I see that you are in the middle of whether to buy the HDFC Life ClassicAssure Plus or not.

Or you could have already bought this insurance plan in hopes of good maturity benefits. But now you have a question.

You probably have researched a little about this insurance investment plan.

And you still haven’t gotten a definitive answer.

Worry no more, we’ve got you covered!

In this HDFC Life ClassicAssure Plus review, we’ll observe the pros and cons of this plan in detail.

Do you want to know if HDFC Life Classic Assure Plus is good or bad for you?

Let’s discover!

Table of Contents:

1. HDFC Life ClassicAssure Plus: An Overview

2. Key Features of HDFC Life ClassicAssure Plus

3. Benefits of HDFC Life ClassicAssure Plus

4. Claims & Promises of HDFC Life ClassicAssure Plus

5. Other Benefits and Bonuses of HDFC Life ClassicAssure Plus

6. HDFC Life ClassicAssure Plus Review—with Illustration

7. HDFC Life ClassicAssure Plus Plan Review And Comparison

8. How to Surrender Your HDFC Life ClassicAssure Plus Plan?

i) Steps to Surrender HDFC Life ClassicAssure Plus plan

ii) Alternate Way to Surrender the Policy

9. Verdict

HDFC ClassicAssure Plus: An Overview

HDFC Life ClassicAssure Plus is a simple traditional participating insurance plan—that has been in the market since 2013.

At maturity, the policy will pay the maturity benefits including Reversionary Bonus to the insured.

Or in case of an insured’s untimely demise, while the policy is in force, it will pay the death benefits to the nominee.

Let’s look at the policy details of HDFC Life ClassicAssure Plus before reviewing the advantages and disadvantages of this plan.

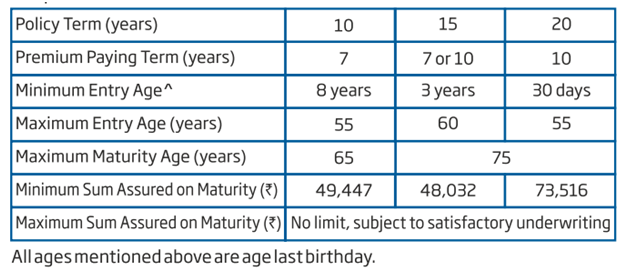

HDFC Life ClassicAssure Plus: Policy Details

The policy offers 3 different policy terms viz. 10, 15, and 20 years.

It also has 2 different Premium Paying Terms (PPT) which will be chosen based on the policy term. See the table below for threshold on age eligibility and Sum Assured, etc.

See the table below for threshold on age eligibility and Sum Assured, etc.

The HDFC ClassicAssure Plus plan offers limited flexibility in policy term and premium structure when compared with several newer HDFC Life traditional plans available today.

HDFC Life also offers Critical Illness Plus rider and Income Benefit on Accidental Disability rider as optional riders in this policy.

HDFC Life ClassicAssure Plus: Premium Details

The policy has four different premium payment frequencies and their respective minimum limits. See the table below.

Grace Period for Premium Payment: A 15-day grace period for the monthly premium payment option.

And a 30-day grace period for Quarterly, Half-Yearly, and Annual premium payment options.

Check out this HDFC ClassicAssure Plus PDF for the official latest brochure of the plan.

HDFC Life ClassicAssure Plus: Review of Benefits

There are only two different benefit options.

i) Maturity Benefits

On maturity of the HDFC Life ClassicAssure Plus, the policyholder will receive a Lumpsum of—Sum Assured + Bonuses—accrued over the policy term.

Most investors checking the HDFC Life ClassicAssure Plus maturity amount expect stable long-term returns, but the final pay-out depends heavily on bonus additions declared during the policy term.

ii) Death Benefits

In the event of the policyholder’s death, the HDFC Life ClassicAssure Plus will pay the nominee the highest of the following.

- Sum Assured on Death

- 10x Annualized Premium

- 105% of the Total Premiums Paid

It is, of course, assuming that the policyholder has paid the policy premiums without fail in both cases.

To calculate your premium and benefits, use the HDFC Life ClassicAssure Plus Calculator.

Besides these, the policy also makes some sincere claims and promises. Let’s analyse them.

HDFC Life ClassicAssure Plus: Claims & Promises

HDFC Life PROMISES a list of things with this insurance plan, stated as:

- Guaranteed Reversionary Bonus

- Short Medical Questionnaire (SMQ) instead of a comprehensive medical check-up.

- Flexibility to Choose Premium Paying Term (PPT)

- Protection Against Untimely Demise

- Ideal Plan for Meeting Long-Term Financial Goals

Is HDFC Life ClassicAssure Plus Reversionary Bonus Guaranteed?

Only 3% of the Sum Assured is guaranteed as a reversionary bonus. Everything over and above 3% is subject to change without notice.

See “Review of Guaranteed Benefits” under HDFC Life ClassicAssure Plus Review with illustrations topic shown below in the article.

The HDFC Life bonus chart and bonus rate history show that non-guaranteed reversionary bonuses can vary significantly across years depending on insurer performance.

Is it true that the HDFC Life ClassicAssure Plus plan does not require a medical check-up?

Yes. But, it is only for buyers between the ages 18 and 50, with Sum Assured proposals only up to ₹20 Lakhs.

Although, buyers still have to answer a Short Medical Questionnaire (SMQ) instead of a medical check-up.

Based on your answers to the SMQ, the insurer may request you to undergo a medical check-up.

Is it okay to purchase this policy by answering a questionnaire alone?

Answering the SMQ may be enough to purchase the policy.

But in case of a death claim, it could become problematic.

Medical Questionnaire leaves an ambiguous area where HDFC Life could challenge the death benefit claim. Since there was no comprehensive medical check-up, the claim rejection probability is always high.

Please take a look at the HDF Life ClassicAssure Plus PDF of SMQ here.

How flexible is the Premium Paying Term of HDFC Life ClassicAssure Plus plan?

As seen under the Policy details section, the policy provides only two different premium paying terms. Even that is available only for a policy term of 15 years.

As for protection against untimely demise and long-term financial goals, it requires detailed analysis.

See the HDFC Life ClassicAssure Plus Review with the illustration shown below. But before that, there are other claimed benefits too.

HDFC Life ClassicAssure Plus: Other Benefits and Bonuses

i) Discount Benefits on Policy Premium

A 5% discount on the premium would be offered if the Sum Assured is set at ₹10 Lakhs or higher.

It excludes rider premium, policy fee, and other charges.

ii) Loan Benefits on Premiums Paid

You may avail a loan on your policy for up to 80% of its Surrender Value.

To avail of this feature, you have to be 18 years old or higher and the policy has to be in force.

However, you will be charged interest at the rate of 14%.

Bonuses in HDFC Life ClassicAssure Plus

i) Reversionary Bonus

It has a Guaranteed Reversionary Bonus and Non-Guaranteed Reversionary Bonus. The table below highlights the HDFC Life ClassicAssure Plus Bonus Rate History.

According to Bonus Rate History, if 3% of the Sum Assured of your policy is guaranteed as Reversionary Bonus.

And, If the Sum Assured is ₹10 Lakhs then, Bonus Amount = 10 Lakhs x 3% = ₹30,000/Annum

The guaranteed reversionary bonus will be the same for every year. The guaranteed reversionary bonus will not compound with the Sum Assured.

The Non-Guaranteed Reversionary Bonus rate will be declared and added at the end of every financial year.

ii) Terminal Bonus

HDFC Life has not declared anything about terminal bonuses or any other bonuses apart from the Reversionary Bonuses.

Hence, policyholders should not expect any bonuses other than the guaranteed and non-guaranteed reversionary bonuses.

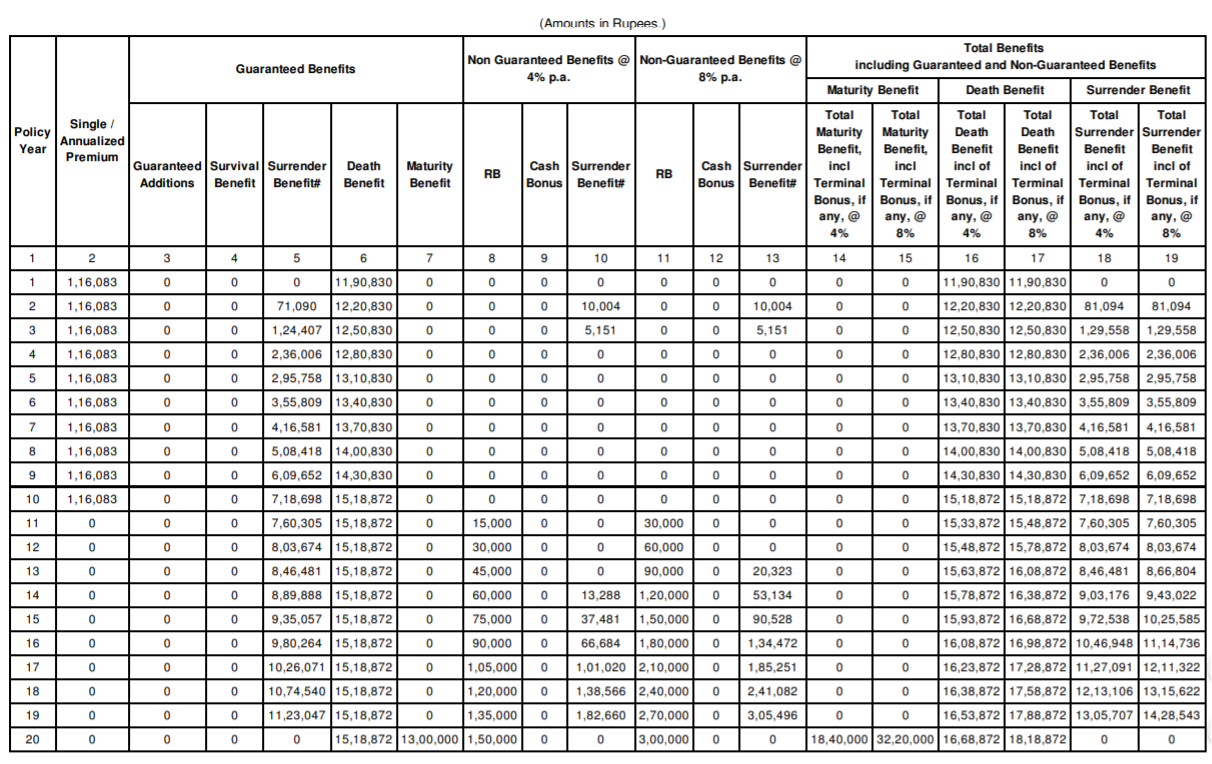

HDFC Life ClassicAssure Plus Review: with Illustration

To review the total Maturity Benefit or actual returns from HDFC Life ClassicAssure Plus we have to consider 3 different components:

1.) Review of Sum Assured on Maturity

Let’s assume you’re a 30-year-old buying the HDFC Life ClassicAssure plus.

For maximum benefit, we shall take the Policy Term and Sum Assured as 20 Years and ₹10 Lakhs respectively.

In that case, the basic features of your policy would look like, Let’s see the illustration provided by HDFC Life for this policy plan.

Let’s see the illustration provided by HDFC Life for this policy plan.

2.) Review of Guaranteed Benefits

The policy provides a guaranteed maximum life cover of ₹15.18 Lakhs in the later years of the policy.

And as promised, the policy also gives the guaranteed 3% reversionary bonus (RB) on the sum assured at maturity.

However, the guaranteed bonus added only for Premium Paying Term, year after year does not compound.

Hence the maximum guaranteed maturity benefit is severely reduced. That is,

Effectively, the return rate for the guaranteed benefits is 1% p.a.

Yet, the policy’s illustration suggests a higher maturity benefit including the non-guaranteed benefits.

Even though the HDFC Life ClassicAssure Plus benefits include guaranteed additions, the overall maturity value remains relatively low after considering the long policy duration.

3.) Review of Non-Guaranteed Benefits

The illustration table shows two different non-guaranteed benefits at a gross return rate of 4% and 8% per annum.

The ideal best-case scenario is a gross return of 8% per annum.

The real rate of return after subject to different charges will be much less in the hands of investor. We will calculate it in the following section.

However, over the years, HDFC Life ClassicAssure Plus has shown gross returns even much lesser than 8% per annum. It means the effective return in the hands of investors have been even lesser.

A table of Non-Guaranteed Benefits return rate over the years is shown below. Despite the past poor records, let us consider the best-case scenario!

Despite the past poor records, let us consider the best-case scenario!

The HDFC Life ClassicAssure Plus returns calculator illustrations appear attractive initially, but the effective return in the hands of investors is often much lower than projected figures.

Total Benefits Review: Effective Internal Rate of Return

The total maturity benefit has three different components.

They are Sum Assured on Maturity, Guaranteed benefits and the Non-guaranteed benefits.

The reversionary bonuses, both Guaranteed Bonuses and Non-Guaranteed Bonuses, are added only as a simple reversionary bonus. That is, you lose the power of compounding.

Let’s find out the effective rate of return(IRR) of the HDFC Life ClassicAssure Plus plan in the hands of an investor.

See the IRR calculation table below, with the data from the illustration table.

A 6.69% return for 20 long years—even after making positive assumptions for the non-guaranteed reversionary and terminal bonuses.

It will fall even further if we take away all the positive assumptions.

This is why many investors reviewing HDFC Life ClassicAssure Plus today compare it with alternatives like PPF, ELSS mutual funds, or other long-term investment products before committing.

What are the positive assumptions we made?

- We assumed the best case 8% return rate from the illustration.

- Even though the records show that the policy returns is only 4.5% at best.

- No transparency was shown regarding how the Guaranteed Bonus is added.

- Only ₹3 Lakhs was shown in the illustration when it is supposed to be ₹6 Lakhs of Guaranteed Bonus.

- We have assumed GST-free premiums and have not considered a total of ~₹30,000 paid as GST @2.5% on premium as an expense.

It is now evident that the cons of HDFC Life ClassicAssure Plus outweigh its pros.

Do you think it is worthy of your time and energy to invest in such a low return investment?

But again, is there a better investment?

You probably are already aware of other investment instruments like PPF and Mutual Funds.

How do they stand against this HDFC Life ClassicAssure Plus plan?

Will it make a difference in the returns?

Let’s explore both alternatives in detail to help you get better clarity.

HDFC Life ClassicAssure Plus Plan Review and Comparison

Let’s make it a fair comparison battle in this HDFC Life ClassicAssure Plus Review and Comparison.

The policy’s premiums and benefits are exempt from income tax under sections 80C and 10(10D) of the IT Act, 1961 respectively. Therefore,

- PPF offers a unique EEE tax exemption.

- Mutual Fund offers tax deduction under section 80C in ELSS investments.

- However, ELSS Mutual Funds redemptions are levied LTCG @ 10% over and above ₹1 Lakhs.

- So we’ll deduct 10% LTCG in this Mutual Fund comparison, too.

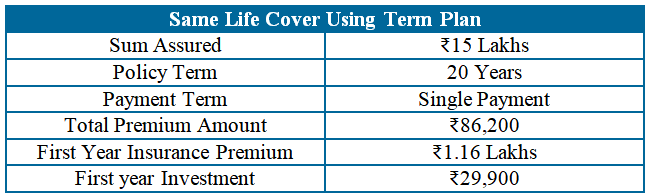

HDFC Life ClassicAssure Plus also offers a life cover of ₹15 Lakhs.

Hence, Now the ground is level with,

Now the ground is level with,

- Same Tax Benefits

- Same Life Cover

- Same Policy & Investment Term

- Different Investment Instruments

Do you want a life coverage along with investment benefits?

Purchase a term life insurance policy. It will provide you with better life coverage at a lower premium.

All that is left to compare is only the investment returns. Let’s put all the cards on the table

i) HDFC Life ClassicAssure Plus Comparison with PPF

As seen in the HDFC Life Classic Assure Plus Plan Review above, we’ll take the same investment parameters for comparison.

The interest rate of PPF for Q4 2025-26 is 7.1% p.a. Here is the plan’s comparison with PPF.

What does the comparison table tell us?

It is understandable that you, as an investor, would want some assurance on investments.

In such a case, there is the PPF investment for risk-averse investors.

It has the lowest risk; there is no risk of capital loss. The returns of PPF are assured.

Also, it has a lock-in period of only 15 years. You can even take a loan or make partial withdrawals after the completion of 5th year.

- Better liquidity

- Better assurance by Govt. of India

Still, PPF delivers almost ₹18 Lakhs more than the HDFC Life ClassicAssure Plus plan in the form of Guaranteed Returns.

For a conservative investor, PPF + Term Insurance proves to be a better alternative than HDFC Life ClassicAssure Plus.

For investors prioritizing capital safety and guaranteed growth, PPF continues to offer stronger long-term value compared to many traditional participating insurance plans.

But what if you could learn to manage risks?

What if you could work on and improve your risk tolerance?

HDFC Life ClassicAssure Plus Review and Comparison with Mutual Funds

The best performing ELSS Mutual Fund has given a return of more than 17% p.a.

However, considering the risks involved we are going to assume a conservative 12% in this review and comparison.

See the table below for the potential return on investment in ELSS Mutual Funds for the same investment parameters. Even though the assumed rate of return is 12%, the LTCG tax @ 10% would have reduced the real return.

Even though the assumed rate of return is 12%, the LTCG tax @ 10% would have reduced the real return.

Only an IRR calculation will show the real rate of return for this ELSS investment.

See the IRR table below.

An IRR of 11.07% from ELSS investment is a sure winner against the best-case scenario 6.69% IRR of HDFC Life ClassicAssure Plus.

This is the return an average performing Mutual Fund can offer, after deduction of LTCG tax.

Even better, it offers better liquidity on investments. ELSS Mutual Funds have a lock-in period of only 3 years, whereas the ClassicAssure Plus plan has a minimum of 10 years.

- Better liquidity

- Better Regulation by SEBI

- Better Transparency

- Extremely better returns

You only have to learn how to manage risks and become a real investor.

Invest in ELSS Mutual Funds if you want to invest for the long term and get higher returns.

The comparison becomes even more relevant for investors focused on wealth creation, because long-term equity investments historically delivered higher inflation-adjusted returns than traditional insurance products.

When it comes to life insurance, Term Insurance is the way to go.

But what if you have already invested in such a poor insurance investment?

If you have, you can always fix this terrible investment mistake. Check out:

Common Reasons Why Investors Cancel HDFC Life ClassicAssure Plus Policies

Many policyholders surrender or discontinue the HDFC Life ClassicAssure Plus plan after realizing that the actual returns are much lower than expected.

Long lock-in periods, limited liquidity, low effective compounding, and dependence on non-guaranteed bonuses are some of the most common reasons behind policy cancellation.

Some investors also shift towards alternatives like PPF, mutual funds, or term insurance after comparing the maturity amount, surrender value, and long-term wealth creation potential of the policy.

How to Surrender /Cancel HDFC Life ClassicAssure Plus Plan?

Surrender During Free-look Period:

If you have just bought this insurance plan, I believe you are already aware of the ‘free-look period’ of 15 days from the receipt of the policy.

IRDAI gives the policyholders the right to cancel their policy with a full refund of any premium paid during these 15 days.

The ‘free-look period’ is 30 days if the policy was bought online.

Surrender After Free-Look Period:

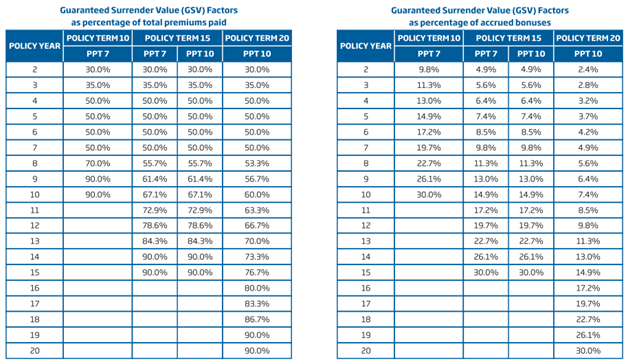

If you miss the free-look period, you can always surrender your HDFC Life ClassicAssure Plus policy.

However, your policy will begin to have any surrender value only after paying the second year’s premium.

The total guaranteed surrender value will be the sum of the stated percentage of total premiums paid and the percentage of accrued bonuses.

See the table below for the different surrender value percentages of the policy. Once you have accepted the fact that HDFC Life ClassicAssure Plus is a lousy investment instrument, it is best to surrender it as soon as possible.

Once you have accepted the fact that HDFC Life ClassicAssure Plus is a lousy investment instrument, it is best to surrender it as soon as possible.

Even if it seems to incur a loss on the investment, the higher returns from other investment instruments will offset any loss.

Not just that, but the sooner you reinvest, the higher your return on investment will be.

It is a compelling reason to surrender your HDFC Life ClassicAssure Plus plan at the first opportunity.

Before surrendering, many policyholders check the surrender value of HDFC Life policy to understand how much of their paid premiums and bonuses can actually be recovered.

Steps to Surrender/Cancel HDFC Life ClassicAssure Plus plan

Step 1: Fill out the Mandate Deactivation Request form.

You may download and print the HDFC Life ClassicAssure Plus Brochure for the same here.

Or you can just walk into the nearest HDFC Life branch for the same.

Step 2: Submit the filled form at the HDFC Life branch.

Step 3: Once the request is processed, your HDFC Life ClassicAssure Plus plan will be terminated and the surrender value, if any, will be paid.

Policyholders can also track HDFC Life ClassicAssure Plus policy status online using their policy number before initiating the cancellation or surrender request.

An Alternate way to Surrender/cancel HDFC Life ClassicAssure Plus

Send an email to service@hdfclife.com requesting the mandate cancellation.

It is advisable to mention the appropriate Surrender Value in the cancellation request email.

Indicate the ‘free-look period’ for a full refund (minus processing charges) in case of cancellation during the free-look period.

Note: You should submit the cancellation request at least 15 days before the premium due date.

If your surrender value is high—say ₹2 lakhs or more—you may find it difficult to reinvest it optimally.

It is recommended you consult an investment advisor before you reinvest for tax optimization.

HDFC Life ClassicAssure Plus: Final Review

Is the HDFC Classic Assure Plus plan good or bad to invest in?

After analyzing the features, Returns, and alternatives of HDFC Life ClassicAssure Plus, we have come to a conclusion that,

DO NOT INVEST in this HDFC Life ClassicAssure Plus plan if you care about wealth creation.

Extremely high Agent Commissions and charges restrict these insurance policies from generating returns similar to PPF or Mutual Funds.

If you are serious enough about achieving your financial goals through wealth creation, what you need is a Financial Plan—not an insurance plan.

Like this review?

Spread the awareness—share it with your family and friends.

Ultimately, if you want to take control of your financial life,

Sign-up for a free 30-minute consultation with a Certified Financial Planner now! Register below.

Clear explanation thank you!

I have HDFC life classic assure Plus plan.

10 years term

7 years premium paying term

Per year i pay 40900 for 7 years

I have already paid 5 premium and now only 2 premium less.

What am I do?

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the time, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

I had taken this policy in 2013 ,paid 50k as premium and forgot abt it .i have recd a call giving me 3 options of what to do .tge 3rd option is to pay 50k & after 3 months get 224740/- as my policy money has grown to 124740/-. Is this correct information & should i go for it

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the time, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

i purchased Classic Assure Plus(CAP) in 2014. the sales agent Prashant Mataskar in HDFC prabhadevi, mumbai branch gave me all false promises. he told me the returns would be better that Fixed Deposit. In 2014 FD was 9% interest rate. My experience after 7 years of premium paying term this plan is a fraud by hdfclife. i paid 1 lakh each year for 7 years that totals 7 lakhs as of now but the value of this investment is 5,61,400. the annual bonus Rs 13,9000. Another 3 years will be total 6lacs. So this CAP is case of cheating and fraud product. don’t ever buy from HDFCLife.

Thank you for sharing your experience.

Same thing happened with. The sales agent gave me all false promises. he told me the returns would be better that Fixed Deposit. when i questioned about illustration & sum assured as in policy document, he said its just illustration. In actual, you will get higher amount. he said I will get minimun 8,00,000/RS and in best case scenario, I will get 10,00,000/ RS after 10 years. I have taken this policy in 2017 & already paid 7 EMIS’ each of 49200/ total to 345000/. As per customer care, I will get ~350000/ Rs after 10 years maturity. If I will surrender it now, I will get only 2,00,000/ RS. This is a cheating from HDFCLife. can we file a complain against HDFCLife agents for misguiding customers.

Hi, i took this hdfc life classic assure plus plan 1.9 years back of annual premium 24,540 for 7 years and maturity 10y, and 2 years of lock in period. Where i only paid 1year premium of 24,540 and now its in lapse status and i want to surrender and lock in period end on 01/10/21. What should i do at this point, kindly help.

Since you have already taken this insurance plan, you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the times, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here!

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Love your explanations…. really very good and helpful.

Glad to help you!

Hi ..

Thank you for providing such a clear explanation. I too having the same policy and now I worried to continue this policy. so can you suggest me whether it is better to surrender this policy now or is there any way that we can approach to get back at least the paid premium.

Premium – 5000 per month

Duration – 10 year plan (7 year premium paying term)

2 year 6 month completed

Since you have already taken this insurance plan, you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the times, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here!

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

A well detailed review, helps a lot to make a decision. Thanks much

You are welcome

i am paying 12k premium per annum ,i am considering to surrender this plan after completion of 2 years — i want to know how much would i get in hand approximately,i am confused how to calculate this amount.thanks

You will get 30% of your premium paid as GSV.