Your salary will likely grow with time.

Promotions, job switches, and experience almost guarantee it.

But here’s a critical question—does your wealth grow at the same pace?

Many people assume that earning more automatically leads to financial security.

Yet, decades later, they find themselves unprepared for retirement, burdened by debt, or chasing missed goals.

Why does this happen?

Because income growth without a structured financial plan is like running fast in the wrong direction.

To truly build wealth, your financial strategy must evolve with your life stages.

Let’s break down exactly what you should focus on—from your 20s all the way to retirement.

Table of Contents

- Why Financial Planning Must Evolve with Age

- Age 20–30: Building the Right Foundations

- Age 30–40: Scaling Income, Managing Responsibilities

- Age 40–50: Protecting and Consolidating Wealth

- Age 50–60: Transitioning Towards Retirement

- Age 60+: Turning Wealth into Income

- The Inflation Reality Check

- Common Mistakes Across Life Stages

- A Simple Age-Wise Financial Checklist

- Final Thoughts

1. Why Financial Planning Must Evolve with Age

Can the same financial strategy work for a 25-year-old and a 55-year-old?

Clearly not.

Your priorities shift—from career growth to family responsibilities, from wealth creation to wealth preservation.

Ignoring this shift often leads to poor decisions—either taking too much risk too late or playing too safe too early.

The key is alignment: your income, goals, and investments must move together.

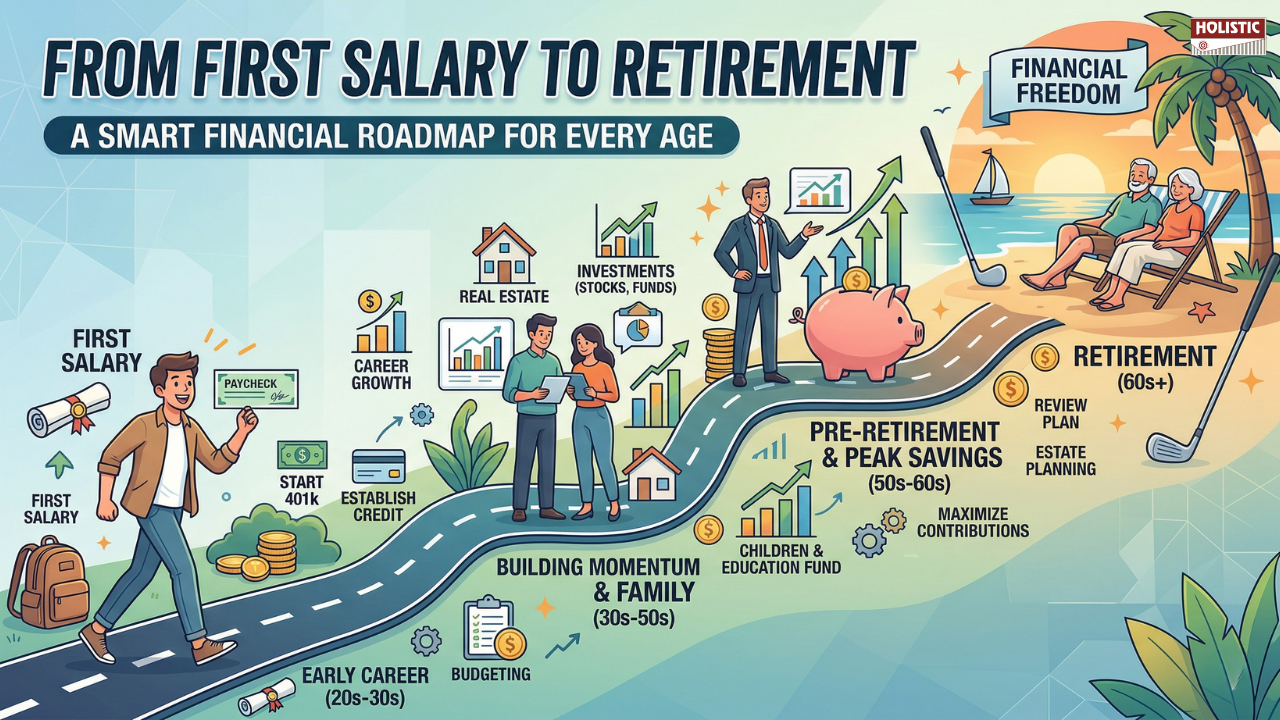

2. Age 20–30: Building the Right Foundations

This is the decade where your financial journey quietly—but powerfully—takes shape.

While your income may be modest, your biggest advantage is something money cannot buy later: time.

The earlier you begin, the more compounding works in your favour, turning even small investments into meaningful wealth over decades.

What typically happens?

At this stage, life is full of “firsts”—your first salary, first financial independence, and often, your first exposure to credit.

Lifestyle aspirations rise quickly.

A better phone, bike, travel, dining out—these feel like well-earned rewards.

At the same time, easy access to credit cards and personal loans can lead to spending beyond your means.

The real challenge? Balancing enjoyment with discipline.

What should you focus on?

Rather than trying to save what’s left after spending, reverse the approach.

Pay yourself first.

▸ Build a minimum 20% savings habit right from your first pay check

▸ Start a Systematic Investment Plan (SIP) in equity mutual funds to harness long-term growth

▸ Create an emergency fund covering at least 6 months of expenses

▸ Be cautious with EMIs—avoid turning lifestyle wants into long-term financial burdens

Even a small SIP started today can outperform a much larger investment started 10 years later.

The question is simple: are you giving your money enough time to grow?

3. Age 30–40: Scaling Income, Managing Responsibilities

By your 30s, your financial life becomes more structured—but also more demanding.

Your income typically grows significantly during this phase, but so do your responsibilities.

This is where many individuals earn well but struggle to build real wealth.

What typically happens?

This decade often brings major life milestones—marriage, children, and buying a home.

These come with emotional satisfaction, but also long-term financial commitments like EMIs, school fees, and family expenses.

As responsibilities increase, so does the pressure on your cash flow.

What should you focus on?

This is your wealth acceleration phase, and decisions made here have long-term consequences.

▸ Increase your savings rate to 30–40% of your income

▸ Protect your family with adequate term life insurance and comprehensive health insurance

▸ Move from random investing to goal-based investing—assign specific investments to each goal

▸ Avoid over-leveraging—just because you qualify for a larger loan doesn’t mean you should take it

A critical reflection here: Is your rising income creating assets—or just funding a more expensive lifestyle?

4. Age 40–50: Protecting and Consolidating Wealth

This is your peak earning phase—but also your most financially demanding period.

By now, you’ve spent two decades building your career.

Income is at its highest, but financial commitments often peak as well.

What typically happens?

Expenses related to children’s higher education, nearing loan repayments, and increasing healthcare needs begin to dominate.

At the same time, retirement is no longer a distant concept—it’s a visible milestone.

Mistakes made here can be difficult to recover from due to limited time.

What should you focus on?

This phase is about strengthening your financial position and reducing vulnerabilities.

▸ Prioritize debt elimination, especially high-interest and long-term loans

▸ Implement disciplined asset allocation—balance equity, debt, and gold based on risk tolerance

▸ Accelerate retirement contributions, even if it requires temporary lifestyle adjustments

▸ Avoid chasing high-risk or speculative investments in an attempt to “catch up”

The key question to ask yourself: Are you securing your future—or relying on hope to fix gaps later?

5. Age 50–60: Transitioning Towards Retirement

As retirement approaches, your strategy must gradually shift from growth to preservation.

This is not the time for aggressive experimentation—it is the time for careful alignment and clarity.

What typically happens?

Income growth stabilizes, and major financial responsibilities begin to wind down.

However, the reality of retirement expenses—healthcare, lifestyle, longevity—becomes more tangible.

What should you focus on?

Your primary goal now is to ensure that your accumulated wealth is protected, structured, and ready to generate income.

▸ Gradually reduce exposure to high-volatility assets

▸ Increase allocation to debt instruments and stable income-generating assets

▸ Define your retirement corpus requirement clearly

▸ Plan a Systematic Withdrawal Plan (SWP) to create a steady post-retirement income

This phase demands clarity: Do you know how much you need—and how your money will support you once income stops?

6. Age 60+: Turning Wealth into Income

Retirement marks a fundamental shift—from earning income to generating it from your accumulated wealth.

At this stage, your portfolio must transition from growth-oriented to income-oriented, without losing sight of longevity and inflation.

What typically happens?

Active income stops, and financial independence depends entirely on how well you have planned.

Stability, predictability, and peace of mind become more important than high returns.

What should you focus on?

The objective now is sustainability—ensuring your money lasts throughout your lifetime.

▸ Generate regular income through SWPs, pensions, or interest income

▸ Maintain a strong focus on capital preservation

▸ Withdraw conservatively to manage longevity risk

▸ Keep a portion invested in growth assets to counter inflation over long retirement years

The ultimate question becomes: Is your portfolio designed to support not just your lifestyle—but your entire retirement journey?

7. The Inflation Reality Check

A rising salary often creates a false sense of financial progress.

At first glance, steady increments feel reassuring.

You start with ₹25,000 per month, receive an average annual hike of 8%, and over time, your income grows significantly.

On paper, this looks like strong financial growth.

But here’s the uncomfortable question: Is your purchasing power really increasing at the same pace?

If inflation averages around 6%, the real growth in your income is far more modest than it appears.

Everyday expenses—housing, education, healthcare, and lifestyle costs—quietly rise year after year, eroding the true value of your earnings.

This is why many individuals feel financially stretched despite earning more than ever before.

The key takeaway is simple but powerful:

Salary growth alone does not create wealth—real wealth is built through disciplined investing.

Investments, particularly growth-oriented assets like equities, have the potential to outpace inflation over the long term.

Without them, you are merely running to stay in the same place financially.

So the real question becomes: Are you just earning more, or are you actually getting richer?

8. Common Mistakes Across Life Stages

Financial mistakes are rarely dramatic—they are usually small, repeated decisions that compound negatively over time.

Across different life stages, certain patterns consistently emerge:

▸ Delaying investments in the early years

Many individuals wait for a higher salary before they begin investing.

Unfortunately, this delay costs them the most valuable ingredient in wealth creation—time.

▸ Lifestyle inflation during peak earning years

As income rises, expenses often rise faster.

Bigger homes, expensive cars, and lifestyle upgrades can quietly consume what could have been long-term investments.

▸ Neglecting insurance and risk protection

Focusing only on returns while ignoring protection exposes families to financial shocks that can derail years of progress.

▸ Chasing past performance

Investing in funds or assets purely based on recent high returns often leads to poor timing—buying high and exiting low.

▸ Taking excessive risk close to retirement

Attempting to “catch up” by taking aggressive bets later in life can jeopardize the very corpus meant to provide stability.

Avoiding these mistakes does not require exceptional financial knowledge—just awareness and discipline.

In many cases, what you avoid doing is just as important as what you choose to do.

9. A Simple Age-Wise Financial Checklist

A structured approach can simplify decision-making across different life stages.

Instead of overcomplicating your strategy, focus on the key priorities that matter most at each phase.

| Life Stage | Focus Area | Key Actions |

|---|---|---|

| 20–30 | Foundation | Build savings habit, start SIPs, create emergency fund |

| 30–40 | Growth | Increase savings rate, secure insurance, invest for goals |

| 40–50 | Stability | Reduce debt, diversify investments, strengthen retirement planning |

| 50–60 | Transition | Protect capital, shift allocation, finalize retirement strategy |

| 60+ | Income | Generate steady cash flow, preserve wealth, manage withdrawals |

Think of this as a guiding framework rather than a rigid formula.

Your personal goals, risk appetite, and life circumstances should always shape the final decisions.

10. Final Thoughts: Wealth Is Built in Phases

Wealth creation is not a one-time decision—it is a journey that unfolds over decades.

Each stage of life offers a different advantage:

- In your 20s, time works quietly in your favor

- In your 30s and 40s, income becomes your strongest lever

- In your 50s and beyond, discipline ensures everything you built is preserved

The challenge is not just earning more or investing more—it is making the right decisions at the right time.

Miss this alignment, and even a high income may not translate into financial freedom.

Get it right, and even modest beginnings can lead to significant wealth over time.

And if you want a structured, unbiased approach tailored to your life stage and goals, working with a qualified Certified Financial Planner (CFP) can help bring clarity and confidence to your financial journey.

Leave a Reply