SBI Shubh Nivesh is an endowment policy, it provides a unique feature of whole life coverage.

The company also claims to provide you with attention-grabbing features such as regular income, multiple benefits of wealth creation, insurance cover, and wealth transfer.

What does this policy have in its basket? Will you get any benefit if you choose to invest in this plan? If you have already taken this policy, should you stay invested in this policy?

In this post, we will critically review its key features and benefits, that will answer all your questions and help you make the right buying decision.

Table of Content:

1.) SBI Shubh Nivesh Plan: Key Highlights – Review

2.) SBI Shubh Nivesh Plan: Analysis of Basic Features and Eligibility

3.) SBI Shubh Nivesh Plan: Review of Maturity Benefits

4.) Documents Required to Buy SBI Shubh Nivesh Plan: A Quick Checklist

5.) SBI Shubh Nivesh Plan: Review of Death Benefits

6.)SBI Shubh Nivesh Plan: Review with Illustration

7.)SBI Shubh Nivesh Plan: Analysis and Review

- SBI Shubh Nivesh Plan (2020 update): Past Performance Review with Illustration

- SBI Shubh Nivesh Plan Vs. Other Alternative Investments Review

- SBI Shubh Nivesh Plan vs SBI Life Smart Privilege Plan

- SBI Shubh Nivesh Plan vs other Investment Plans – Review Conclusion

8.) Limitations of SBI Shubh Nivesh Plan: Analysis

9.) SBI Shubh Nivesh Plan: FAQs

10.) Conclusion: SBI Shubh Nivesh Plan Good or Bad?

SBI Shubh Nivesh Plan: Key Highlights -Review

The SBI Life Shubh Nivesh Plan is designed for individuals seeking a combination of life insurance protection and long-term savings through an endowment-based solution.

- You will have the option of choosing the Life Cover for 30 years OR the whole life depending on your insurance needs.

- Flexibility to choose between Single and Regular Premium Payment.

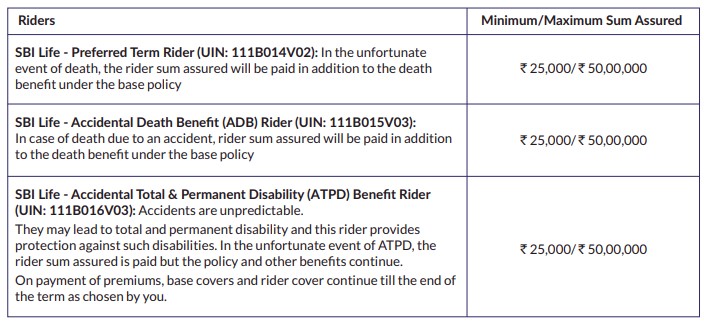

- Additional Rider options are available at an affordable cost. Details are shown below:

- This plan comes with 2 options: An endowment option, and Endowment with a whole life option.

Before investing, it is important to understand the SBI Shubh Nivesh plan details, benefits, maturity value, and surrender provisions to evaluate whether the plan aligns with your financial goals.

Endowment Option:

Under this option, the Sum Assured + accrued Simple Reversionary Bonus would be paid on the death of the Life Insured within the Policy Tenure as Death Benefit or on survival till the end of the Policy Tenure as Maturity Benefit.

This structure makes the plan similar to a traditional SBI Life Shubh Nivesh Endowment Plan, where policyholders receive insurance coverage along with guaranteed benefits and declared bonuses.

Endowment with whole life option:

Under this option, the policy is converted to a whole life cum Endowment Plan.

Thus, the Sum Assured + accrued Simple Reversionary Bonus would be paid at the end of the Endowment Tenure and the policy continues.

An additional amount of the basic Sum Assured will be paid on survival till 100 years of age or on the death of the Life Assured, whichever is earlier.

The SBI Shubh Nivesh Whole Life Plan may appeal to investors looking for lifelong protection while preserving a legacy for future generations.

Income Tax Benefit:

Life Insurance premiums paid up to Rs. 1,00,000 are allowed as a deduction from the taxable income each year under section 80C and the Maturity Proceeds are tax-free under section 10(10) D subject to fulfilment of terms and conditions.

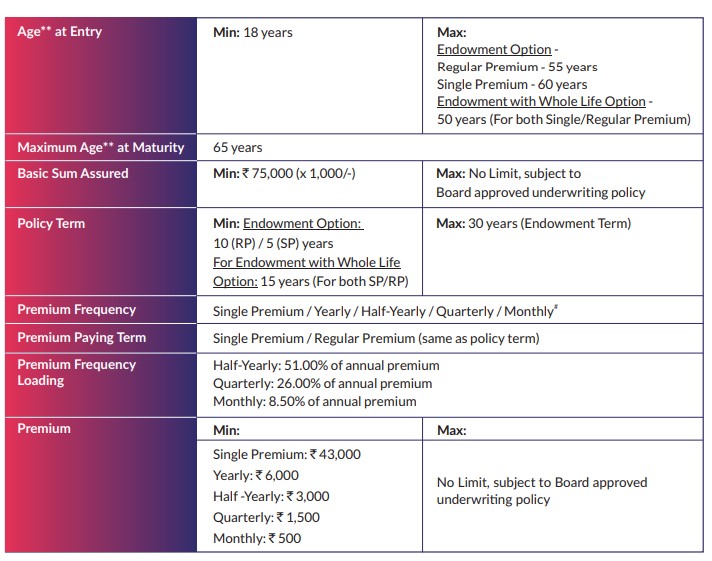

SBI Shubh Nivesh Plan: Analysis of Basic Features and Eligibility

All the basic features of this plan such as Policy Term, Premium frequency, Premium paying term, Premium option etc. are shown in the table below.

Documents Required to Buy SBI Shubh Nivesh Plan: A Quick Checklist

Before purchasing the SBI Life Shubh Nivesh Policy, you should keep the necessary documents ready to ensure a smooth application process.

Typically, the insurer may require:

- PAN Card

- Aadhaar Card or any valid address proof

- Recent passport-size photograph

- Identity proof (Passport, Voter ID, Driving Licence, etc.)

- Income proof (for higher sum assured amounts, if applicable)

- Bank account details for premium payments and policy servicing

The exact documentation requirements may vary depending on the applicant’s age, sum assured chosen, underwriting requirements, and prevailing regulatory guidelines.

It is advisable to verify the latest requirements with SBI Life Insurance before submitting the proposal form.

SBI Shubh Nivesh Plan: Review of Maturity Benefits

On survival till the end of the policy tenure, the policyholder will get the Maturity Benefits according to the chosen plan:

Endowment Assurance: Analysis

- After completion of Policy Tenure, the Basic Sum Assured + vested Simple Reversionary Bonus is paid as Maturity Benefit and the policy terminates

- If the Deferred Maturity Payment option has been chosen, the accrued bonus will be paid on the date of policy maturity and the policyholder may choose to receive the sum assured in regular instalments over the next 5/10/15/20 years as selected

Whole Life Endowment Assurance: Analysis

- After completion of the endowment term, the Basic Sum Assured + vested Simple Reversionary Bonus and Terminal bonuses are paid as Maturity Benefits, provided that the policy is in force.

- If the Deferred Maturity Payment option has been chosen, the accrued bonus will be paid on the date of policy maturity and the policyholder may choose to receive the sum assured in regular instalments over the next 5/10/15 or 20 years, as selected

- An additional amount equal to the basic sum assured will be paid on the attainment of the 100th Birthday!!

Those comparing SBI Life Endowment Plans often evaluate this option because of its combination of maturity benefits and lifelong coverage.

SBI Shubh Nivesh Plan: Review of Death Benefits

In case of the death of the Policyholder within the Policy Term, the nominee will get the death benefits according to the opted plan.

Endowment Assurance:

- Death before the completion of Policy Tenure: Sum Assured + Simple Reversionary Bonus (if any) is paid to the nominee as Death Benefit and the policy terminates

- The deferred Maturity Payment Option has been opted for and death happens after the completion of the Endowment term: The Balance amount of the Deferred Maturity Payment Option, if any; would continue to be paid to the legal heirs till the end of the stipulated chosen period.

Whole Life Endowment Assurance:

- Death before the completion of the Endowment term: Sum Assured + Simple Reversionary Bonus (if any) is paid to the nominee as Death Benefit and the policy terminates

- If the death happens after the completion of the endowment term and up to 100 years of age: Basic Sum Assured is paid to the nominee as Death Benefit and the policy terminates

- If the deferred Maturity Payment Option has been opted for and death happens after the completion of the Endowment term but before the receipt of the final instalment under the deferred payment option.

- The Basic Sum Assured would be paid to the nominee as Death Benefit and the policy continues. The remaining amount of the Deferred Maturity Payment Option would continue to be paid to the nominee till the end of the stipulated period as chosen.

The death benefit structure of SBI Life Shubh Nivesh Policy ensures that the nominee receives financial support even if the policyholder passes away during the policy term.

SBI Shubh Nivesh Plan: Review with Illustration

Let us say, Mr X who is 30 years old; chooses to purchase Endowment with a whole life option in SBI Shubh Nivesh Plan.

After putting all the relevant details, such as Sum Assured, Premium Frequency, Policy Term and Premium Payment Term on the SBI Life Online Calculator:

|

Male |

35 years |

|

Sum Assured |

₹ 20,00,000 |

|

Policy Term |

25 years |

|

Premium Paying Term |

25 years |

|

Annualised Premium |

₹ 89,160 |

From the Calculator, we have found that

– To get the Sum Assured of Rs.20 Lacs, Mr X has to pay the annual Premium amount of Rs. 89,160 for 25 years.

– Maturity Benefits (after 25 years) will be Rs.24,47,500 when assumed at the gross return rate of 4%. And Rs.45,30,000 in the best-case scenario considered at 8% Assumed return rate.

Note that we have not considered the additional riders in this calculation.

Watch the visual illustration below!

Many investors use an SBI Shubh Nivesh Maturity Calculator Online to estimate the expected maturity proceeds based on the premium amount, policy term, and chosen plan option.

Insight:

The additional riders are cheaper in cost but let’s first have a look at the entire policy itself, whether it provides good returns for your investment or not! Riders can be considered much later!

We will do the analysis of the returns of this SBI Shubh Nivesh Plan in both worst and best-case scenario of the assumed return rate calculated at 4% and 8% respectively in the next section…

SBI Shubh Nivesh Plan: Analysis and Review

As we have discussed in the illustration that Mr X is paying his Premium of Rs. 89,160 for 25 years (equal to the policy term)

In this analysis let’s consider that he is getting the SBI Shubh Nivesh Plan Maturity benefit in the best-case scenario, where the assumed (gross) rate of return is calculated at 8%.

These returns are NOT guaranteed but this is the maximum value you may get from this plan!

Let us find out the average returns considering all your premium payments for 25 years and the Maturity Amount of SBI Shubh Nivesh Plan, as discussed in the illustration (previous section)

|

At 4% p.a. |

At 8% p.a. |

||||

|

Age |

Year |

Annualised premium / Maturity benefit |

Death benefit |

Annualised premium / Maturity benefit |

Death benefit |

|

35 |

1 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

36 |

2 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

37 |

3 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

38 |

4 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

39 |

5 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

40 |

6 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

41 |

7 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

42 |

8 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

43 |

9 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

44 |

10 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

45 |

11 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

46 |

12 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

47 |

13 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

48 |

14 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

49 |

15 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

50 |

16 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

51 |

17 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

52 |

18 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

53 |

19 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

54 |

20 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

55 |

21 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

56 |

22 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

57 |

23 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

58 |

24 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

59 |

25 |

-89,160 |

20,00,000 |

-89,160 |

20,00,000 |

|

60 |

26 |

27,47,500 |

20,00,000 |

45,30,000 |

20,00,000 |

|

61 |

27 |

0 |

20,00,000 |

0 |

20,00,000 |

|

62 |

28 |

0 |

20,00,000 |

0 |

20,00,000 |

|

63 |

29 |

0 |

20,00,000 |

0 |

20,00,000 |

|

64 |

30 |

0 |

20,00,000 |

0 |

20,00,000 |

|

65 |

31 |

0 |

20,00,000 |

0 |

20,00,000 |

|

66 |

32 |

0 |

20,00,000 |

0 |

20,00,000 |

|

67 |

33 |

0 |

20,00,000 |

0 |

20,00,000 |

|

68 |

34 |

0 |

20,00,000 |

0 |

20,00,000 |

|

69 |

35 |

0 |

20,00,000 |

0 |

20,00,000 |

|

70 |

36 |

0 |

20,00,000 |

0 |

20,00,000 |

|

71 |

37 |

0 |

20,00,000 |

0 |

20,00,000 |

|

72 |

38 |

0 |

20,00,000 |

0 |

20,00,000 |

|

73 |

39 |

0 |

20,00,000 |

0 |

20,00,000 |

|

74 |

40 |

0 |

20,00,000 |

0 |

20,00,000 |

|

75 |

41 |

0 |

20,00,000 |

0 |

20,00,000 |

|

76 |

42 |

0 |

20,00,000 |

0 |

20,00,000 |

|

77 |

43 |

0 |

20,00,000 |

0 |

20,00,000 |

|

78 |

44 |

0 |

20,00,000 |

0 |

20,00,000 |

|

79 |

45 |

0 |

20,00,000 |

0 |

20,00,000 |

|

80 |

0 |

20,00,000 |

0 |

20,00,000 |

|

|

20,00,000 |

20,00,000 |

||||

|

IRR |

3.67% |

5.92% |

|||

In the above illustration, the IRR is calculated at 3.67% for the 4% Scenario and 5.92% for the 8% scenario.

SBI Shubh Nivesh Plan Maturity Amount Calculator

Therefore, if Mr X pays the annual premiums of Rs. 89,160 for 25 years and receives the SBI Shubh Nivesh Plan Maturity Amount of Rs. 45.30 Lakhs, in the best-case scenario.

And if we assume a life expectancy of 80 years, then he receives a death benefit of ₹ 20 Lakhs (sum assured payable under whole life option)

The average returns will be capped at 5.92% only!

The SBI Life Shubh Nivesh Maturity Amount shown in policy illustrations is influenced by bonus assumptions and should not be considered a guaranteed return.

Key insights from the above analysis:

- Even after considering the best-case scenario, Mr.X will end up getting the returns of 5.92% and we have not included the taxes that Mr X has to pay along with each of his premiums.

- Taxes will be added to the premiums at the rate of 4.5% in the first year and 2.25% from 2nd year and onwards.

- The assured sum is inadequate for the premiums that Mr X will pay throughout the policy term of 25 years.

- The maturity benefit at pre-expenses assumed (gross) return rate of 4% is Rs. 27,47,500, as we saw in the illustrative example in the previous section.

- The returns are in the range of 3.67%. Therefore, in the average case scenario, you may expect a 3.67% return from this plan. It means the returns from this plan will vary between 3.5% to 6%, with NO guarantees!

SBI Shubh Nivesh Plan (2020 update): Past Performance Review with Illustration

Since the inception of the SBI Shubh Nivesh Plan, it has generated the returns in their bonuses as shown below:

A review of historical SBI Life Bonus Rates indicates that traditional participating plans may deliver lower returns compared to market-linked investment alternatives.

Please note: The returns in Bonuses are percentages of the basic sum assured.

Reversionary Bonuses

Terminal Bonuses

Insight:

As you can notice that in SBI Shubh Nivesh Plan the calculated returns on bonuses have been below average in the past years.

You can easily get more returns than this even from your Saving Bank Account!!

So, basically, it doesn’t make any financial sense to invest or stay invested in this plan.

Now let’s have a look at other investment options.

Let’s see how other options could possibly benefit you with the investment of the same amount of money and duration!

SBI Shubh Nivesh Plan Vs. Other Alternative Investments – Review

There is no point investing your money in SBI Shubh Nivesh Plan.

However, if your primary intention is to grow your money, then we recommend you invest your money in PPF or Mutual Funds to get a better value for your money.

Now, let’s compare the returns of SBI Shubh Nivesh Plan Vs. Mutual Funds and PPF.

For investors seeking long-term wealth creation, alternatives such as PPF, ELSS, or diversified equity mutual funds may provide a more compelling risk-reward profile than the SBI Shubh Nivesh Endowment Plan.

SBI Shubh Nivesh Plan Vs. PPF – Review

Let us say if you invest Rs. 89,160 per annum in PPF for 25 years, which provides you with guaranteed returns of 7.1%.

Therefore, after 25 years the returns from the PPF will be Rs. 61,27,084/-.

PPF Returns after 25 years: ₹ 61.27 Lakhs

Don’t you think, these guaranteed returns are much better than the best scenario’s non-guaranteed returns from SBI Shubh Nivesh Plan, where the assured sum is merely Rs.20 Lacs!!

SBI Shubh Nivesh Plan Vs. Mutual Funds – Review

In the case of Mutual funds, let’s say you invest Rs. 7,500 per month (or Rs. 90,000 annually) through SIP payment in a good equity Mutual Fund, that will generate 12% average returns.

You can use this Mutual Fund Online Calculator to find the Mutual Fund Returns.

After 25 years’ duration, the returns from Mutual Funds will be over Rs.1.27 Crores!

Unlike traditional SBI Endowment Plans, mutual funds provide greater transparency, flexibility, and the potential for inflation-beating returns over long periods.

Mutual Fund Returns after 25 years: ₹ 1,27,66,549

Have you noticed it? You have the potential to grow your amount of Rs. 89,160 (approx. 90,000) per annum up to Rs.1.27 Crores and more if only you choose to manage your money wisely!

In SBI Shubh Nivesh Plan the only guaranteed benefit is the Sum Assured, which is Rs. 20 Lacs only!

Returns from SBI Shubh Nivesh Plan Vs. Mutual Funds – Review conclusion

In the above illustration the Guaranteed Returns in 20 years for PPF, Assumed Returns of Equity Mutual Fund and SBI subh Nivesh plan are calculated.

The calculated Returns of Mutual Funds seem to be much higher than the other two.

You can read this Comprehensive Guide to Mutual Funds, to get a good understanding of choosing them.

Now, YOU tell us, will you still go for SBI Shubh Nivesh Plan?

Let’s have a look at the major limitations of this plan in the next section.

SBI Shubh Nivesh Plan vs SBI Life Smart Privilege Plan

‘Smart Privilege Plan’ is a unit-linked investment insurance plan which has 11 different fund options to choose from whereas ‘Shubh Nivesh Plan’ is a endowment policy which promises to provide lifelong coverage.

Read the complete review here. How Good or Bad is SBI Life Smart Privilege Plan?– Review 2024

SBI Shubh Nivesh Plan vs other Investment Plans – Review Conclusion

After a thorough analysis of all other alternative investment options for SBI Shubh Nivesh Plan, Term Insurance + ELSS or PPF seem to be far better options with greater returns.

Prospective buyers often look for SBI Shubh Nivesh Policy Details and SBI Life Shubh Nivesh Policy Benefits to understand whether the plan can meet both insurance and investment needs effectively.

Limitations of SBI Shubh Nivesh Plan: Analysis

Below are the major limitations of the SBI Shubh Nivesh Plan

- Lower Returns: As you have seen in the above analysis, this plan is giving you the returns of 6% in the best-case scenario and these are the returns after excluding the GST tax and other charges in this policy. And, returns in the average case scenario are just 2%! Such returns in a 20-year long-duration can’t even beat the rate of inflation!! In other words, you are losing money in this policy.

- Lack of Flexibility: There is a lock-in period of 5 years in this plan; if you choose to discontinue your policy within this duration, then you need to pay a heavy penalty. Whereas, if you invest in Mutual Fund, you will have the flexibility to cancel and move to the other fund anytime, in case your fund is not performing well.

- Lack of Transparency: Charges within this policy are not transparent and also the process by which returns are calculated in an online calculator is NOT transparent.

- Regulatory Authority: Endowment Plans are basically regulated by IRDA. And, IRDA’s regulations are predominantly focused on the Insurance aspect rather than the investment aspect. The investments, such as Mutual Funds investments are regulated by SEBI. So, when you invest your money, look for the right regulatory authority. You should not allow your investments to be handled by an authority that basically regulates the Insurance schemes.

- Premium Paying Term is equal to the Policy Term! If you are choosing your policy for 20 years, you will have to pay your premiums for 20 years. There is no option to reduce your premium paying term.

- Whole-life option: In personal finance planning, securing life insurance coverage up to your working years or until major financial goals are achieved is generally sufficient. Opting for whole-life coverage can lead to significantly higher premiums without necessarily providing proportional value.

SBI Shubh Nivesh Plan: FAQs

If you are still confused about whether this policy is good or bad, then read our answer below.

Should you buy SBI Shubh Nivesh Plan? Is it good or bad?

You should NOT put your money into SBI Shubh Nivesh Plan and it is a BAD policy. If you invest in this policy you may get the non-guaranteed returns in the range of 3.5% to 6%!! which cannot even beat the rate of inflation!!

What are the other investment options to consider as an alternative to the SBI Shubh Nivesh plan?

As you have noticed in the above analysis, with the same investment, you are getting a guaranteed amount of Rs. 61.27 Lakhs from PPF and over Rs. 1.27 Crore from Mutual Funds.

So, we recommend you go for Mutual Funds. However, if you are risk-averse then you can pick PPF investment.

Along with your investment, we suggest you take up a separate Term Insurance Policy. You can read this cheat sheet to select the best term insurance plan for you.

Also, have a look at our reviews on HDFC Life Click 2 Protect 3D Plus and ICICI Pru iProtect Smart Policy. These articles will help you to choose a better Term Insurance Policy for you!

Those looking for liquidity and higher growth potential may find that a combination of Term Insurance and Mutual Fund SIPs offers greater financial efficiency than the SBI Shubh Nivesh Plan.

Before surrendering the policy, it is advisable to calculate the SBI Life Shubh Nivesh Surrender Value and compare it with the future benefits expected from continuing the plan.

How to cancel the SBI Shubh Nivesh Plan?

There is a Free-Look in period of 15 Days, if you do not agree with the terms and conditions, you can cancel the policy and the premium will be refunded to you.

However, if you want to discontinue the policy beyond the free-look period, there will be discontinuance charges, you can read this SBI Shubh Nivesh product brochure for more details.

Conclusion: SBI Shubh Nivesh Plan Good or Bad?

You should NOT waste your money on this policy.

The SBI Life Shubh Nivesh Policy may be suitable for conservative investors seeking traditional insurance-linked savings, but it may not be the most efficient vehicle for long-term wealth creation.

The returns from this policy are not enough even to beat the rate of inflation, let alone get investment returns!!

Please beware of insurance agents who will try to fool you for their agent commission!

As we have already discussed in the analysis, if you want to grow your money, then consider investing in Mutual funds as the best-preferred option.

And, if you avoid all the investment-related risks, then consider investing in PPF, which provides guaranteed returns of around 7.1%!

For better Life coverage, consider taking up a standalone Term Insurance Policy. You can read this Cheat Sheet to find a better Term Insurance Plan.

Do you think surfing through social media platforms like Quora, Facebook, Twitter, etc. will clear your doubts on financial planning?

Please consult a professional financial planner for advice on comprehensive financial planning.

If you have any more queries on this policy, feel free to drop them in the comment below.

To get the suggestion about the right investment and insurance policy customized for your needs, you can book the FREE Complimentary Consultation Call with us by clicking the link below:

Sir, I have taken this policy for 11years and I already paid 6 installment, is there any way to come out of this?

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the time, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Sir, I know it’s too late that just because I have taken this policy for 15year and I already paid 6 installment, is there any way to come out of this or if I continue for the next 10 year shall I get any benefit form this ?

For me, even if I get 5%return or after 15year if I convert to pension, is it ok if I get a small return rather than losing my invested money?

Please suggest what to do now.

Awaiting for your valuable reply.

“Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the times, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here!

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/“

Nice review

Thanks

Thanks for this Article. By the policy doc link, I am unable to calculate how much money will I get if I choose surrender option.

I have paid premium of 23k for 6 years. I dont want to continue and havent paid its last premium, I now decide to surrender and get back my money. Can you help me know how much can I get back?

“Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the times, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here!

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/“

Wish I could have read this before. I bought this policy only to find fake promises from agent. Fortunately I found this article before the end of my review period. So I am returning back my SBI Shubha nivesh policy right away. Thanks for such good insight .

Nice to know Rohith.

I am happy that our article has helped you take better decision.

Thanks for sharing.

I took sbi shubh nivesh policy for endowment will life .now I m thirty years old.i have to till 60 years.sum assured is 800000 and monthly emi of 2362.please suggest me what should I do.please suggest about surrender or paid option also

“It is advisable to not take this insurance plan.

But if you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the times, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here!

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/“

THE Worst policy I have ever seen in my life. I took policy 12 years ago with Rs.3000/- per month with sum assured Rs.3,80,000/-. After 12 years, I would get only 5,30,000/-. Very very bad policy, do not believe SBI

We understand your disappointment—many traditional endowment plans like SBI Shubh Nivesh Plan tend to deliver lower returns over long periods.

In your case, the maturity value reflects an annual return of around 4–5%, which often struggles to beat inflation.

Going forward, it’s important to separate insurance and investment—a term plan for protection and better-performing instruments for wealth creation. Let’s focus on improving outcomes from here.

Hello Team,

A

I have opted for “Sbi Life – Shubh Nivesh-Whole Life Plan – Series 3” with 30 lacs sum assured starting from Jan 2019 and 8865/month payment for 30 years.

It also includes “Accidental Death Benefit Ride and ATPD Rider – RP (Shubh Nivesh)”. I have few questions if you can help answering;

1. Is it a good investement?

2. If I want to stop this policy, what options do I have face minimum loss? Please explain this.

B

I have opted for “Sbi Life – Shubh Nivesh-Whole Life Plan – Series 2” with 3 lacs sum assured starting from MAR, 2016 and 17142 yearly payment for 20 years.

It also includes “Accidental Death Benefit Ride and ATPD Rider – RP (Shubh Nivesh)”. I have few questions if you can help answering;

1. Is it a good investement?

2. If I want to stop this policy, what options do I have face minimum loss? Please explain this.

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the times, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

What if I stopped paying amount after my 3rd year of payment..

If you have discontinued the policy beyond the free-look period, there will be discontinuance charges, you can read this SBI Shubh Nivesh product brochure for more details.