ICICI Pru Wealth Builder II is a ULIP Policy with an attention-grabbing title and features such as it gives you the flexibility to choose your investment among 7 different investment options, apart from investment benefits, it also provides you bonuses if you stay invested for long term.

Now the point is, should you consider investing in this policy?

In this article, we will critically analyze its key benefits and overall outcome of this policy.

You will find everything you need to know about this policy, whether you should stay invested or cancel this policy.

If you are considering to buy this policy now, you will find out whether this is the right policy to buy or not!

So, read on and get the key insights of the ICICI Pru Wealth Builder Plan…

Please Note: UIN of the ICICI Pru Wealth Builder II is 105L139V01

Topic Navigation

1.) ICICI Pru Wealth Builder II Plan: How Does It Work?

2.) ICICI Pru Wealth Builder II Plan: Basic Features and Eligibility

3.) ICICI Pru Wealth Builder II Plan: Key Benefits

4.) Charges Under ICICI Pru Wealth Builder II Plan

5.) ICICI Pru Wealth Builder II Plan: Illustration

6.) ICICI Pru Wealth Builder II Plan: Analysis and Review

7.) Common Queries on ICICI Pru Wealth Builder II Plan

8.) Who Should Avoid ICICI Pru Wealth Builder II Plan?

ICICI Pru Wealth Builder II Plan: How does it work?

ICICI Prudential Wealth Builder II is a market-linked ULIP designed to combine life insurance with long-term wealth creation.

The final corpus depends on the performance of the underlying funds, making it important to understand the fund options, charges, and portfolio strategy before investing.

- Decide how much premium you want to pay and for how long?

- Select the Sum Assured as per your need

- Choose one of the 2 available Portfolio Strategies, which will be described in later sections…

- On maturity of the policy, a policyholder can receive the maturity benefit as a lump sum or as a structured pay-out.

- In case of unfortunate death of the policyholder during the policy term, his family will get the death benefit.

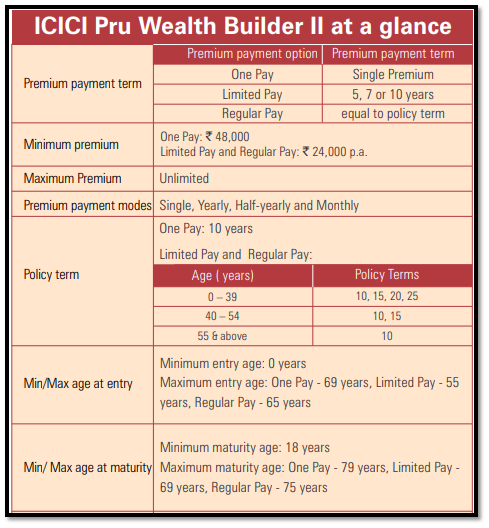

ICICI Pru Wealth Builder II Plan: Basic Features and Eligibility

Calculation of Sum Assured is shown below:

Calculation of Sum Assured is shown below:

Image Source: ICICI Pru Wealth Builder II product brochure

Before investing in the ICICI Wealth Builder Plan, ensure that the policy term, premium payment option, and sum assured align with your financial goals rather than selecting the plan solely based on projected maturity values.

ICICI Pru Wealth Builder II Plan: Key Benefits

1. This plan comes with 3 options: Single Pay, Limited Pay, and Regular Pay; as discussed in the eligibility criteria discussed in the earlier section.

2. Choice of portfolio strategies: Select a portfolio strategy of your choice among,

- Fixed Portfolio Strategy: Option to allocate your savings in the funds of your choice, OR

- Lifecycle based Portfolio Strategy: A unique and personalized strategy to create an ideal balance between equity and debt, based on your age.

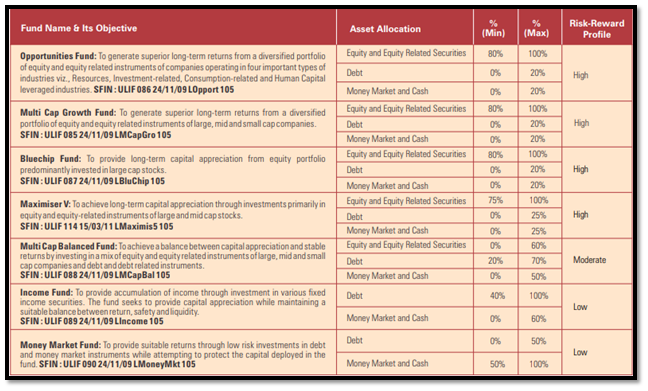

3. Multiple fund options: Invest in the funds of your choice from a diverse suite of 7 funds shown below: You can choose any fund out of above 7 based on the portfolio strategy you may choose among a fixed portfolio or Lifecycle based portfolio strategy.

You can choose any fund out of above 7 based on the portfolio strategy you may choose among a fixed portfolio or Lifecycle based portfolio strategy.

You will also get the option to switch your money between any fund anytime you need to.

The ICICI Pru Wealth Builder II fund options include equity, debt, and balanced funds.

Investors should review the historical performance of their chosen fund instead of assuming that past returns or NAV movements will continue in the future.

4. Loyalty additions and wealth boosters will be added to your fund value if you pay your premiums regularly and remain invested.

5. At the end of the policy term, you will receive your fund value.

6. You can choose to get your Fund value either as a lump sum or as a regular pay-out spread over time.

7. If the person whose life is covered in this policy dies anytime during the policy term, an insurance amount will be paid out to the nominee.

8. You will make partial withdrawals from your Fund Value after 5 years

Charges under ICICI Pru Wealth Builder II Plan

i. Premium Allocation Charge

Premium Allocation Charge depends on the premium payment option and the premium payment mode chosen. It is deducted from the premium amount at the time of premium payment and units are allocated in the chosen funds thereafter. This charge is expressed as a percentage of premium:

-

- One Pay option: 3%

A discount of 0.5% in the premium allocation charge is given to customers who buy directly from the Company’s website.

-

- Limited Pay and Regular Pay

A discount of 1% in the premium allocation charge in Year 1 is given to customers who buy directly from the Company’s website. All Top-up premiums are subject to an allocation charge of 2%.

A discount of 1% in the premium allocation charge in Year 1 is given to customers who buy directly from the Company’s website. All Top-up premiums are subject to an allocation charge of 2%.

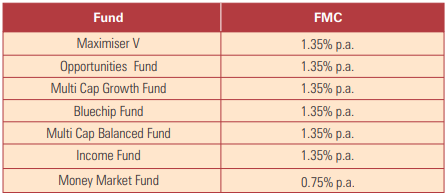

ii. Fund Management Charge (FMC)

The following fund management charges will be applicable and will be adjusted from the NAV on a daily basis. This charge will be a percentage of the Fund Value.

While comparing ICICI Pru Wealth Builder II with other ULIPs, always evaluate the total cost of ownership, including Premium Allocation Charges, Fund Management Charges, Policy Administration Charges, and Mortality Charges, as these directly influence long-term returns.

iii. Policy Administration Charge

The policy administration charge will be levied every month by the redemption of units, subject to a maximum of Rs.500 per month (Rs. 6,000 p.a.). The policy administration charge will be as set out below:

One Pay: Rs. 60 p.m. (Rs. 720 p.a.) for the first five policy years

Limited Pay and Regular Pay:

iv. Mortality Charges

Mortality charges will be levied every month by the redemption of units based on the Sum at Risk.

-

- For all One Pay policies and Limited Pay and Regular Pay policies with age at entry greater than or equal to 50 years

- Sum Assured, including Top-up Sum Assured, if any (reduced by applicable partial withdrawals),

- Fund Value (including Top-up Fund Value, if any), Minimum Death Benefit Less

- Fund Value (including Top-up Fund Value, if any)

For Limited Pay and Regular Pay policies with age at entry less than 50 years

The sum at Risk = Higher of,

- Sum Assured, including Top-up Sum Assured, if any

- Minimum Death Benefit

Indicative annual charges per thousand life cover for a healthy male and female life at a Sum Assured of Rs. 10 lakh are as shown below: Please note:

Please note:

- If the Life Assured is female the mortality charge for a male life two years younger will apply.

- Smokers may be charged extra mortality charges as per our underwriting guidelines.

- Sub-standard lives may be charged extra mortality charges as per our underwriting guidelines.

Insight: As you can see, these are the expenses being deducted from your policy annually. These are the charges which you cannot get rid of if you choose this policy. These charges will balance out whatever returns you may get through this plan.

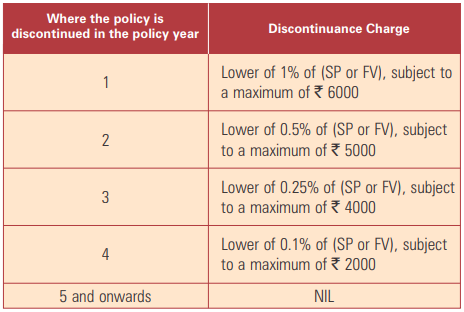

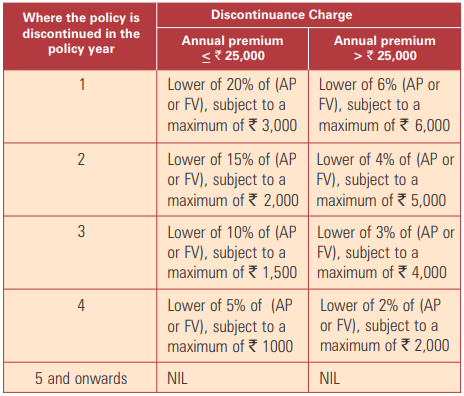

v. Discontinuance Charges

For One Pay policies: For Limited Pay and Regular Pay

For Limited Pay and Regular Pay

Where, AP: Annualised Premium; SP: Single Premium FV: Fund Value including Top-up Fund Value, if any, on the Date of Discontinuance No Discontinuance Charge is applicable for Top-up premiums.

ICICI Pru Wealth Builder II Plan: Illustration

Let’s take an example to understand the returns from this policy. Below are the assumptions:

Let’s say Mr. X is 35 years old and he wants to invest Rs. 50,000 p.a. Policy Term is 20 years.

He is choosing the assured sum of Rs. 5 Lacs. That is if nothing happens Mr. X will get his assured sum.

Note that 100% of the investment is done in the Maximizer V fund, out of the 7 available investment options.

Now let’s consider 2 cases, in the first case Mr. X is paying the premium for the first 5 years, that is, 5 years of Premium Payment Term.

And, in the second case, the premium payment term is equal to the policy term of 20 years.

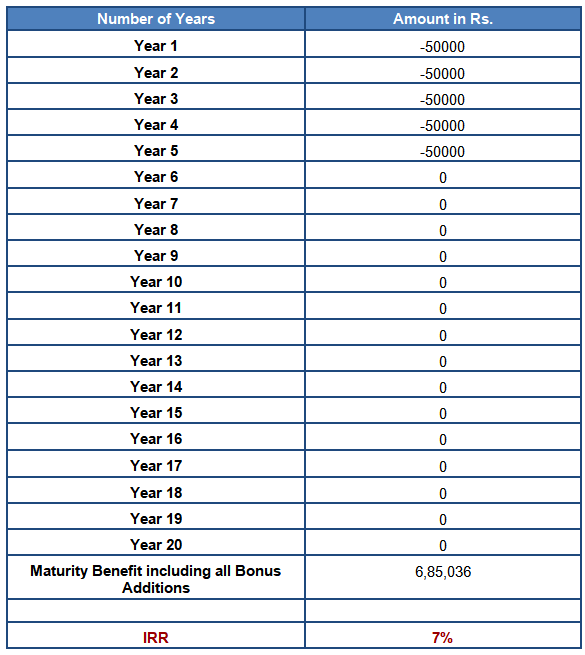

Case 1: 5 years of Premium Payment Term

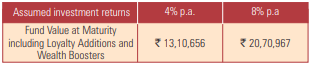

If Mr. X invests Rs. 50,000 per annum for the first 5 years, he may get the maturity value of:

-

- Rs. 6,85,036 in the best-case scenario, that is, when the company is getting 8% returns from the fund, you may get Rs. 6,85,036 including all Loyalty Additions and Wealth Boosters.

- Rs. 3,25,463 in the average-case scenario, that is when the company is getting 4% returns from the fund, you may get Rs. 3,25,463 including all Loyalty Additions and Wealth Boosters.

- Both of the returns are NON-GUARANTEED!

- The highlighted amount does NOT include the charges and expenses that you pay in this policy and are being deducted from your premiums.

Case 2: Premium Payment Term equals to the Policy Term of 20 years

However, in case Mr. X invests Rs. 50,000 per annum for the entire Policy Term of 20 years, he may get the maturity value of:

- Rs. 20,70,967 in the best-case scenario, that is, when the company is getting 8% returns from the fund, you may get Rs. 20,70,967 including all Loyalty Additions and Wealth Boosters throughout the policy term of 20 years!

- Rs. 13,10,656 in the average-case scenario, that is when the company is getting 4% returns from the fund, you may get Rs. 13,10,656 including all Loyalty Additions and Wealth Boosters.

- Both of the returns are NON-GUARANTEED!

- The highlighted amount does NOT include the charges and expenses that you pay in this policy and are being deducted from your premiums.

ICICI Pru Wealth Builder II Plan: Analysis and Review

In this section let us find out the returns that you may get from this plan based on the illustration that we have already discussed in the previous section.

Case 1: Average returns for 5 years Premium Paying Term

In this case, Mr. X is paying his premiums of Rs. 50,000 for 5 years, the Policy Term is 20 years. And, during the Maturity period, he is receiving the non-guaranteed benefits of Rs. 6,85,036/-, which includes Loyalty Additions and Wealth Boosters.

Let us calculate the average returns of all these pay-ins and pay-outs. It is shown in the table below: Mr. X is getting 7% average returns from this policy when he pays Rs. 50,000 for 5 years’ duration in the policy term of 20 years. An in-depth analysis of these returns is given after the description of Case 2!

Mr. X is getting 7% average returns from this policy when he pays Rs. 50,000 for 5 years’ duration in the policy term of 20 years. An in-depth analysis of these returns is given after the description of Case 2!

Case 2: Average Returns for the Premium Paying term equals to Policy Term

In this case, Mr. X is paying his premiums of Rs. 50,000 for the entire Policy Term of 20 years.

And, during the Maturity period, he is receiving the non-guaranteed benefits of Rs. 20,70,967/-, which includes Loyalty Additions and Wealth Boosters.

Let us calculate the average returns of all these pay-ins and pay-outs. It is shown in the table below: Mr. X is getting 7% average returns from this policy when he pays Rs. 50,000 for 20 years’ duration; that is, throughout an entire 20 years policy term. In-depth analysis of these returns is given below:

Mr. X is getting 7% average returns from this policy when he pays Rs. 50,000 for 20 years’ duration; that is, throughout an entire 20 years policy term. In-depth analysis of these returns is given below:

Following Insights are drawn from the above analysis:

1. As you can notice that Mr. X is receiving the average returns of 7% in both cases, it is considered under the best-case scenario. That is, Mr. X may get 7% returns only if the company gets 8% returns from the market and these are not guaranteed returns!

2. Returns are considered only if you choose to put 100% of your investment in the Maximizer V option, and the returns exclude the hefty charges that you pay to the company. And these returns changes with time.

Investors should distinguish between gross fund performance and the actual returns received after deducting all applicable charges throughout the policy term.

3. There is no transparency in the calculation of the Maturity Amount provided by the product brochure of the ICICI Pru Wealth Builder II Plan.

4. Overall this ULIP follows the complex procedure of giving you the returns. Once you invest in this policy you will have zero control over your money and you will never know how much you return will you actually get from this plan!

5. Moreover, if there are better investment options available as an alternative to this plan, then why you should consider investing in this plan?

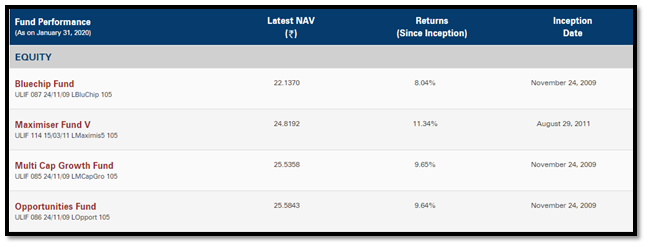

Before we get into the details into the alternative plan options; let’s have a look at the performance of various funds under the ICICI Pru Wealth Builder II Plan.

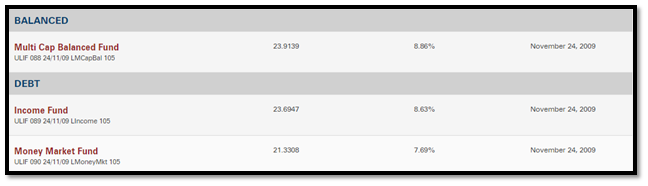

ICICI Pru Wealth Builder II Plan: Fund Performance as on 31st January 2023

As you can see from the above table, that the performance of all equity, debt and balanced funds have been good so far but it is NOT possible for you to get the returns at this rate!

As you can see from the above table, that the performance of all equity, debt and balanced funds have been good so far but it is NOT possible for you to get the returns at this rate!

You have to pay different kinds of charges under this policy as we have discussed in the earlier section.

The overall return you may get from this policy in the very best case scenario will not be greater than 6%, no matter what!!

Now let us look into the alternative plans versus ICICI Pru Wealth Builder II Plan.

Alternative Plans Vs. ICICI Pru Wealth Builder II Plan:

We recommend you to invest your money in PPF or Mutual Funds to get a better value of your money and secure your retirement life.

Below are the comparative details:

(i) PPF Vs. ICICI Pru Wealth Builder II Plan:

Let us say you are investing Rs. 50,000 per annum in PPF for 20 years, which gives you the guaranteed returns of 8%.

Therefore, after 20 years the returns from the PPF will be Rs. 24,71,146/-.

PPF Returns after 20 years: ₹ 24,71,146

Don’t you think, these guaranteed returns are far better than the best scenario’s non-guaranteed returns from ICICI Pru Wealth Builder Plan?

(ii) Mutual Funds Vs. ICICI Pru Wealth Builder II Plan:

In the case of Mutual funds, let’s say you invest Rs. 12,500 quarterly (or, Rs. 50,000 annually) through SIP payment in a good equity Mutual Fund that will generate 12% average returns.

You can use this Mutual Fund Online Calculator to find the Mutual Fund Returns.

After 20 years’ duration, the returns from Mutual Funds will be Rs. 41,37,549.

For conservative investors seeking predictable returns and capital protection, traditional fixed-income investments may offer greater simplicity and transparency than market-linked insurance products.

Mutual Fund Returns after 20 years: ₹ 41,37,549

Have you noticed it? You have the potential to grow your Rs. 50,000 per annum up to Rs. 41,37,549, if only you choose to manage your money wisely!

In ICICI Pru Wealth Builder II Plan the sole guaranteed benefit is Sum Assured, which is Rs. 5 Lacs only!

Along with your investment, we suggest you take up a separate Term Insurance Policy.

You can read this cheat sheet to select the best term insurance plan for you.

Also, have a look at our reviews on HDFC Life Click 2 Protect 3D Plus and ICICI Pru iProtect Smart Policy.

These articles will help you to choose a better Term Insurance Policy for you!

Let’s summarize their guaranteed returns through a table below:

Separating insurance from investments allows investors to choose better-performing investment products while purchasing adequate life insurance at a significantly lower cost through a standalone term insurance policy.

Common queries on ICICI Pru Wealth Builder II Plan

1. Is ICICI Pru Wealth Builder II, a good plan to buy?

No. you should avoid investing in ICICI Pru Wealth Builder II Plan. Instead, you must keep your investment and insurance as a separate policy.

2. If not ICICI Pru Wealth Builder II, where should I invest?

You should invest your money in Mutual Fund or PPF Scheme as an alternative to this plan. And, also take a Term Insurance as a standalone scheme.

3. How to cancel ICICI Pru Wealth Builder II?

There is a free-look period of 15 Days. However, if you want to discontinue your policy within 5 years, the Discontinuance Charges will be applicable as already discussed in this article. To surrender your policy, you can visit the nearest ICICI Prudential Life branch with the required documents.

Who Should Avoid ICICI Pru Wealth Builder II Plan?

This plan may not be suitable for investors looking for complete transparency, high liquidity, low-cost investing, or inflation-beating returns.

Individuals who prefer flexible investment options may find a combination of mutual funds and term insurance more suitable than combining insurance and investments in a single ULIP.

Conclusion

Now, we want you to answer why you are even contemplating to buy this policy? Or, stay invested in this policy?

Do you want flexibility in investment options?

Then go for Mutual Funds, there not only you will choose your preferred funds but also get much higher returns!

There you can cancel your investment ANYTIME you want!

Whereas in this ULIP your money is locked for 5 years!!

You can’t withdraw it before 5 years otherwise you have to pay a heavy penalty.

A financial product should be selected based on suitability for your financial goals rather than projected illustrations alone.

What are your other reasons which motivate you to invest in this plan? Let us know in the comment section.

Our advice for you is to keep your investment and insurance as a separate vehicle.

And, you should avoid investing in this ULIP and invest in a standalone Mutual Fund and Term Insurance separately.

If you have any more specific doubts or queries on this plan or any other experience to share regarding your take on this policy, share them in the comment section.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

I have started WB -II in 2014 with 50000 premium until 2018 and its maturity is Sep 2024. Now the market is positive. Shall I surrender and get the money or wait until maturity date. If I stay until end what will be the advantage. If I surrender and encash what will be the loss

I am holding icici wealth Builder 2 since 2016 return is showing 24% so what I should to do? I read your article then talk to icici representative they saying keep investing money will growth please sir suggest me my hard earn money

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the time, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

I agree, ICICI Pru Wealth Builder II is the worst plan. My wife had this fund enrolled in 2016 and has been paying Rs. 60000/- annually , present value of fund is Rs. 2,64,000/- returns are negative.

Best is to go with Mutual funds and online term insurance.

Thank you for sharing your experience with us.

I have a WB II policy term of 10 years and payment term of 5 years. I have already paid 4 years and last payment is to be made in December 2020. Should I make the last payment and wait till 2026 or discontinue the policy. I have paid Rs. 4.84 lakhs till now and fund value is Rs. 4.59 lakhs. I am confused what to do. Kindly advise.

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the time, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Thank you so much, I have been fooled by the icici, of course, and invested in the wealthbuilder2 for 5 years now. However, I’m thinking to withdraw the amount now. Since it been 5 years and my return is for now is 4%, fortunately. I won’t have to pay for the surrender fee. What do you think, is it a good time to withdraw the fund without thinking that I might get some more returns?

Worst investment ever though.

What will happen to my charges invested in mortality? Will I get the whole money back invested + interest at once? how about the mortality charge of around 20-30k. will they give me back?

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the time, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Mesmerized by the ICIC Prulife guys, I took a Policy of ICIC Pru Wealth Builder in the year 2015 at a premium of Rs. 100000. I sincerely continued to pay Rs. 100000 unitil 2019 (Rs. 500000) and as I was observing that this Rs. 500000 was not doing well (as I strongly believe the fund managers have not prudentially invested to take into consideration of poor investors objectives. As in the beginning of 2020 it was not doing well, I requested them what can be done. They said, I have to wait till 20 March 2020 if I have to cancel the policy or switch over to some other scheme. As I was not conviced with the ICICI guy on the line I cancelled the Policy and took Rs. 300000 and odd Rupees . Should I have waited for 10 years even this Rs. 300000 I would not have got though all the Gurus may suggest that it will pick up. As I had a doubt the ICIC Prulife guys are not a good fund managers as and when they see a downward trend they should chanage the portfoilos so as to ensure Investors benefit, but I think ICIC Prulife Guys (for Wealth Builder II Scheme) are not capable of and are only going to derail the Scheme and after 10 years from the date of Investment, they are going to keep the poor investors deceived. You will appreciate that, frequently they call the investor and advise tjhem, they may be calls to close the Policy but you do not budge to such callers, and having faith in such ICIC Prulife callers, we continue to pay premiums and end up with a loss. I sincerely seek you advise, whether these Schemes are really useful. Your prompt comments would be appreciated.

Thank you for sharing your experience with us.

Have invested in ICICI Prude Wealth Builder II and have paid four premiums. Have to pay the 5th premium. Is it worth to staying long in this or to withdraw. Advice.

It depends.

Please check with your financial planner.

You can also book a slot with our financial planner for an initial complimentary consultation.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

dear sir my plan is 60000/y and 5 premium 10 year term

i was invested 60000 /y and 4 premium i was completed if am not paid 5 th premium and what amount can i get after 5 year please give suggestion

Please check with your financial planner.

You can also book a slot with our financial planner for an initial complimentary consultation.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/