Is the Bharti AXA Life Wealth Pro Plan genuinely aligned with your long-term goals, or does it only look attractive on paper?

Can the Bharti AXA Life Wealth Pro Plan outperform simple mutual fund investments over time?

Is the Bharti AXA Life Wealth Pro Plan truly a smart wealth-building ULIP, or just another complex product with hidden costs?

This article examines the plan in detail, evaluating its features, benefits, and limitations.

Table of Contents

What is the Bharti AXA Life Wealth Pro?

What are the features of the Bharti AXA Life Wealth Pro?

Who is eligible for the Bharti AXA Life Wealth Pro?

What are the features of the Bharti AXA Life Wealth Pro?

What are the investment strategies and fund options in the Bharti AXA Life Wealth Pro?

What are the charges of the Bharti AXA Life Wealth Pro?

Grace Period, Discontinuance and Revival of the Bharti AXA Life Wealth Pro

Free Look Period for the Bharti AXA Life Wealth Pro

Surrendering the Bharti AXA Life Wealth Pro

What are the advantages of the Bharti AXA Life Wealth Pro?

What are the disadvantages of the Bharti AXA Life Wealth Pro?

Research Methodology of Bharti AXA Life Wealth Pro

Benefit Illustration – IRR Analysis of Bharti AXA Life Wealth Pro

Bharti AXA Life Wealth Pro Vs. Other Investments

Bharti AXA Life Wealth Pro Vs. Pure-term + Equity Mutual Fund

Final Verdict on the Bharti AXA Life Wealth Pro

What is the Bharti AXA Life Wealth Pro?

Bharti AXA Life Wealth Pro is a unit-linked, non-participating individual life insurance plan.

This plan offers you a comprehensive life and financial solution that gives you life coverage up to 10 times your premium and helps build wealth over the long term to ensure that you and your family fulfil all your aspirations.

What are the features of the Bharti AXA Life Wealth Pro?

- The plan offers two variants to choose from: the Growth Variant and the Legacy Variant.

- A wealth booster, calculated as a percentage of the fund value, is added at specified intervals.

- It allows you to select from two investment strategies and multiple fund options, aligned with your investment objectives and risk–return profile.

- Tax benefits may be available on premiums paid and benefits received, subject to the prevailing tax laws.

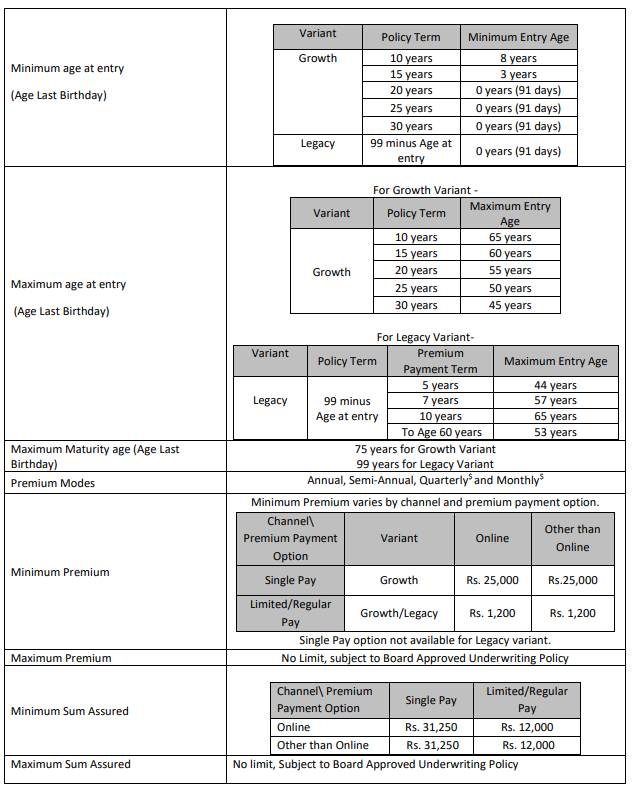

Who is eligible for the Bharti AXA Life Wealth Pro?

What are the features of the Bharti AXA Life Wealth Pro?

Death benefit

In case of the death of the Life Insured during the Bharti AXA Life Wealth Pro Plan Policy Term, the Death Benefit will be payable to the Nominee or the Policyholder, as the case may be, subject to the Policy being in force. Death Benefit, which is the higher of:

- Sum assured less all partial withdrawals made during the two-year period immediately preceding the date of death of the Life Assured

- Policy Fund Value (including any Loyalty Additions) as on the date of death

- 105% of all premiums paid as on date of death

Maturity Benefit

On maturity, subject to the Bharti AXA Life Wealth Pro Plan policy being in force and depending upon the variant chosen, you shall be eligible for the Maturity Benefit as follows –

Growth Variant

Maturity Benefit payable shall be equal to the Bharti AXA Life Wealth Pro Plan Policy Fund Value (including Return of Mortality Charges, Return of Premium Allocation Charges and Wealth Boosters) as on the date of maturity

Return of Mortality Charges (RoMC) and Return of Premium Allocation Charge (RoPAC): Subject to the Bharti AXA Life Wealth Pro Plan Policy being in force, the total amount of Mortality charges and total Premium Allocation Charges (excluding any applicable tax/cess levied) deducted during the Policy Term will be credited to the Policy at maturity.

Legacy Variant

Maturity Benefit payable shall be equal to the Bharti AXA Life Wealth Pro Plan Policy Fund Value (including Loyalty Additions and Wealth Boosters) as on the date of maturity.

Settlement Option on Maturity (Applicable for both Growth and Legacy Variant)

You may choose to receive the Policy Fund Value as:

- A lump sum payment

- At regular intervals chosen by the Bharti AXA Life Wealth Pro Plan Policyholder, during the Settlement Period

- A combination of the above

Loyalty Addition (Applicable for Legacy Variant)

Subject to the Bharti AXA Life Wealth Pro Plan Policy being in force, Loyalty Additions will be credited to the Policy at the end of each Policy Year in the Legacy Variant (chosen by the Policyholder at inception)

| Variant | Policy Year | % of Policy Fund Value as at end of Policy Year |

| Legacy | From the end of Policy Year 10 till one year before maturity | 0.75% |

Wealth Booster

Subject to the Bharti AXA Life Wealth Pro Plan Policy being in force, Wealth Booster will be credited to the Policy at the end of the fifth policy year and at the Maturity date.

| Variant | Policy Year | % of Policy Fund Value as at end of Policy Year |

| Growth & Legacy | End of 5th Policy Year | 0.25% |

| At Maturity | 1.25% |

What are the investment strategies and fund options in the Bharti AXA Life Wealth Pro?

Depending on your financial objectives, you have the choice of investing your premiums in any or all of the following investment funds mentioned below:

| Asset Allocation | |||||

| S.no | Fund Name | Debt | Money Market Instruments | Equities | Risk Profile |

| 1 | Growth Opportunities Plus Fund | – | 0-20% | 80-100% | High |

| 2 | Grow Money Plus Fund | – | 0-20% | 80-100% | High |

| 3 | Build India Fund | 0-20% | 0-20% | 80-100% | High |

| 4 | Save ‘n’ grow Money Fund | 0-90% | 0-40% | 0-60% | Moderate |

| 5 | Steady Money Fund | 60-100% | 0-40% | – | Low |

| 6 | Safe Money Fund | 60-100% | 0-40% | – | Low |

| 7 | Stability Plus Money Fund | 55-100% | 0-20% | 0-25% | Moderate |

| 8 | Emerging Equity Fund | – | 0-35% | 65-100% | High |

| Money Market securities | Government securities | ||||

| Discontinued Policy Fund | 0-40% | 0-60% | |||

Investment Strategies

At the inception of the Bharti AXA Life Wealth Pro Plan Policy, you may also choose to allocate the premium/s in one of the Investment strategies as per the conditions of the Product, with a maximum of two Investment strategies being available.

You shall have the option to choose only one of the Strategies at a time.

Dynamic Fund Allocation

In case this strategy is chosen at inception, the 1st and subsequent premiums will be allocated (after deducting Premium Allocation Charges) to the Grow Money Plus Fund.

During the last 5 years of the Bharti AXA Life Wealth Pro Plan Policy Term (before maturity), the funds will automatically be rebalanced between the Grow Money Plus Fund and the Steady Money Fund to protect you against any adverse movements in the equity markets.

The Company will automatically allocate the monies between the Grow Money Plus Fund and the Steady Money Fund, from the end of the 5th year before Policy Maturity, in a pre-determined manner as described below, through switching Units in the respective Fund

| Year | Existing Funds | |

| Grow Money Plus Fund | Steady Money Fund | |

| (PT-5) yr | 80% | 20% |

| (PT-4) yr | 75% | 25% |

| (PT-3) yr | 70% | 30% |

| (PT-2) yr | 50% | 50% |

| (PT-1) yr | 0% | 100% |

Systematic Transfer Plan (STP)

The Company will automatically allocate the Premium received (after deducting Premium Allocation Charges) to purchase Units in the Safe Money Fund.

On each subsequent monthly anniversary, the Fund Value of [1/ (13 less month number in the Bharti AXA Life Wealth Pro Plan Policy Year)] of the Units available at the beginning of the month] shall be switched to the Grow Money Plus Fund by cancelling Units in the Safe Money Fund, and purchasing Units in the Grow Money Plus Fund till the availability of Units in Safe Money Fund.

You shall not be permitted to make partial withdrawals from the Safe Money Fund during the period when this investment strategy option is in force.

While STP is operational, you are not allowed to change your fund choice. This strategy can be availed only on annual Premium payment mode.

What are the charges of the Bharti AXA Life Wealth Pro?

i). Premium Allocation Charge

The Company will levy an Allocation Charge as a percentage of the Annualised Premium.

The balance allocation amount will be utilised to purchase Units for the Bharti AXA Life Wealth Pro Plan Policy in accordance with the Investment Fund Allocation mentioned by you.

| Policy Year | Single Premium | Limited/ Regular Premium | Limited/ Regular Premium |

| Annual Mode | Non-Annual Mode | ||

| Year 1 | 1.00% | 6.00% | 4.50% |

| Year 2 | 5.00% | 3.00% | |

| Year 3 | 4.00% | 3.00% | |

| Year 4 | 3.00% | 2.00% | |

| Year 5 + | 2.00% | 2.00% |

ii). Mortality Charge

This charge is applied on the Sum at Risk and is deducted proportionately by cancellation of units on a monthly basis.

The annual charge per thousand of Sum at Risk will be based on the attained Age of the Bharti AXA Life Wealth Pro Plan policyholder, age last birthday.

| Age | Mortality Rate |

| 30 Years | 0.977 |

| 35 Years | 1.202 |

| 40 Years | 1.68 |

| 45 Years | 2.579 |

iii). Policy Administration Charge

This charge is deducted by cancellation of units on a monthly basis. The monthly Policy administration charge as a percentage of the annual / Single Premium is as per the table below:

| Policy Year | Single Premium | Limited/RegularPremium |

| 1 – 5 | 0.15% | 0.15% |

| 6 – 10 | Nil | 0.45% |

| 11+ | Nil | Nil |

iv). Fund Management Charge

| Fund | Fund Management Charge |

| Growth Opportunities Plus Fund | 1.35% per annum |

| Grow Money Plus Fund | 1.35% per annum |

| Build India Fund | 1.35% per annum |

| Emerging Equity Fund | 1.35% per annum |

| Save ‘n’ grow Money Fund | 1.25% per annum |

| Steady Money Fund | 1.00% per annum |

| Safe Money Fund | 1.00% per annum |

| Stability Plus Money Fund | 0.80% per annum |

| Discontinued Policy Fund | 0.50% per annum |

v). Discontinuance Charge

The Discontinuance Charge shall be levied at the time of surrender or on Discontinuance of Premium, whichever is earlier. It depends on the year of discontinuance and the premium amount.

There is no discontinuance charge from the fifth year onwards.

Inference from the charges: These charges are applied throughout the Bharti AXA Life Wealth Pro Plan policy tenure, leading to a continuous erosion of returns over time.

Grace Period, Discontinuance and Revival of the Bharti AXA Life Wealth Pro

For other than Single Premium Policies

Grace Period

The Bharti AXA Life Wealth Pro Plan Policyholder gets a grace period of Fifteen (15) days in case of Monthly Premium Payment Mode and Thirty (30) days in case of Annual/ Semi Annual/ Quarterly Premium Payment mode.

Discontinuance

Discontinuance of Premium during lock-in period: the fund value after deducting the applicable discontinuance charges shall be credited to the discontinued policy fund, and the risk cover and rider cover, if any, shall cease.

At the end of the lock-in period, the proceeds of the discontinuance fund shall be paid to the Policyholder, and the Bharti AXA Life Wealth Pro Plan Policy shall terminate

Discontinuance of Policy after the lock-in Period: the Policy shall be converted into a reduced paid-up policy with the paid-up sum assured, i.e. original sum assured multiplied by the total number of premiums paid to the original number of premiums payable as per the terms and conditions of the Bharti AXA Life Wealth Pro Plan Policy.

Revival

The revival period for this product is three years from the date of the first unpaid premium.

Free Look Period for the Bharti AXA Life Wealth Pro

If you disagree with any of the terms and conditions of the Bharti AXA Life Wealth Pro Plan Policy, you can return the original Policy along with a letter stating the reason/s within 30 days of receipt of the Policy.

Surrendering the Bharti AXA Life Wealth Pro

Single premium policies

Surrender during lock-in period: The Bharti AXA Life Wealth Pro Plan Policyholder has an option to surrender at any time during the lock-in period.

Upon receipt of a request for surrender, the fund value, after deducting the applicable discontinuance charges, shall be credited to the discontinued policy fund.

The Bharti AXA Life Wealth Pro Plan Policy shall continue to be invested in the discontinued policy fund, and the proceeds from the discontinuance fund shall be paid at the end of the lock-in period.

Surrender after the lock-in period: the Bharti AXA Life Wealth Pro Plan Policyholder has an option to surrender the Bharti AXA Life Wealth Pro Plan Policy at any time.

Upon receipt of a request for surrender, the fund value as on the date of surrender shall be payable.

For other than Single Premium Policies:

Surrender during the lock-in period: the Bharti AXA Life Wealth Pro Plan Policyholder has an option to surrender the Policy anytime, and proceeds of the discontinued policy shall be payable at the end of the lock-in period or date of surrender, whichever is later.

Surrender after the lock-in period: the Bharti AXA Life Wealth Pro Plan Policyholder has an option to surrender the Policy anytime, and the proceeds of the policy fund shall be payable.

What are the advantages of the Bharti AXA Life Wealth Pro?

- The policyholder can opt for partial withdrawals from the Bharti AXA Life Wealth Pro Plan policy fund value after the completion of the 5-year lock-in period.

- A Systematic Withdrawal Plan (SWP) is available only under the Legacy Variant, allowing a pre-determined amount to be automatically withdrawn from the Bharti AXA Life Wealth Pro Plan policy fund value.

- For enhanced protection, optional riders can be added by paying an additional premium.

- Premiums can be paid on a monthly, quarterly, semi-annual, or annual basis.

What are the disadvantages of the Bharti AXA Life Wealth Pro?

-

- Policy loans are not allowed under this plan.

- No liquidity is available during the initial policy years.

- The sum assured may be insufficient.

- Investments are made using the net premium after deducting applicable charges.

Research Methodology of Bharti AXA Life Wealth Pro

The primary objective of market-linked investments is to generate superior long-term returns, with risk-taking investors seeking meaningful alpha.

To assess the return potential of the Bharti AXA Life Wealth Pro Plan, we analyse a case study using figures provided on the insurer’s portal and calculate the Internal Rate of Return (IRR) to evaluate its effectiveness against alternative investment avenues.

Benefit Illustration – IRR Analysis of Bharti AXA Life Wealth Pro

Consider a 40-year-old male who purchases the Bharti AXA Life Wealth Pro Plan with a sum assured of ₹20 lakh.

Both the Bharti AXA Life Wealth Pro Plan policy term and the premium payment term are 10 years, with an annual premium of ₹2 lakh. He chooses the Growth Variant.

| Male | 40 years |

| Sum Assured | ₹ 20,00,000 |

| Policy Term | 10 years |

| Premium Paying Term | 10 years |

| Annualised Premium | ₹ 2,00,000 |

If premiums are paid consistently, the maturity benefit comprises the fund value along with applicable maturity boosters. The projections below are based on assumed investment returns of 4% and 8% per annum and are not guaranteed.

| At 4% p.a. | At 8% p.a. | ||||

| Age | Year | Annualised premium / Maturity benefit | Death benefit | Annualised premium / Maturity benefit | Death benefit |

| 40 | 1 | -2,00,000 | 20,00,000 | -2,00,000 | 20,00,000 |

| 41 | 2 | -2,00,000 | 20,00,000 | -2,00,000 | 20,00,000 |

| 42 | 3 | -2,00,000 | 20,00,000 | -2,00,000 | 20,00,000 |

| 43 | 4 | -2,00,000 | 20,00,000 | -2,00,000 | 20,00,000 |

| 44 | 5 | -2,00,000 | 20,00,000 | -2,00,000 | 20,00,000 |

| 45 | 6 | -2,00,000 | 20,00,000 | -2,00,000 | 20,00,000 |

| 46 | 7 | -2,00,000 | 20,00,000 | -2,00,000 | 20,00,000 |

| 47 | 8 | -2,00,000 | 20,00,000 | -2,00,000 | 20,00,000 |

| 48 | 9 | -2,00,000 | 20,00,000 | -2,00,000 | 20,00,000 |

| 49 | 10 | -2,00,000 | 20,00,000 | -2,00,000 | 20,00,000 |

| 50 | 22,09,523 | 27,28,357 | |||

| IRR | 1.80% | 5.58% | |||

At 4% p.a. return: Fund value of ₹22.09 lakh with an IRR of 1.80% as per the Bharti AXA Life Wealth Pro Plan maturity calculator.

At 8% p.a. return: Fund value of ₹27.28 lakh with an IRR of 5.58% as per the Bharti AXA Life Wealth Pro Plan maturity calculator.

Despite being a market-linked product, the plan fails to deliver returns comparable to conventional debt instruments, falling short of the alpha investors typically expect.

Moreover, the maturity corpus is inadequate to meet the inflated cost of long-term financial goals, rendering the plan unsuitable for wealth creation.

From an insurance perspective, the sum assured is also insufficient to provide meaningful financial protection to the family.

The IRR analysis clearly indicates that the Bharti AXA Life Wealth Pro Plan weakens effective financial planning due to low return efficiency and inadequate life cover, making it an inferior choice for meeting both investment and insurance objectives.

Bharti AXA Life Wealth Pro Vs. Other Investments

Although the Bharti AXA Life Wealth Pro Plan is positioned as a market-linked product, its return profile remains inferior even to traditional debt instruments, making it an unattractive proposition for investors.

To put this into perspective, let us compare it with an alternative strategy that clearly separates insurance and investment, using the same assumptions and evaluation metrics as in the earlier illustration.

Bharti AXA Life Wealth Pro Vs. Pure-term + Equity Mutual Fund

A pure-term life insurance policy with a sum assured of ₹20 lakh requires an annual premium of ₹7,200 for a 10-year term.

This leaves ₹1,92,800 out of the ₹2 lakh annual outflow available for wealth creation. Based on individual risk appetite, this surplus can be allocated to either debt or equity instruments.

| Pure Term Life Insurance Policy | |

| Sum Assured | ₹ 20,00,000 |

| Policy Term | 10 years |

| Premium Paying Term | 10 years |

| Annualised Premium | ₹ 7,200 |

| Investment | ₹ 1,92,800 |

| Term insurance + Equity Mutual Fund | |||

| Age | Year | Term Insurance premium + Equity Mutual Fund | Death benefit |

| 40 | 1 | -2,00,000 | 20,00,000 |

| 41 | 2 | -2,00,000 | 20,00,000 |

| 42 | 3 | -2,00,000 | 20,00,000 |

| 43 | 4 | -2,00,000 | 20,00,000 |

| 44 | 5 | -2,00,000 | 20,00,000 |

| 45 | 6 | -2,00,000 | 20,00,000 |

| 46 | 7 | -2,00,000 | 20,00,000 |

| 47 | 8 | -2,00,000 | 20,00,000 |

| 48 | 9 | -2,00,000 | 20,00,000 |

| 49 | 10 | -2,00,000 | 20,00,000 |

| 50 | 35,72,353 | ||

| IRR | 10.33% | ||

If the surplus is invested in an equity mutual fund, the investment generates a pre-tax maturity value of ₹37.89 lakh and a post-tax corpus of ₹35.72 lakh.

The combined strategy of pure-term insurance plus equity mutual fund delivers a post-tax IRR of 10.33%.

| Equity Mutual Fund Tax Calculation | |

| Maturity value after 10 years | 37,89,404 |

| Purchase price | 19,28,000 |

| Long-Term Capital Gains | 18,61,404 |

| Exemption limit | 1,25,000 |

| Taxable LTCG | 17,36,404 |

| Tax paid on LTCG | 2,17,050 |

| Maturity value after tax | 35,72,353 |

This alternative approach results in a significantly higher corpus than the Bharti AXA Life Wealth Pro Plan. More importantly, the IRR comfortably exceeds inflation, making it far more effective for long-term wealth creation.

This comparison clearly reinforces the principle that separating insurance and investment leads to superior financial outcomes compared to bundling them into a single product.

The Bharti AXA Life Wealth Pro Plan fails to offer competitive returns, while its bundled structure restricts flexibility and efficiency.

In contrast, opting for a pure-term life insurance policy and investing independently in market-linked instruments provides a more robust, transparent, and goal-oriented solution for achieving both financial protection and wealth growth.

Final Verdict on the Bharti AXA Life Wealth Pro

The Bharti AXA Life Wealth Pro Plan is a conventional ULIP that provides equity exposure within an investment portfolio.

While it may appear attractive to investors seeking long-term equity participation, a deeper analysis highlights notable deficiencies in its return profile.

The plan delivers sub-optimal long-term returns, with an unfavourable risk–return trade-off.

Elevated charges steadily erode performance, and the sum assured is inadequate to meaningfully secure the financial future of dependents. As a result, the plan is ill-suited for equity allocation and it also has a high agent commission.

Equity investments warrant acceptance of higher risk only when they generate returns that comfortably exceed inflation.

To achieve superior risk-adjusted outcomes, investors are better served by allocating capital to other market-linked instruments rather than ULIPs.

For insurance needs, pure-term life policies remain the most efficient solution, offering substantial coverage at relatively low premiums.

A robust financial plan is best built with professional guidance.

Do Quora, Facebook, and Twitter have the final say when it comes to financial advice?

A qualified financial planner can structure a customised investment strategy aligned with your risk appetite, financial goals, and time horizon, ensuring clarity, efficiency, and long-term sustainability.

Leave a Reply