Opportunities seldom knock on our doors.

But that is not true to everyone.

Many of us have to work hard for it; you may be someone creating your opportunities through sheer hard work. One of those is earning a job overseas that you deserve.

It is not only the global exposure that lies ahead of you—but alsothe financial betterment that will transform your life.

It is not only the global exposure that lies ahead of you—but alsothe financial betterment that will transform your life.Is there such an opportunity within your hands reach?

Or are you counting days to board your flight?

It will be a world of change in your life. At this point, handling your NRI finances is a top priority.Because if you don’t, you could end up losing your hard-earned money and miss great investment opportunities.

Creating a Checklist or ‘to-do list’ helps to ensure consistency and completeness in carrying out your financial tasks. Becoming an NRI is a major transition that needs a checklist.

Here is a personal finance checklist to be taken care of before departing from India.

Table of Contents:

1. Update NRI Status in All KYC

2. Your First NRO Account

3. Open Your NRE Account

4. NRI Demat Account

5. Power of Attorney for NRIs

6. NRI Financial Plan

7. NRI Financial Services

8. Conclusion

Update NRI Status in All KYC

The first significant step is to update your change of status as NRI in relevant KYC.

Inform the mutual fund AMCs, Banks, and Insurance Companies by submitting the updated Know Your Customer (KYC) forms stating your change of status as a non-resident Indian. Your professional financial planners, Investment advisor, and Bank branch/relationship manager could help you best with the different formalities.

Now that you are all set to assume your NRI status, it is time to level up to other significant steps.

Your First NRO Account

Be it a resident or NRI Financial Plan: a savings bank account is a cornerstone of your personal finance.

But when you become an NRI, you cannot use your savings bank account as you would as a resident. The first thing is to convert your savings bank account to an NRO account.

An NRO account (Non-Residential Ordinary account) is a bank account for NRIs to avail the services same as a savings bank account. It gives the domestic rate of interest as set by the bank.

You can use your NRO account for depositing your domestic earnings like rent, interest and dividends, and remittances from abroad into this account. You can also issue cheques for EMI payments and investments from your NRO account.

How to convert Savings Bank Account to an NRO Account?

Here’s a checklist to follow to convert your regular savings account into an NRO account:

-

- Get the NRO account opening/conversion form from the bank

👉 Or you can download it online from the bank’s website.

-

- Attach photocopies of required documents

👉 Proof of Identity

👉 Proof of Overseas Address

👉 Banks may also require proofs: passport or work permit photocopy, etc.

-

- Submit the form with the document copies to the bank:

👉 Through courier to the bank in India

👉 Or at the branch in your resident country

Note: If you are submitting your conversion form to the bank branch in India through courier, you have to get them attested by the Indian embassy in your resident country.

On receiving the conversion form with the valid documents, the bank will convert your savings bank account into an NRO account post verification.

If your savings bank account is a zero balance account, after conversion into an NRO account, you may have to maintain a minimum balance as prescribed by the bank.

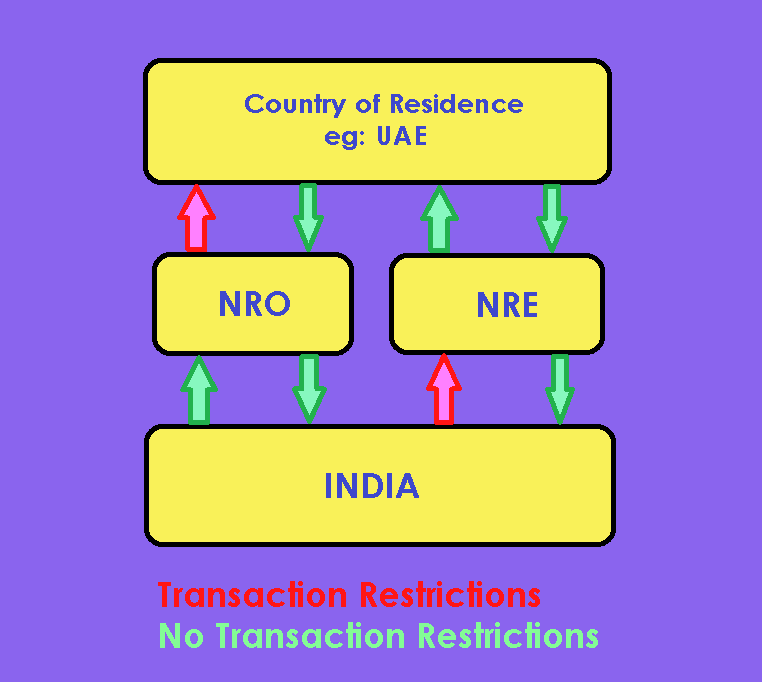

NRI Money Transfer to and from India:

There are no restrictions to transfer your current income earned in India to your NRO account.

But with an NRO account, there are restrictions for transferring money to the country of residence as an NRI. That is, the money in your NRO account is not freely repatriable.

The remittance of sales proceeds of properties and investments in India can be only to the extent of 1 million $’s a year.

A certificate from a chartered accountant, declaring that all taxes have been paid has to be furnished. It is important to note that an NRO account invites a tax of about 30% (plus cess and surcharge) as TDS on the interest earned.

One important thing is that it is best not to send your overseas earnings as an NRI, money to India using your NRO account. To do so, use an NRE account.

Let’s see, what is an NRE account? And why should you create one?

Open Your NRE Account:

A Non-Resident External (NRE) Account is an account to allow an NRI to deposit their foreign earnings.

An NRE (Non-Resident External) account can be opened with the currency of the country of your residence. Unlike an NRO account, there is no restriction to remittance in your NRE account.

You can make local payments in rupees, invest money and receive proceeds from the sale of investments and property.

As an NRI, you can deposit your overseas earnings in your NRE account. Besides, you may also deposit your investment earnings in India for investments made through your NRE account. However, this account offers no facility to receive incomes in the shape of rent, interest, dividends, or any other sources in India.

The principal and the interest earnings from your NRE account will not be taxable. Although, you would only get a low rate of interest than with an NRO account.

How to convert a savings bank account to NRE Account?

No, you cannot convert your savings bank account to NRE account. You have to create a new designated NRE account with the bank.

The NRE account opening procedure will pretty much be the same as with an NRO account.

Why Should You Open an NRE Account?

An NRE account is ideal when you want to invest or buy properties in India with your overseas earnings.

Since the funds in your NRE account is fully repatriable, I recommend against spending them in India.It is also not beneficial to keep a large sum in your NRE account since it earns only a little interest.

It is much easier to open both NRO and NRE accounts in India, as it requires 2passport size photographs with a copy of your passport and visa, other relevant document copies. In case you are already abroad, it is mandatory to get an attestation from the Indian Embassy or Notary before sending it to the bank branch.

NRI Demat Account

To start with, you must close your domestic Demat account.

RBI has prescribed a restriction with domestic Demat accounts held by NRIs. It says that: you can invest only up to 5% of the paid-up capital of an Indian company.Hence, to avoid this such restrictions, it is best to open an NRI Demat Account.

You have the option of 2 types of separate Demat accounts. You can open a non-resident ordinary (NRO) anda Non-Resident External (NRE) demat account under the Portfolio Investment Scheme (PIS). NRO & NRE Demat accounts are for non-repatriable and repatriable shares, respectively.

If you already have a domestic Demat account, you can transfer your existing shareholdings to this account.

The account opening procedure is the same if you are an NRI and want to open a Demat account for the first time.

How to Open A NRI Demat Account?

As stated above, you can open an NRI (NRO & NRE) Demat Account by opening a PIS account.

To open a PIS Account, visit the bank with which you hold the NRO & NRE account. Submit the following documents to the bank to open your PIS Account:

- Duly filled PIS form

- Address Proof (India & Overseas)

- Recent Passport Size Photograph

- Photocopy of Passport & Visa

- Photocopy of PAN Card

- FEMA Declaration

- Cancelled Check Leaf of NRO/NRE Account

Your Demat service provider will assist you in the submission of copies of your passport and visa.

You can read more about NRI Demat Account here: What Every NRI Needs to Know about PIS?

You can close the PIS Demat account once you return to India and become a resident Indian.

Power Of Attorney for NRIs

As an NRI working overseas, you must give a power of attorney to someone you trust.

The person you entrust must be a resident in India.

It essential to manage the financial transactions with bank accounts, buying & selling real estate, renting out property, signing tax forms, etc.when you become an NRI.

It also helps a lot in the protection of NRI property.

Property fraud is not a new thing in India. At this very moment, there are thousands of property fraud cases in the Indian courts. A good number of them will be with an NRI property.

By having a person with power of attorney in India, you are virtually present in India to protect your property. However, the benefits of granting Power of Attorney is not limited only to property protection alone.

Technically you can carry out almost every other legal deed even if you’re not physically present in India. Hence bestowing the Power of Attorney to someone you trust is essential.

A power of attorney could be general, where the authority entrusted holds good for banking and real estate transactions. Or it could be specific, where the POA holder can authorize only certain transactions.

I highly recommend you create only a Specific Power of Attorney where the holder has limited powers. Since two different people can hold the Power of Attorney for the same person, a specific Power of Attorney is more practical and relatively secure.

How to create & Grant Power of Attorney?

- Write two identical copies of the POA document in a white paper

- Detail the terms and conditions in the POA document clearly

- Have your original passport

- Overseas Address Proof

- 2 Passport Size Photo

- 2 Witnesses

- Visit the Indian Embassy to get the POA attested

- You (Grantor) must sign all the pages in the document in the presence of the Indian consul.

- Courier the POA document to the POA holder in India

Typically the POA need not be registered. However, in case of a sale of NRI property register your Power of Attorney at the sub-registrar’s office.

Note: The POA holder must register the POA within 90 days of its receipt.

Also, read: “How to Create Power of Attorney as an NRI?” for a detailed explanation about NRI Power of Attorney. It also contains a free Downloadable Power of Attorney Template.

NRI Financial Planning

One of the best things you can do before becoming an NRI is to have an NRI Financial Plan in place.

One common factor that prevents an NRI from making the right investment decisions is the complications in their financial plan. After a couple of years or so: when an NRI discovers the comprehensive NRI financial plan, their portfolio is already a mess. Their investments scattered around everywhere, limiting them from what they can do with their money.

It ranges from lack of liquidity to unnecessary taxation to missing the right investment opportunities and so on.

If you are an NRI or about to become one, avoid such investment complications at all costs. You may either create an NRI financial plan by yourself or get professional NRI financial services to get everything in place.

When it comes to an NRI, the approach to investments or the financial plan is identical to a resident’s financial plan. So what does an NRI Financial Plan takes care of?

Why is NRI Financial Plan indispensable for an NRI?

A few core things that makes your NRI Financial Plan indispensable are:

- NRI Investment in India

- NRI Tax Planning

- NRI Wealth Management

- NRI Estate Planning

1. NRI Investment in India:

All your investments must be your financial goals based.

There is no second thought on that. But, how much of your investments are in India. It is because India, as a fast-growing economy, can deliver the best returns for your investments, whereas your overseas investments give you the necessary diversification in your portfolio.

Moreover, the way you invest in India as an NRI matters a lot. It is because if your investments in India are non-repatriable, it may complicate things in the future.

For example: Since you are an NRI, your future may have too many uncertainties than does a resident. You may choose to settle overseas. Or even if you return to India after retirement, your children may want to live overseas. The uncertainty in NRI financial requirements such as these demands special attention while investing.

2. NRI Tax Planning

Tax planning is not always a priority when you are about to become an NRI. However, every NRI should be proactive in tax planning for the sake of wealth you are about to create in the future.

For an NRI, it is even more important since they might face double taxation in India and their country of residence. And if you are returning to India for good, you may want to move all your overseas assets& Investments to India. In such a case, a lack of an NRI Tax Plan may result in taxation that is easily avoidable otherwise.

Read more about NRI Tax Planning here: Everything You Need to Know about NRI Taxability and NRI Exemption.

3. NRI Wealth Management & Estate Planning

Even though you won’t need either NRI Wealth Management or NRI Estate Planning in your early days as an NRI, you will need them later.

NRI Wealth Management helps you manage, preserve and optimize the wealth you have accumulated over the years. On the other hand, NRI Estate Planning enables the smooth transfer of assets to your heir.

An NRI Financial Plan will help you identify your needs in those areas and build your portfolio in alignment with those needs.

A proactive NRI Financial Plan prevents all such complications and financial hardships of NRIs rather than making mistakes and then regretting it later.

Regardless of these, you may still be wondering,

“Why should I hire a financial planner?”

After all, who would want to spend money to manage their money?

It is a good question. Your caution show how important your finances is to you. But it is all the more reason to have a Certified Financial Planner to create an NRI Financial Plan and manage it for you.

If you have such questions in your mind, here are the secrets: Revealed: Are Financial Planners Worth the Cost?

NRI Financial Services

Are you taking the secure route by choosing to hire a Professional Financial Planner?

Smart decision!

But before you choose a NRI Financial Planner, you must assess them carefully. You have to look for a Certified Financial Planner specialized in creating and managing financial plans for NRIs. So,

How can you choose the right NRI Financial Planner?

I’ll list down a few key points to note before hiring a financial planner for your NRI Financial Services:

-

- NRI Financial Services Online:

One of the restrictions NRIs have is with their physical presence in India.

Before becoming an NRI, you may hire a financial planner. But if they can’t do a financial plan review online or enable you to access your portfolio over a secured network, it becomes a challenge for you to keep up.

Look for a Certified Financial Planner who employs FinTech Software and can provide NRI financial services over a secure online network.

-

- Reviews from NRIs:

You may choose an NRI Financial Planner based on referral or suggestion from a fellow NRI you know in person.

However, at times, one person’s experience may not be enough to gain your trust. Also, your needs and priorities may not always align with another individual. Hence always look for multiple reviews and recommendations.

With the digital revolution, the world has become more transparent. Finding Google reviews and Testimonials for an NRI Financial Planner online is much easier today.

Read multiple reviews and then approach your NRI financial planner.

- Online Presence:

An NRI Financial Planner’s online presence may look like an insignificant thing to consider. But, an NRI Financial Planner’sactivity on their website, blog, or social media handles could be a measure of their response time.

Being an NRI, ease of communication should be your priority since you will be in a different time zone.

Regular blog posts, social media post and other activities are a sign of ease of communication with your NRI Financial Planner.

These are only a few factors to size up an NRI Financial Planner before hiring one. For extensive ways to identify and assess the right NRI Financial Planner, read: The Ultimate Guide for NRIs to choose a Certified Financial Planner.

Conclusion

Becoming an NRI and stepping up in your career is a once in a lifetime opportunity one cannot afford to miss. But even such opportunities may not bring a deserving growth if you don’t prepare well in advance.

If you cannot star-off with an NRI financial plan right away, start with the simple things discussed in this article. They can help you move forward in the right direction.

As an NRI and to be NRI, you may have few queries to clarify. If you have any specific questions: leave them in the comment section.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘Book Now’ button below.

Hello There. I found your blog using msn. This is an extremely well written article.

I’ll make sure to bookmark it and return to read more

of your useful info. Thanks for the post. I will definitely comeback.