“You have worked hard and smart to earn your money.

With Tata AIA Fortune Pro, let your money work smartly as you do.” Says the official brochure of Tata AIA Fortune Pro.

It is not only a statement; it is also an indirect promise from Tata AIA Life Insurance.

But, can Tata AIA Fortune Pro fulfil this promise of bringing you a fortune?

There is only one way to find out.

Read this detailed review of Tata AIA Fortune Pro with examples and in-depth illustrations.

Table of Contents:

1.) Features of Tata AIA Fortune Pro

2.) Benefits of Tata AIA Life Fortune Pro

3.) Tata AIA Fortune Pro Policy Benefits Review

4.) Taxation of Tata AIA Fortune Pro

5.) Charges under Tata AIA Life Fortune Pro

6.) Can You Do Partial Withdrawal in Tata AIA Fortune Pro?

7.) Tata AIA Fortune Pro VS Tata AIA Fortune Maxima – Review

8.) Tata AIA Fortune Pro VS Tata AIA Fortune Guarantee Plus – Review

9.) Tata AIA Life Insurance Fortune Pro vs Tata AIA Life Insurance Wealth Pro – Review

10.) Comparison of Tata AIA Fortune Pro Returns against PPF

11.) Comparison of Tata AIA Fortune Pro Returns against ELSS Mutual Fund

12.) Tata AIA Fortune Pro vs Alternatives: Comparison Evaluation

13.) Final Verdict on TATA AIA Fortune Pro

14.) How to surrender your Tata AIA Fortune Pro policy?

15.) Tata AIA Fortune Pro Customer Support and Claim Assistance Review

16.) Who Should Avoid Buying Tata AIA Fortune Pro?

To understand whether it is worth investing in this ULIP policy, let’s take a closer look.

Here is the Tata AIA Fortune Pro review, starting with the policy features.

Features of Tata AIA Fortune Pro:

Before diving deeper, it’s important to understand how the Tata AIA Fortune Pro features, such as flexible policy terms and fund options, influence your long-term ULIP investment performance and overall financial planning strategy.

The Tata AIA Fortune Pro has no minimum age eligibility to buy this policy.

However, it has maximum age eligibility and maximum age at maturity.

Also, it offers a range of policy terms, starting from 15 years to 40 years.

Hence, for people over 35 years of age, the policy term will be based on their age.

The table below shows the eligibility conditions and other features of Tata AIA Fortune Pro.

Please review the table carefully for a better understanding of the good and bad features of this plan.

You should note that you cannot increase or decrease the premium once you buy this policy.

Many investors exploring tata aia fortune pro plan details and tata aia life insurance fortune pro plan often overlook how premium lock-in and policy tenure impact long-term returns.

Many investors comparing tata aia fortune pro review and tata aia life insurance fortune pro review often fail to evaluate how long-term ULIP charges affect actual wealth creation over 15 to 20 years.

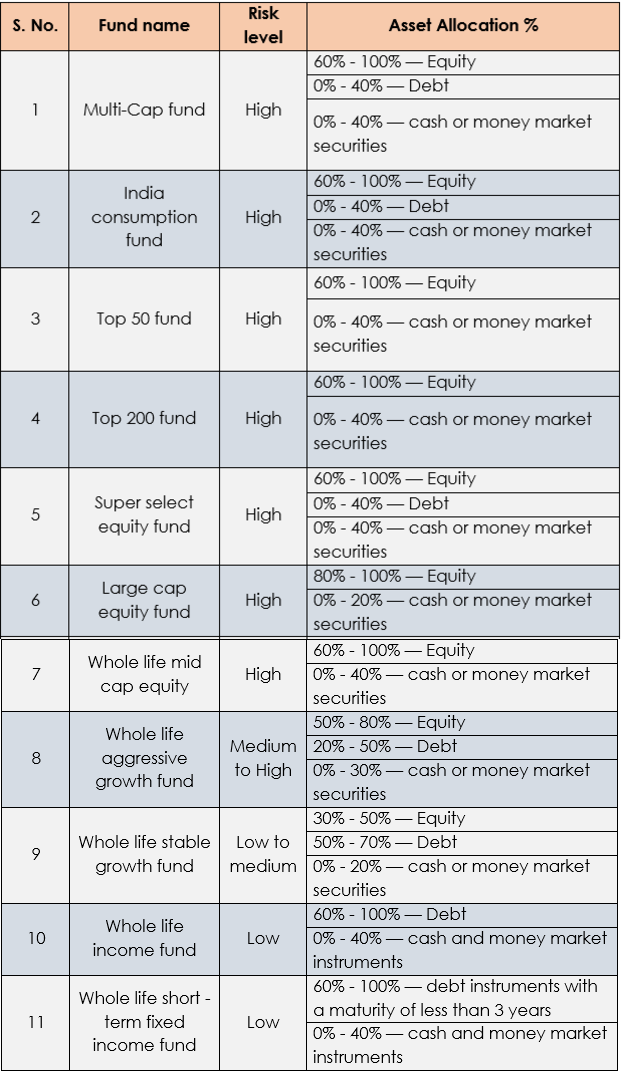

Funds in Tata AIA Fortune Pro Policy:

To make better fund choices, understanding the Tata AIA ULIP fund performance, risk levels, and long-term wealth-building potential becomes crucial for investors seeking balanced or aggressive growth.

The good thing about Tata AIA Fortune Pro is that it offers eleven different funds to invest in the premium.

You can choose to invest in any number of funds among these eleven funds.

Different funds have different risk profiles and fund performances based on their asset allocation.

You must weigh the good and bad aspects using the fund performance and risk profiles for a better perspective.

The table below shows the 11 different funds available under Tata AIA Fortune Pro.

The table also includes their asset allocation and risk profiles.

You can analyze the risk profiles of different funds, and decide whether it is good or bad for taking the risk, a calculated risk that you will not regret later!

A careful review of tata aia fortune pro fund performance, tata aia funds list, and tata aia ulip funds helps investors compare equity, debt, and balanced options under this tata aia unit linked insurance plan.

Before choosing between tata aia fortune pro ulip plan and tata aia wealth pro, investors should compare fund flexibility, policy charges, surrender conditions, and long-term return efficiency.

The different level of risk is calculated in the above table based on asset allocation.

Tata AIA Fortune Pro plan allows a systematic investment strategy, for Lumpsum investments, called Enhanced SMART.

It is abbreviated as Enhanced Systematic Money Allocation & Regular Transfer (Enhanced SMART).

It is nothing but a fancy name for the STP (Systematic Transfer Plan) in mutual funds.

It helps the investors choose single and annual premium payment options to spread their investments over a period.

In Enhanced SMART, the premium is first directed to any of the two debt funds.

The amount is then reviewed and transferred to any chosen equity fund systematically over a period.

Like every ULIP plan, a portion of the premium is invested in market funds and the returns generated will fluctuate based on the share price.

It is not available for the monthly and quarterly premium payment options.

The flexibility to switch between funds under Tata AIA Fortune Pro can be useful, but frequent switching without strategy may not improve long-term outcomes.

Benefits of Tata AIA Life Fortune Pro:

These Tata AIA Fortune Pro benefits often appeal to buyers seeking a combination of life cover and market-linked growth, but understanding their real-life value helps you avoid unrealistic expectations.

Unlike a pure Tata AIA term plan, this ULIP combines insurance with equity and debt exposure, which means returns depend heavily on fund selection and holding discipline.

Death benefit:

In the case of the policyholder’s untimely death, the nominee will receive the sum assured amount.

Once the sum assured amount is reviewed and paid, the policy will terminate.

Tata AIA Fortune Pro Policy Benefits Review:

Hopefully, on surviving the policy term, the policyholder will receive the fund value as of date.

Below is an illustration of the potential maturity benefit of the Tata AIA Fortune Pro policy.

We shall take the single premium option followed by the regular premium option.

Let’s calculate and review the fund performance in both the options.

Is the calculated maturity benefit good or bad?

Will the returns meet the expectations mentioned in their brochure?

Will it be a good or bad investment plan for your future? Let’s review and find out!

The Tata AIA Fortune Pro brochure presents assumed return scenarios, but actual maturity value depends entirely on long-term market performance and investor behaviour.

The Tata AIA Fortune Pro returns calculator may project higher maturity values, but actual investor returns depend heavily on market performance, fund selection, and policy continuation period.

Benefit Illustration of Single Premium Option:

The single premium ULIP return calculation reveals how charges, market volatility, and fund selection affect the final pay out, often reducing the effective CAGR investors expect from promotional brochures.

Suppose your age is 35 years.

You opt for the single, one-time premium option for your Tata AIA Life Fortune Pro Policy.

Now let’s calculate the expected returns of this investment plan.

Your one-time premium is ₹1,00,000. And the policy term is 20 years.

Your assured benefit, in this case, will be 1.25 times your single premium amount, i.e. ₹1,25,000.

On surviving the policy term, your maturity benefit will be calculated based depend on the fund performance.

And unlike an endowment policy, these returns are not guaranteed.

The official policy brochure of Tata AIA Life Insurance Pro gives an assumed return rate of 8% as the higher end and 4% as the lower end.

Assuming the funds, you choose is giving a return of 8% CAGR, your maturity value will be ₹3,35,903.

Even though the fund return is 8% CAGR, it is not the return rate in the hands of the investors.

It is because a significant portion of your premium will be deducted to provide life cover, and as a premium allocation charge.

Moreover, every year, other charges will eat into your fund returns.

This will result in a net annual return of 6.25% in 20 years.

The real impact on Tata AIA Fortune Pro returns comes from layered charges such as premium allocation, fund management, and mortality costs, which gradually reduce effective CAGR.

On the other hand, debt funds are more likely to give a 4% CAGR.

In such a case, your premium will grow to ₹1,50,865 at the end of 20 years.

And as always, the net annual return in the hands of the investor will be just 2.07%.

Investment return rates of 6.25% and 2.07% after 20 long years does not look attractive, does it?

Let’s see if the regular premium payment option is good or bad comparatively.

Before deciding whether Tata AIA Fortune Pro is a good or bad investment, investors must align the policy term with their actual financial goals, risk tolerance, and alternative investment options available in the market.

Benefit Illustration of Limited Premium Option:

Understanding the limited premium ULIP return calculation helps investors see how long-term charges, policy duration, and fund performance impact real returns—often much lower than brochure assumptions.

Let’s say you pay an annual premium of ₹1,00,000 for fifteen years. And the policy term is 20 years.

Your assured benefit will be 10 times the annual premium amount—₹10,00,000.

On surviving the policy term, you will get your fund value.

Again, this is non-guaranteed and only an assumption based on review.

Let’s assume your fund of choice gives 8% CAGR. In that case, your maturity value will be ₹32,56,363.

But in the hands of the investor, the 8% fund return will come down to a net return rate of 6.36%.

Even when the Tata AIA Fortune Pro returns illustration shows an 8% scenario, the effective IRR depends on charges, fund selection, and how long you stay invested without surrendering the policy.

Table showing the calculation of a net annual rate of return (IRR) in case your funds get a higher return of 8%:

Note: Minus sign before premium payment in the above table simply means it will be an outflow for you.

Considering the review of policy term and the premium paid, neither the ‘single pay’ nor the ‘limited pay’ options give a fair return.

The deduction of different charges, risk charges, and the GST on charges brings down the net investment return rate.

A detailed look at Tata AIA ULIP charges explains why the difference between fund CAGR and investor IRR widens over long holding periods.

A detailed Tata AIA Fortune Pro brochure review helps investors understand premium allocation charges, mortality charges, and policy administration deductions that reduce net returns.

Taxation of Tata AIA Fortune Pro:

Many people look for Tata AIA Fortune Pro taxation rules, so it’s crucial to understand how Section 80C, Section 10(10D), and the ₹2.5-lakh ULIP premium rule affect your post-tax maturity returns.

Tata AIA Life Insurance Fortune Pro premiums up to ₹1.5 lacks per annum are deductible under Section 80C of the Income Tax Act.

The maturity amount is exempt under Section 10(10D).

However, the maturity amount is tax-exempt only if the revised annual premium amount is less than ₹2.5 lakhs.

If the premium amount in any year exceeds ₹2.5 lakhs, you will be liable to pay the Long Term Capital Gains tax.

The LTCG tax for ULIPs is set at a rate of 20% before indexation or 10% after indexation.

Indexation means adjusting the amounts you paid for premiums for inflation to bring them in present value terms, for calculating the capital gains that you realized from your maturity benefit.

Before investing, reviewing the Tata AIA Fortune Pro taxation impact alongside alternative tax-saving investments helps in understanding true post-tax returns.

Charges under Tata AIA Life Fortune Pro:

Premium allocation charges will be deducted from all the premiums you pay in this policy.

The single-pay option will incur a premium allocation charge which will be calculated at 3% of the premium amount

For the other premium payment options, the premium allocation charge ranges from 6% to 2% of the premium amount as an annual premium charge.

Besides the premium allocation charge, you also have to pay a fund administration charge.

For the single-pay option, the fund administration charge is 0.90% of the premium amount per annum, for the entire policy term.

For the other premium payment options, the fund administration charge will be 0.75% of the annual premium amount throughout the policy term.

The fund administration charge is deducted by cancelling the units of your investments every month.

Besides, the mortality charge is also levied by cancelling your fund units.

The mortality charge is levied to provide life cover to the policyholder.

The mortality charge varies based on the Sum Assured and the age of the policyholder.

Waiver of premium rider (WOP) is available in this plan if the policyholder is rendered totally and permanently disabled before they attain 65 years of age.

Hidden charges in investment insurance policies are one of the major reasons for their poor returns.

Some charges reduce your investment capital, while others eat into your investment returns for years.

In the illustration section, we have seen that the fund return is not the same as the investment return.

Understanding Tata AIA mortality charges, fund administration fees, and premium allocation costs is critical before concluding whether this ULIP structure justifies the insurance wrapper.

In such a case, it is necessary to look for better alternatives.

Let’s compare and review the Tata AIA Fortune Pro against the alternative options.

It will help you make a better decision on whether to buy the Tata AIA Fortune Pro or not.

Investors reviewing tata aia fortune pro plan details should also understand the impact of lock-in period, discontinuance rules, and partial withdrawal conditions before investing.

A side-by-side review of Tata AIA Fortune Pro and Tata AIA Fortune Maxima helps investors compare flexibility, rider benefits, and overall cost efficiency.

Can You Do Partial Withdrawal in Tata AIA Fortune Pro?

Yes, partial withdrawals are allowed in Tata AIA Fortune Pro — but only after the mandatory 5-year lock-in period applicable to all ULIPs.

During the first five policy years, you cannot withdraw money freely.

If you discontinue the policy during this period, the fund value is moved to a discontinuance fund and paid only after completion of five years, subject to applicable charges.

After completing five policy years, partial withdrawals are permitted subject to certain conditions:

- A minimum fund balance must be maintained after withdrawal.

- The insurer may specify a minimum withdrawal amount.

- Withdrawals may reduce the death benefit, depending on the policy structure and sum assured multiple chosen.

- Frequent withdrawals can impact long-term compounding potential.

It is important to understand that while partial withdrawal provides liquidity flexibility, ULIPs like Tata AIA Fortune Pro are designed primarily for long-term wealth accumulation.

Using them like short-term savings products can dilute returns because of insurance charges and market volatility.

Before planning withdrawals, policyholders should evaluate:

- Whether emergency funds are available elsewhere.

- The impact on long-term goals.

- The tax implications, if any, under prevailing income tax rules.

Partial withdrawal can be a useful feature — but it works best when used strategically, not reactively.

Tata AIA Fortune Pro VS Tata AIA Fortune Maxima- Review

This is also a ULIP plan and both plans allow you to invest in 11 different funds.

Fortune Maxima has the option to customize your plan with 3 additional unit deduction riders.

To know more about the good and not-so-good aspects of TATA AIA Fortune Maxima

Check the below review with precise calculation of returns and a comprehensive analysis

TATA AIA Fortune Maxima: ULIP Review (2023)-Is it Good or Bad?

A comparison between Tata AIA Fortune Maxima fund performance and tata aia fortune pro fund performance helps investors evaluate whether additional rider flexibility justifies the overall ULIP cost structure.

Tata AIA Fortune Pro vs. Tata AIA Fortune Guarantee Plus – Review

Since many investors wonder whether a ULIP or guaranteed plan is better, this comparison highlights how Fortune Pro differs from Fortune Guarantee Plus in terms of return assurance and risk profile.

This plan is not a ULIP like ‘Tata AIA Fortune Pro’. ‘Tata AIA Fortune Guarantee Plus’ has a wide choice of payment and policy terms.

The income term is almost 45 years.

To know more about ‘Tata AIA Fortune Guarantee Plus’ with insights into good and bad aspects as well as a comprehensive calculation of returns.

Check the below link

TATA AIA Fortune Guarantee Plus: Review (2023) – Should you buy it?

Investors comparing Tata AIA Fortune Guarantee Plus review with tata aia fortune pro review should understand the difference between guaranteed return plans and market-linked ULIP products.

Comparing Tata AIA Fortune Pro with Tata AIA Fortune Guarantee Plus clarifies the difference between market-linked growth and guaranteed income structures.

Tata AIA Life Insurance Fortune Pro vs Tata AIA Life Insurance Wealth Pro – Review

Both the plans are ULIP and also don’t have a minimum age of eligibility.

While Fortune Pro allows you to invest in 11 diverse funds, Wealth Pro allows you to invest in as many as 14 diverse funds.

In both plans, the maturity amount is exempt under Section 10(10D). To know more,

Click the below link for a detailed review of the ‘Tata AIA Life Insurance Wealth Pro Plan’ to analyze the good and bad features.

Tata AIA Life Insurance Wealth Pro Plan Review: Good or Bad?

A comparison between Tata AIA Fortune Pro and Tata AIA Wealth Pro should focus on fund variety, cost structure, and long-term return efficiency rather than just the number of available funds.

Many investors evaluating Tata AIA Wealth Pro review alongside tata aia fortune pro often overlook the impact of recurring ULIP charges on long-term compounding efficiency.

Comparison of Tata AIA Fortune Pro Returns against PPF:

Public Provident Fund is an investment instrument from the Govt. of India.

It offers guaranteed returns, along with tax exemptions.

The Tata AIA Fortune Pro also offers a life cover, which the PPF does not.

When comparing Tata AIA Fortune Pro vs PPF, the core difference lies in guaranteed sovereign-backed returns versus market-linked performance with insurance charges.

Hence, you can take a term insurance plan for an assured value of ₹10,00,000 along with your PPF investment.

The term of this policy is calculated at 20 years.

This term insurance plan is not a savings plan.

It will give your nominees ₹10,00,000 in case of your death during the policy term. But, survival benefits are not calculated in this plan.

The term insurance policy premium will be much lesser than the Tata AIA Life Insurance Fortune Pro premium.

The combination of Tata AIA Term Plan with PPF creates clearer separation between insurance and investment compared to bundled ULIP structures.

Therefore, you can invest the remaining of your premium amount in PPF.

Read further to review whether PPF is good or bad compared to Fortune Pro.

Let’s see the return you can get by investing in this combo of term life insurance and PPF, for the same premium amount, sum assured, and investment term.

The prevailing interest rate of PPF is 7.1% p.a. And unlike the Tata AIA Fortune Pro, there are no hidden charges and deductions.

So you can get a higher return by buying a term insurance plan and investing in PPF, rather than in the Tata AIA Life Insurance Fortune Pro.

The table below shows the returns from PPF alongside the returns from Tata AIA Fortune Pro, for the same investment and period.

A Tata AIA Fortune Pro returns comparison clearly shows how cost layers reduce effective yield compared to fixed-rate PPF compounding.

The added advantage of the PPF investment is that there is no risk on this return, unlike the Tata AIA Life Insurance Fortune Pro.

Also, its investment, interest, and maturity amount are tax-free.

The term insurance will take care of your life insurance needs.

The PPF will take care of your saving needs. And the risk will be zero in the PPF option.

Comparison of Tata AIA Fortune Pro Returns against ELSS Mutual Fund:

Before exploring deeper, it’s also important to understand how long-term wealth creation, tax-efficient investing, and low-cost equity strategies play a major role in comparing ULIPs and ELSS funds.

When evaluating Tata AIA ULIP returns against ELSS mutual funds, cost efficiency and flexibility become decisive factors in long-term wealth creation.

Now suppose you have risk tolerance, you may choose to invest in an ELSS mutual fund scheme for even better returns.

To be fair, you don’t need any more risk tolerance than needed to invest in ULIP policy like the Tata AIA Fortune Pro.

Even after accounting for LTCG, ELSS mutual fund returns often exceed Tata AIA Fortune Pro net returns due to lower structural costs.

Even after accounting for LTCG taxation, ELSS investments may deliver stronger post-tax wealth creation than Tata AIA Fortune Pro Ulip Plan returns.

Since both are equity-linked investment instruments, they have the same investment risk levels.

Now instead of buying Tata AIA Life Insurance Fortune Pro, invest in an equity-linked savings scheme (ELSS).

And, of course, with a term life insurance to provide the same life cover for a far lesser premium.

Like the Tata AIA Fortune Pro, the ELSS mutual fund returns are not guaranteed.

Their returns are dependent on the performance of the stocks that they invest in.

A well-managed ELSS mutual fund can give you an annual return in the range of 12% – 15% or sometimes even higher.

The table below shows the potential return from an average ELSS mutual fund scheme in comparison with the Tata AIA Fortune Pro.

The investment amount is ₹1 Lakh, and the investment period is 15 years.

Long-term Capital Gains Tax (LTCG) on mutual fund returns is 10%.

After this tax, you can get a net return of 13.5% on your ELSS investment.

Even with the LTCG tax @ 10%, the returns from an average ELSS Mutual Fund scheme are more than twice that of the Tata AIA Fortune Pro.

One of the added advantages of investing in the ELSS Mutual Fund scheme is liquidity and flexibility.

If you are investing in Tata AIA Fortune Pro policy, you will have to face a 5-year lock-in period.

On the other hand, ELSS Mutual Funds have a lock-in period of only 3 years. It is the lowest for any investment option with Section 80C tax benefit.

Also, when you surrender your ULIP policy because of poor performance, it may incur some charges.

Thereby reducing your returns. But you can choose to stop investing in an ELSS fund and invest in a better-performing one at any time.

Such flexibility to the investors makes the ELSS scheme fund managers deliver good performance consistently.ULIPs lack this compulsion because of the lack of flexibility.

Hence ULIP funds consistently underperform even an average-performing ELSS Mutual Fund Scheme.

Tata AIA Fortune Pro Vs Alternatives: Comparison Evaluation

This is also where concepts like smart asset allocation, cost-efficient investment planning, and transparent financial products help investors judge the real long-term value of ULIPs versus traditional investment tools.

After a thorough and comprehensive analysis of all the other alternatives for ‘Tata AIA Fortune Pro’.

We have come to the conclusion that ELSS & PPF seem to be far better options.

We should not fall for the trap of dazzling new plans in the market. But, compare & review them with traditional plans.

When we see the good and bad aspects of new investment plans and traditional plans with a neutral mind set, the conclusion that we reach most of the time is that fund performance in ELSS & PPF seems to be better!

A disciplined combination of term insurance plus PPF or ELSS creates clearer financial boundaries than bundled ULIP products like Tata AIA Fortune Pro.

Final Verdict on TATA AIA Fortune Pro:

Ultimately, choosing between ULIP and market-linked alternatives depends on understanding real return on investment, charge structure transparency, and flexibility of your long-term financial roadmap.

The verdict is clear by now.

Like many ULIP policies in the bazaar, Tata AIA Life Insurance Fortune Pro is not a sound investment option.

A combination of term insurance policy with PPF investment is a better investment option.

It gives a slightly better return for absolutely no risk.

But, a combination of term insurance with ELSS mutual fund is a far better option.

Considering that the Tata AIA Fortune Pro is a ULIP, it has the same investment risks as an ELSS Mutual Fund.

By choosing to buy a term life insurance plan and investing in ELSS Mutual Fund, you get the benefit of better returns and investment flexibility.

But if you have already bought the Tata AIA Fortune Pro, you can always surrender it and go for the better alternatives.

Investors evaluating Tata AIA Life Insurance Fortune Pro review should also compare opportunity cost, liquidity restrictions, and long-term inflation-adjusted returns.

More about surrendering your Tata AIA Fortune Pro and its implications below.

Before concluding whether Tata AIA Fortune Pro is good or bad, investors must evaluate opportunity cost, liquidity needs, and long-term compounding efficiency.

How to surrender your Tata AIA Fortune Pro policy?

Before surrendering, it also helps to understand policy exit charges, lock-in rules, and fund value adjustments, which affect how much money you actually receive.

You can surrender your Tata AIA Life Insurance Policy back to the company.

And there are two options to do it, based on when you bought this policy.

Surrendering during the Free Look Period:

This phase is crucial for evaluating whether the policy aligns with your financial protection goals and wealth-building expectations before getting tied to long lock-ins.

The free look period is within 15 days of purchasing the policy.

If you are within the free lookout period, then you can immediately surrender the policy. No questions asked.

You can return your policy document with a request to surrender your policy.

Your premium amount will be returned to you minus any writing charges and the risk charge for the number of days covered.

For purchases through distance mode, such as online purchases, the free look period is 30 days.

If you are in the free look period, do not hesitate and surrender your policy if you are convinced to have better alternatives.

Otherwise, your huge premium amount will be locked-in for 5 years in a below-par investment product. And you will have no choice but wait for years

Surrendering after the Free Look Period:

Investors should also be aware of discontinued fund returns, low-yield holding patterns, and mandatory waiting periods, which can significantly affect final pay-outs.

You already know there is a 5-year lock-in period after the free look period.

But if you still proceed to surrender the policy, your investments will be moved to a Discontinued Policy Fund.

Discontinued policy fund earns returns in the range of 4%.

Of course, the net return will be even lesser—probably even lesser than a savings bank account interest rate.

At the end of five years, the fund value will be paid to you and the policy terminated.

If your lock-in period has also passed, then you can surrender the policy and the company will return the balance amount in your funds after deducting discontinued policy charges.

To surrender your policy, walk into any Tata AIA Life Insurance branch and submit your surrender request.

They may ask for proof of ID and address and the original policy document.

You may also request for policy surrender by emailing them to customercare@tataaia.com

The Tata AIA Life Insurance customer care process for policy surrender usually requires policy documents, ID proof, bank details, and a formal surrender request.

Understanding Tata AIA Fortune Pro surrender charges and discontinued policy fund returns helps avoid unpleasant surprises at exit.

Tata AIA Fortune Pro Customer Support and Claim Assistance Review

Apart from fund performance and returns, customer service quality also plays an important role in the overall policy experience.

Many policyholders evaluate factors like responsiveness, claim settlement support, policy servicing efficiency, and grievance handling before choosing a long-term ULIP plan.

Understanding the quality of Tata AIA customer care, policy assistance process, and claim support responsiveness can help investors avoid future servicing difficulties.

Whether it is updating nominee details, requesting fund switches, tracking policy status, or initiating surrender requests, efficient support becomes essential in long-duration investment-linked insurance products.

Investors should also review branch accessibility, online servicing features, and turnaround time for resolving complaints before purchasing any ULIP policy.

Step-by-Step Checklist Before Surrendering Tata AIA Fortune Pro

- Check lock-in period: ULIPs have a 5-year lock-in. Know how many years have passed.

- Gather policy documents: Original policy, latest fund statement, and unit statement.

- Calculate fund value vs premiums paid: Helps assess gains or losses.

- Request surrender/discontinued fund value: Ask customer care for exact net pay out and charges.

- Check surrender charges & penalties: Include premium allocation, fund admin, and mortality charges.

- Compare options: Surrender now vs move to discontinued policy fund — which gives better net return?

- Review projected returns if you continue: Single premium, limited pay, and regular pay options.

- Consider tax implications: Check Section 10(10D), LTCG, and limits for premiums > ₹2.5 lakh/year.

- Plan replacement life cover: Ensure term insurance is in place before surrendering ULIP.

- Explore alternatives: Partial withdrawal, fund switch, or top-up instead of full surrender.

- Check riders & benefits: Waiver of premium, disability cover, or other benefits may be lost.

- Prepare documents: Surrender form, policy document, photo ID, address proof, canceled cheque.

- Get written confirmation: Net payable amount and expected timeline for fund transfer.

- Plan reinvestment: Decide on PPF, ELSS, or other investments beforehand.

- Consult financial advisor (optional): Review pros and cons before making the final decision.

- Execute & follow up: Submit documents, keep acknowledgment, and track payment.

Who Should Avoid Buying Tata AIA Fortune Pro?

Individuals who prefer straightforward investments, low charges, or high transparency should steer clear of this policy.

It is not suitable for people who want liquidity since ULIPs impose strict lock-ins and penalties for early exit.

Anyone who prefers to track their investments regularly, switch funds freely, or improve long-term returns through compounding and low-cost instruments should avoid ULIPs entirely.

If you dislike mixing insurance with investment, this product will feel unnecessarily complicated and expensive.

A proper Tata AIA Fortune Pro review should assess not only fund performance, but also liquidity flexibility, surrender conditions, taxation, and post-charge investor IRR.

Conclusion:

Choosing the right financial product becomes easier when you focus on low-charge investment options, flexible wealth-building strategies, and independent insurance-investment planning

ULIP policies fall short as insurance products and as investments.

The Tata AIA Fortune Pro is no exception.

All they can bring is hidden charges and complications to your investment portfolio.

Hence, it is always wise to keep your insurances and investments separate.

But before you surrender your Tata AIA Fortune Pro, consult your financial advisor.

They can help you take the best course of action and avoid unprecedented financial complications.

More importantly, help you make the right investment decision.

Please don’t fall prey to amateur bits of advice on social media platforms like Twitter, Facebook, Quora, etc. It is always wise to take the help of a professional financial planner.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30-minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

This was in depth and so accurate so easy to understand that a person who has zero knowledge about investment can also make decisions and not fall prey for these Insurance plans that guarantees a guaranteed return.

Thankyou so much for this article you’ve saved my hard earned money .

I want to connect with you for investment planning kindly let me know how can we connect?

My contact number – 7042467789

Thank you so much for such a great information.

Can explain to me, how can buy the ELSS Mutual Funds.

Thank you for your kind words! We can certainly guide you on buying ELSS Mutual Funds. Please register for a free consultation through this link: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/. Our experts will provide personalized advice and help you make informed investment decisions.

Hi There

Your review and illustration was awesome. I couldn’t find a better analysis than yours. It was super helpful

Very vital informative,indepth and best learner’s for us as we’re confused by different ones about the best way of comprehensive investment.Eqully thankful to u kindself for suggestions for better to go for the elss plans.By table we are happy finding your comparison table between different segments of investment.

I’m glad to hear you find the information valuable! For comprehensive investment, ELSS plans can indeed be a great choice. They offer tax benefits along with potential for growth. If you have specific questions or need further details on ELSS or any other investment segments, feel free to ask. I’m here to help!

pl guide me to creating a Comprehensive Financial Plan for my financial goals

If you have any queries regarding Personal Finance,

book a compiled Consultation with one of our Financial Planners by using the following link:

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/