish to Hedge your investments then you can approach a Financial Planner for NRI for this process.

2) Different sectors or schemes in which NRIs are allowed to invest

You should remember that not every investment avenue in India is available for NRIs.

For instance, due to the regulations of the US Securities and Exchange Commission (SEC),most Mutual Funds in India do not accept investments from NRIs or PIOs based in the United States. The same is the case with Canada.

So when you approach Indian Financial Advisor who services predominantly to Resident Indians, you are only able to get little guidance in all these aspects.

3) Exposure to the Right Investment Opportunities

Some financial planners say that NRIs should build a portfolio that includes three parts:

- one part invested in international stocks,

- one part invested in Indian stocks and

- one part invested in bonds.

Other financial planners say that NRIs should invest all their money in Indian stocks because they are not exposed enough to international stocks.

You should be looking for an advisor who is familiar with the wealth of investment opportunities available both in the international financial markets as well as in India. Therefore, consulting a Financial Planner for NRI in India could be ideal for catering to your Financial Requirements.

4) Tax implication of the investment decision for NRIs

Your financial planner should be well-versed in the tax implications of investments for an NRI in financial assets in India.

Securities transaction tax, taxes on short-term and long-term capital gains, etc can affect the final value. So these are all the things that an NRI investor realizes from the investment in India.

Double taxation treaties of India with several countries can have some tax implications for NRI investors.It might be difficult for Financial Advisors in India to keep track of all these changes.

So, before selecting your financial planner, you need to check whether the financial planner knows all these tax implications.

Must Read: An NRIs Perfect Guide for Income Tax Planning

5) Investment Product Knowledge

Before guiding NRIs in India, what should a Financial Advisor know?

The right financial planner would understand clearly the various investment schemes that are available for NRIs or PIOs.

Due to the higher economic growth and higher interest rates in India in recent years, PIOs have shown a lot of interest in investing in Indian financial assets to generate higher returns.

Even these factors are more important while doing Financial Planning for NRI in India.

6) Right Investment Process for NRIs in India

The biggest advantage of choosing the right financial planner is that a systematic investment process will be followed.

A systematic investment approach increases the chance of making the right investment decisions. NRI clients should take the services of a financial planner so that they make better investments.

Many NRIs think that they do not need to take the services of a financial planner; they can make investments without needing any advice. This approach often proves to be harmful and loss-making.

7) In-depth Requirement Analysis for NRIs

Your financial planner should be able to identify the investment horizon of NRI customers like you. Different NRI customers can have different investment horizons. So indeed you expect your professional Financial Planner to provide expert NRI services for financial needs.

A clear investment policy statement should be made by the financial planner.

This investment policy statement should clearly state the investment goals, investment horizon and risk tolerance of the NRI investor.

Your financial planner should be able to assess your goals in India and overseas. He should be able to come up with different investment options – repatriable and non-repatriable – for different investment goals.

8) Macroeconomic Risks for NRIs

The financial planner should also be able to understand the various macroeconomic risks that can have an impact on the investments made by NRIs in India.

India is a developing country with a unique set of macroeconomic risks and opportunities.

These macroeconomic risks include higher oil prices and the country’s dependence on imports for meet more than 80% of its energy needs.

When oil prices rise, the Indian currency tends to depreciate against other currencies. An NRI may realize lower returns from his / her investment in India because of this depreciation.

Another macroeconomic risk relating to India is political or economic instability. An increase in the fiscal deficit or current account deficit can be an important macroeconomic risk for the economy.

This again proves the fact that why is it recommended for an NRI to approach to reach out for an NRI Financial Advisor.

9) Having Adequate Funds for Retirement

The financial planner must be able to help you with your customised retirement plan as an NRI.

The financial planner should be able to guide you through the process of

- determining your asset allocation based on your risk profile,

- selecting appropriate investment avenues within each asset class,

- assisting you in managing your cashflows with the necessary discipline to invest, and

- reviewing your portfolio regularly

to ensure that you are on track to meet your important financial goal.

Keeping this in mind you should choose your NRI Financial Advisor who you think is more reliable and approachable.

Must Read: 7 Basic Factors every NRI ought to know about Retirement Planning

10) Investment Transaction Execution for NRIs

The financial planner should also be able to offer convenient ways in which NRI clients can invest, once the asset in which the investment has to be made is decided. Your Financial Advisor should be experienced in effectively doing wealth management for NRI.

This is where the importance of choosing the right financial advisor comes in. It is very difficult if we go on looking for the right financial advisor using the trial and error method but we can choose a certified financial planner after a careful analysis.

The financial planner should advise NRIs on the entire value chain of the investment process and ways in which investments can be made most conveniently,

such as through online transfer in the scheme, is an area in which the financial planner should be well-versed.

The financial planner should have an understanding of the transactional side too so that he can guide NRI clients on how to make investments most conveniently.

11) Easy Accessibility (Very Important for NRIs)

Your financial planner should make use of the latest technology products or tools when it comes to communication.

The financial planner should be one who can be contacted easily through the use of Skype, email, phone etc.

Due to the geographical distance involved, NRI investors like you may face difficulty and dissatisfaction if you are not able to communicate easily and in real-time with your financial advisor.

So, as an NRI, when you look for a financial advisor, you should also enquire about the communication modes/ methods that the financial planner uses for communication with clients.

It is very important factor for NRI investors but still certain investors fail to make note of it. So this factor should also be given equal importance like other factors by NRIs in choosing the Financial Planner.

12) Online Access

The use of FinTech software, helps financial planner as well as their clients to invest and track their portfolios online anytime and anywhere.

A financial planner, with the help of communication tools, can send Portfolio reports/Newsletter to their clients effortlessly at regular intervals and whenever required to keep their clients informed about their portfolio and market.

Regular communication of a financial planner plays a vital role in keeping the emotions of investors under control which advises the investors to be rational and avoid making wrong investment decisions out of market volatility.

So as NRI investors, it is important for them to maintain strong and stable relationships with their Financial Planner.

Beware of Following Financial Planners

NRIs Specific to a Country

Case 1: NRIs in Gulf Countries:

Over 2 million NRIs live and work in Gulf countries such as UAE. Most of them intend to return to India at the time of their retirement. They have an option of contacting UAE Financial Planners who have their base in India.

They send billions of dollars every year as remittances to their families in India.

They want to preserve their savings and grow them so that their retirement needs and those of their family members can be met.

The financial planner should have a clear understanding of the investment objectives of such clients while giving them advice.

Factors such as the city where a client intends to settle after retirement, the cost of living in that city, etc, are important factors in investment advice.

An issue with NRIs living in Gulf countries is that many of them go to these countries on temporary jobs or assignments.

They work for 5 to 10 years and then come back to the country. Some of the white-collar jobs are not secured. Anytime, they may lose their job.

An ‘NRI Financial Advisor’ should know how to accommodate this job insecurity in the financial plan.

Back in India, they work in Indian jobs at comparatively lesser salaries. The financial planner should understand the situation of many NRIs and advise them appropriately.

Such advice should be about how to invest the savings made during years of working in the Gulf so that the returns earned can offset the decline in income in later years.

Case 2: NRIs in USA, Canada, and Europe:

The USA and Canada-based NRIs may have to pay tax on the accrued income from the investments made in India. This needs to be accounted for in the financial plan.

Your financial planner should have worked with different kinds of NRIs – NRIs who settle abroad; NRIs who will return to India in the future; NRIs who have not yet decided about returning or settling.

These different categories of NRIs need different treatment in their financial plan.

Your financial planner should be comfortable with all these categories of NRI and should have proper strategies to address their different financial situations.

Financial Planner’s Fees:

The fee that the financial planner charges should also be taken into consideration before the final decision to take the services of that financial planner.

The very high fee can result in lower net returns for the NRI client from their investment.

But, please be careful of quacks posing as an ‘NRI financial advisor’ and misselling high commission paying insurance policies.

This makes it even more important for you to know, your Financial Planner is well-educated and trained in doing Financial Planning for NRIs.

The cost of choosing a wrong the Financial Planner:

People often fail to understand the significance of choosing the right financial planner.

They don’t realize that a lifetime of their effort can go down the drain if they choose the wrong financial planner.

The right financial planner can multiply their wealth significantly and make them richer and happier.

The right financial planner is one of the requirements for a successful financial life. If you do not have one, then go get one soon.

Definite Ways to Find Trustworthy Financial Planners

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30-minute FREE Financial Plan Consultation. Click the ‘Book Now’ button below.

Need help in understanding tax complications as I am currently employed outside India but stuck in India during Covid lockdowns placed by many countries

Hi!

If you are interested, then you can sign up for our 30-minute Complimentary Financial Plan Consultation to talk with our Certified Financial Planners.

Click the link to get your appointment.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Hi,

Seems interesting

Can we have an initial chat

Thanks

Shyam

Sure. You can start with our complimentary consultation. Please register in this link (https://www.holisticinvestment.in/complimentary-financial-plan-consultation/) to avail our free consultation.