Can the HDFC Life Smart Pension Plus Plan ensure your golden years are truly golden, without the stress of financial uncertainty?

Can the HDFC Life Smart Pension Plus Plan turn your retirement dreams into a financially secure reality?

Can the HDFC Life Smart Pension Plus Plan secure a retirement that guarantees comfort and dignity?

This article delves into the workings of an annuity plan, offering a detailed review of the HDFC Life Smart Pension Plus Plan, including its features, benefits, drawbacks, and potential returns.

Table of Contents:

- What is the HDFC Life Smart Pension Plus?

- What are the features of the HDFC Life Smart Pension Plus?

- Who is eligible for the HDFC Life Smart Pension Plus?

- What are the annuity options and the benefits of the HDFC Life Smart Pension Plus?

- Grace period, Lapsed Policy and Revival of the HDFC Life Smart Pension Plus

- Free Look Period of the HDFC Life Smart Pension Plus

- Surrendering the HDFC Life Smart Pension Plus

- What are the advantages of the HDFC Life Smart Pension Plus?

- What are the disadvantages of the HDFC Life Smart Pension Plus?

- Research Methodology of HDFC Life Smart Pension Plus?

- Benefit illustration – IRR Analysis of HDFC Life Smart Pension Plus

- HDFC Life Smart Pension Plus Vs. Other investments

- HDFC Life Smart Pension Plus Vs. Other Fixed-return instruments

- HDFC Life Smart Pension Plus Vs. Inflation-adjusted income

- Risks to Consider Before Buying HDFC Life Smart Pension Plus

- Final Verdict on HDFC Life Smart Pension Plus

What is the HDFC Life Smart Pension Plus?

HDFC Life Smart Pension Plus is a Non-Linked, Non-Participating Individual/Group Annuity Savings Plan.

HDFC Life Smart Pension Plus Plan ensures you have financial independence with a secure and regular stream of income during your retirement period.

It is designed as a retirement income solution that converts your accumulated savings into a guaranteed lifelong pension.

For individuals looking for a predictable retirement income plan in India, annuity plans like HDFC Life Smart Pension Plus help create financial stability after retirement.

What are the features of the HDFC Life Smart Pension Plus?

- A plan designed to suit both Single and Joint Life needs.

- Flexible pay-out options: Receive your annuity income monthly, quarterly, half-yearly, or annually.

- Guaranteed annuity income for life with a single premium or limited payment term.

- Choice between Immediate Annuity or Deferred Annuity options.

- Option to delay annuity pay-outs by selecting a deferment period.

- Four annuity variants to choose from:

A. Life Annuity

B. Life Annuity with Return of a Percentage of Total Premiums Paid

C. Life Annuity with Early Return

D. Increasing Annuity

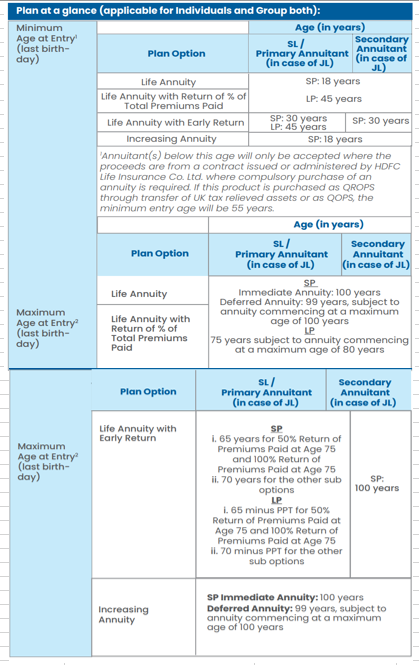

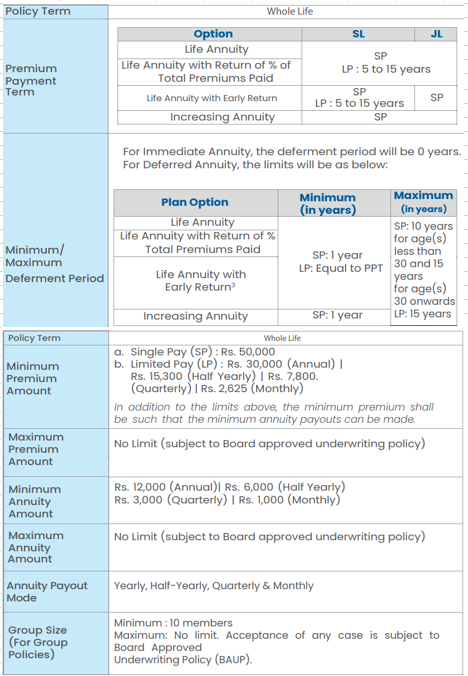

Who is eligible for the HDFC Life Smart Pension Plus?

The HDFC Life Smart Pension Plus eligibility depends on factors such as minimum entry age, maximum maturity age, premium payment option chosen, and the type of annuity selected.

Both individual investors planning retirement and NPS subscribers looking for annuity options after retirement can consider this plan.

What are the annuity options and the benefits of the HDFC Life Smart Pension Plus?

You can choose any of the following annuity options at inception.

- Life Annuity

- Life Annuity with Return of % of Total Premiums Paid

- Life Annuity with Early Return

- Increasing Annuity

Choosing the right annuity option is important because it determines how long the pension will be paid, whether the premium is returned to nominees, and how income flows during retirement.

i.) Life Annuity

| Options | Survival benefit | Annuity Amount | Death benefit |

| Single pay/Limited pay Immediate annuity/ Deferred annuity Single life/Joint Life |

Paid in arrears post deferment period as long as the annuitant(s) is/are alive |

Single Pay: Annuity Rate x Single Premium Limited Pay: Annuity Rate x Annualized Premium |

Immediate Annuity – No Benefits Deferred Annuity – During the deferment period: 105% of the Total Premiums Paid After the deferment period: No Benefits |

This option is typically chosen by individuals who want the highest possible annuity income for their lifetime without additional return-of-premium benefits.

ii.) Life Annuity with Return of % of Total Premiums Paid

| Options | Survival benefit | Annuity Amount | Death benefit |

| Single pay/Limited pay Immediate annuity/ Deferred annuity Single life/Joint Life |

Paid in arrears post deferment period as long as the annuitant(s) is/are alive |

Single Pay: Annuity Rate x Single Premium Limited Pay: Annuity Rate x Annualized Premium |

Immediate Annuity – x% of Total Premiums Paid Deferred Annuity – During the Deferment Period: Higher of – Total Premiums Paid accumulated at 6% p.a. compounded daily or 105% of the Total Premiums Paid After the Deferment Period: Higher of – Total premiums paid accumulated at 6% p.a. compounded daily less Total Annuity Payouts made till date of death or x% of the Total Premiums Paid |

This option is preferred by retirees who want lifelong pension income while ensuring that a portion of the invested premium is returned to their nominee after death.

iii.) Life Annuity with Early Return

| Options | Survival benefit | Annuity Amount | Death benefit |

| Single pay/Limited pay Immediate annuity/ Deferred annuity Single life/Joint Life ▪ Option I – 50% Return of Premiums Paid, at Age 75 ▪ Option II – 100% Return of Premiums Paid at Age 75 ▪ Option III – 50% Return of Premiums Paid at Age 80 ▪ Option IV – 100% Return of Premiums Paid at Age 80 ▪ Option V – 100%Return of Premiums Paid between 76 to 95 |

Paid in arrears post deferment period as long as the annuitant(s) is/are alive Survival till milestone age(s) – Benefits will be based on the chosen option |

Single Pay: Annuity Rate x Single Premium Limited Pay: Annuity Rate x Annualized Premium |

Immediate Annuity – Total Premiums Paid less survival benefit on milestone age(s) already paid Deferred Annuity – During the Deferment Period: Higher of Total Premiums Paid accumulated at 6% p.a. compounded daily or 105% of the Total Premiums Paid After the Deferment Period: Higher of Total Premiums Paid accumulated at 6% p.a. compounded daily less Total Annuity Payouts made till the date of death or Total Premiums Paid less survival benefit on milestone age(s) already paid till the date of death |

This variant provides milestone-based benefits, making it suitable for retirees who want access to part of their invested premium at specific ages.

iv.) Increasing Annuity

| Options | Survival benefit | Annuity Amount | Death benefit |

| Single pay Immediate annuity/ Deferred annuity Single life/Joint Life With/without return of premium Option I – x% p.a. simple increase every year Option II – x% p.a. compound increases every year |

Paid in arrears post deferment period as long as the annuitant(s) is/are alive |

Single Pay: Annuity Rate (t) x Single Premium Annuity Rate (t) represents the rate applicable for policy year ‘t’ | Immediate Annuity -Single Premium, if ROPP is selected or Nil otherwise Deferred Annuity – Death during Deferment Period -a. If ROPP is selected: Higher of Single Premium Paid accumulated at 6% p.a. compounded daily or 105% of the Single Premium Paid b. If ROPP is not selected: 105% of Single Premium Paid Death after Deferment Period – a. If ROPP is selected: Higher of Single Premium Paid accumulated at 6% p.a. compounded daily less Total Annuity Payouts made till date of death or Single Premium Paid b. If ROPP is not selected: Nil |

Increasing annuity options help retirees partially address rising living costs by gradually increasing pension pay-outs over time.

Grace period, Lapsed Policy and Revival of the HDFC Life Smart Pension Plus

Grace Period

The grace period for payment of the premium shall be 15 days, where the HDFC Life Smart Pension Plus Plan policyholder pays the premium on a monthly basis and 30 days in all other cases.

Grace periods ensure that temporary delays in premium payment do not immediately terminate the policy benefits.

Lapsed Policy

The policy acquires Guaranteed Surrender Value (GSV) on payment of at least one year’s premiums in case of Limited Pay

For limited pay policies, the HDFC Life Smart Pension Plus Plan policy will lapse if it has not acquired a Guaranteed Surrender Value (GSV). No benefit will be paid on the lapse of the policy.

If a due premium is unpaid upon the expiry of the grace period, the policy will become paid-up if it has acquired a Guaranteed Surrender Value (GSV).

A paid-up policy allows policyholders to retain limited benefits without continuing premium payments.

Revival

A policy can be reinstated during the HDFC Life Smart Pension Plus Plan policy term but within a period of five years from the date of the first unpaid premium.

Revival provisions allow policyholders to restore their retirement plan benefits by paying pending premiums within the specified revival period.

Free Look Period of the HDFC Life Smart Pension Plus

In case the HDFC Life Smart Pension Plus Plan Policyholder is not agreeable to any terms and conditions stated under this product, the insured shall have the option of returning the policy within 30 days from the date of receipt of the policy.

The free look period allows policyholders to review the annuity policy terms and cancel the plan if it does not align with their retirement planning needs.

Surrendering the HDFC Life Smart Pension Plus

The policy acquires Guaranteed Surrender Value (GSV) immediately on payment of premium in case of Single Pay and on payment of at least one year’s premiums in case of Limited Pay.

Surrender value payable will be equal to the higher of Guaranteed Surrender Value (GSV) and Special Surrender Value (SSV).

Surrendering the policy allows policyholders to exit the annuity plan early, subject to surrender value conditions defined by the insurer.

What are the advantages of the HDFC Life Smart Pension Plus?

- In the event of the policyholder’s death, the nominee can utilize the annuitization provision.

- Includes the NPS – Family Income Option for NPS subscribers.

- Policyholders have the option to receive a lump sum by opting for reduced annuity payments and benefits.

- The Advanced Annuity Option enables withdrawal of the present value of annuities for the next 1 to 5 years as a lump sum in advance.

What are the disadvantages of the HDFC Life Smart Pension Plus?

- Annuity option once chosen at inception can’t be changed during the policy term.

- The annuity is fully taxable

- The plan can be surrendered only on the specified period

- There is no yearly step-up annuity to beat inflation

- Fixed annuity income may lose purchasing power over long retirement periods due to inflation.

- Compared to market-linked retirement investments, annuity plans generally offer lower flexibility and limited liquidity.

Research Methodology of HDFC Life Smart Pension Plus?

The HDFC Life Smart Pension Plus Plan offers fixed returns, meaning your annuity amount is determined at the time of purchase and remains unaffected by changes in economic interest rates.

This makes the plan a predictable retirement income product where the pension amount remains stable regardless of market fluctuations or interest rate movements.

Let’s evaluate the Internal Rate of Return (IRR) for this plan using figures from the HDFC Life Smart Pension Plus Plan policy brochure.

IRR is commonly used in retirement planning analysis to evaluate the real return generated by annuity plans and compare them with other fixed-income investments.

Benefit illustration – IRR Analysis of HDFC Life Smart Pension Plus

Consider a 60-year-old male who invests ₹10 lakhs in the plan and selects Option B: Life Annuity with Return of 100% of Total Premiums Paid.

He opts to receive an annual annuity of ₹63,200 for life, starting immediately.

Since it is a lifetime annuity, we assume a life expectancy of 85 years.

| Male | 60 years |

| Purchase Price | ₹ 10 Lakhs |

| Life Expectancy | 85 years |

| Annuity (per annum) | ₹ 63,200 |

This example helps illustrate how a typical annuity pay-out works in retirement income planning scenarios.

At age 85, the purchase price is returned to the nominee.

Based on this cash flow, the IRR is calculated to be 6.21% as per the HDFC Life Smart Pension Plus Plan maturity calculator.

The IRR calculation helps investors understand the effective annual return generated by the annuity plan over the assumed retirement horizon.

| Age | Life Annuity with Return of % of Total Premiums Paid |

| 60 | -10,00,000 |

| 61 | 63,200 |

| 62 | 63,200 |

| 63 | 63,200 |

| 64 | 63,200 |

| 65 | 63,200 |

| 66 | 63,200 |

| 67 | 63,200 |

| 68 | 63,200 |

| 69 | 63,200 |

| 70 | 63,200 |

| 71 | 63,200 |

| 72 | 63,200 |

| 73 | 63,200 |

| 74 | 63,200 |

| 75 | 63,200 |

| 76 | 63,200 |

| 77 | 63,200 |

| 78 | 63,200 |

| 79 | 63,200 |

| 80 | 63,200 |

| 81 | 63,200 |

| 82 | 63,200 |

| 83 | 63,200 |

| 84 | 63,200 |

| 85 | 10,00,000 |

| IRR | 6.21% |

While the HDFC Life Smart Pension Plus provides a reliable income stream during retirement, it lacks liquidity since the invested amount is locked in.

Moreover, the annuity amount remains fixed throughout the individual’s lifetime, making it vulnerable to inflation over time.

This is a common limitation seen in many traditional annuity products where fixed pay-outs may gradually lose purchasing power during long retirement periods.

In summary, the HDFC Life Smart Pension Plus Plan offers a moderate rate of return but is limited by its lack of liquidity and inability to provide inflation-adjusted income.

HDFC Life Smart Pension Plus Vs. Other investments

For retirees seeking a regular income stream, several alternatives to annuity plans offer better returns and liquidity.

Let’s explore some fixed-income options available. The returns mentioned are as of November 2024:

These instruments are commonly used in retirement portfolios to generate predictable income with varying levels of liquidity and safety.

HDFC Life Smart Pension Plus Vs. Other Fixed-return instruments

| Investment Option | Expected Returns |

| Bank Fixed Deposit (FD) | 6-7% annually |

| Senior Citizen Savings Scheme (SCSS) | 8.20% annually |

| RBI Floating Rate Savings Bond | 8.05% annually |

Bank Fixed Deposits: A safe investment option provided by banks, offering a guaranteed interest rate for a specified period.

Senior Citizen Savings Scheme (SCSS): A government-backed scheme designed for senior citizens, ensuring regular interest pay-outs.

RBI Floating Rate Bonds: Bonds issued by the government with interest rates linked to the National Savings Certificate (NSC) rate, offer biannual pay-outs.

Government-backed retirement schemes like SCSS are often preferred by senior citizens because they provide higher interest rates and strong capital safety.

These alternatives provide better returns and liquidity compared to the HDFC Life Smart Pension Plus Plan.

However, they lack inflation-adjusted income, which can only be achieved by incorporating equity into your portfolio.

A well-structured retirement portfolio usually combines multiple asset classes to balance income stability, growth potential, and liquidity needs.

HDFC Life Smart Pension Plus Vs. Inflation-adjusted income

Here’s a strategy that combines fixed-income instruments with equity to optimize returns and combat inflation, using the same ₹10 lakh corpus from the HDFC Life Smart Pension Plus example:

- Equity Allocation (₹6 lakhs): Generates wealth with an assumed return of 12%.

- Debt Allocation (₹4 lakhs): Provides regular income with an assumed return of 6%.

Such asset allocation strategies are commonly used in retirement planning to balance growth and income generation.

Strategy:

1. Withdraw an initial annual amount of ₹63,200, increasing it by 6% every 5 years to keep up with inflation.

2. Rebalance the portfolio every 5 years by replenishing the debt portion from equity growth.

3. Stop rebalancing at age 71(shift fully to debt).

Periodic portfolio rebalancing helps maintain the desired risk level while ensuring sustainable withdrawals during retirement.

Outcome:

By age 85, this strategy leaves a surplus corpus of ₹16.5 lakhs, significantly higher than the return of premium offered by the HDFC Life Smart Pension Plus Plan.

Benefits:

- Ensures regular income throughout retirement.

- Adjusts withdrawals to combat inflation, maintaining your lifestyle.

- Allows the retirement corpus to outlive you.

This type of systematic withdrawal strategy helps retirees generate inflation-adjusted income while preserving long-term wealth.

This approach demonstrates how a balanced allocation of 60:40 between equity and debt, with periodic rebalancing, can outperform fixed-return annuity plans.

Adjustments can be made to suit individual preferences and risk tolerance.

Different investors may adopt alternative retirement strategies depending on their risk tolerance, life expectancy assumptions, and income requirements.

Risks to Consider Before Buying HDFC Life Smart Pension Plus

Before choosing an annuity plan like the HDFC Life Smart Pension Plus, it is important to understand the potential risks and limitations associated with it.

One of the biggest concerns is inflation risk. Since the annuity amount is largely fixed for life, the purchasing power of the income can gradually decline over time as the cost of living increases.

What seems like an adequate monthly income today may not be sufficient after 10 or 15 years of retirement?

Another factor is lack of liquidity. Once a large portion of your retirement corpus is invested in an annuity plan, accessing that money becomes difficult.

Unlike other investments, you generally cannot withdraw the capital whenever needed.

There is also an opportunity cost involved.

By locking your funds into a fixed annuity, you may miss the chance to earn potentially higher returns through a diversified retirement portfolio that includes equity and other growth-oriented investments.

Therefore, while the HDFC Life Smart Pension Plus Plan offers stability and guaranteed income, investors should carefully evaluate these risks before committing a significant portion of their retirement savings to such products.

Final Verdict on HDFC Life Smart Pension Plus

The HDFC Life Smart Pension Plus offers a variety of annuity options for retirees, allowing flexibility in choosing features such as immediate or deferred pay-outs, single or limited pay, return or no return of premium, and single or joint life coverage.

These features make it a structured retirement income solution for individuals seeking guaranteed lifetime pension payments.

While these options may seem appealing, a closer examination reveals that the returns are typically more moderate than those of debt instruments.

While providing a steady income stream for life is a key feature, it shouldn’t be the sole factor in choosing the HDFC Life Smart Pension Plus.

The plan’s lack of liquidity and absence of inflation-adjusted income are major drawbacks that can erode the value of a fixed income over time and it also has a high agent commission.

Over long retirement periods, inflation can significantly reduce the real value of fixed pension income.

For regular income, retirees can explore other fixed-income securities that offer higher returns and greater liquidity.

To address inflation during retirement, incorporating equity into your portfolio is essential.

A diversified retirement portfolio that includes equity, debt, and income-generating assets can help maintain financial security throughout retirement.

When it comes to financial advice, are Quora, Facebook, and Twitter the final word?

Rather than relying on a one-size-fits-all annuity or pension plan, retirement planning should be personalized to align with individual needs and goals.

Consulting a Certified Financial Planner can help you craft a customized retirement portfolio that suits your risk tolerance and financial requirements.

Professional retirement planning ensures that investment strategies are aligned with longevity risk, inflation risk, and sustainable income needs.

Leave a Reply