“Save one third, live on one-third, and give away one-third.” – Angelina Jolie

What if you had a job loss, a major sickness, an accident or a natural calamity? Imagine what you would do, when there is no one around? Or when none of them can help you financially? Difficult isn’t it? Here comes to rescue, your “Emergency Fund.”

Having an emergency fund which is properly planned and invested would allow you to invest better in other long term investments, without the fear of having no money during an emergency.

“Prevention is better than cure”.

Yes, you heard it right, you should prepare for your future, a step ahead, and so you will not suffer later.

An emergency fund is a readily available source to help you solve financial crises due to unexpected reasons. This fund helps improve financial security by creating highly liquid cash to meet any emergency and reduce the use of unsecured loans.

Why are Emergency funds so important and what mistakes investors do?

Many investors have their investments in illiquid products, say for eg: real estate, land, etc. and so when there is an urgent requirement they don’t have enough in cash.

There are many other temptations to spend these days. For every other product/service you hear of free, offers, discounts, cashback, win an exciting trip to XYZ, win exciting prices, win a free ticket, etc, all these make us spend.

Taking loans or swiping credit cards has also started becoming very common. And with all these happening around, there is no enough saving taking place.

Who thinks of an emergency and saves for an emergency?

Not many.

So, if you are in the above said situation and if you haven’t saved enough for an emergency, What if these kinds of emergencies happen to you?

It could be anything for E.g. a sudden job loss, a major accident, natural disaster, death, unexpected travels, house repairs, car repairs, medical expenses, etc. Any of these could happen and all of a sudden too.

Are you prepared? Have you set aside enough money, for an emergency? If yes, how fast can you access this money? Can your family access this money, if you are not around? If yes, How much and how fast can they access this money?

Also read, Why An Emergency Fund Is Important!

What if you said you have already enough money in the bank?

You might think that you have enough money in the bank and can be used in case of an emergency. That’s the current money you have, will you still be having the money when you meet with an emergency?

You “may not,” as you haven’t saved something as an “emergency fund”. People, who have enough funds in the bank, don’t have it when they need it the most. Maybe you would have used it for some other purpose. E.g. shopping, an expensive gift, etc.

Hence the money for emergencies should not be used for any other purpose; it can be used only for emergencies.

People worry about some situations, they don’t want to face but can happen, like a job loss, accident or other such unexpected situations. But imagine you have already saved enough and are ready for the worst. You may suffer and it can’t be fully eliminated, but the intensity will be reduced, at least financially.

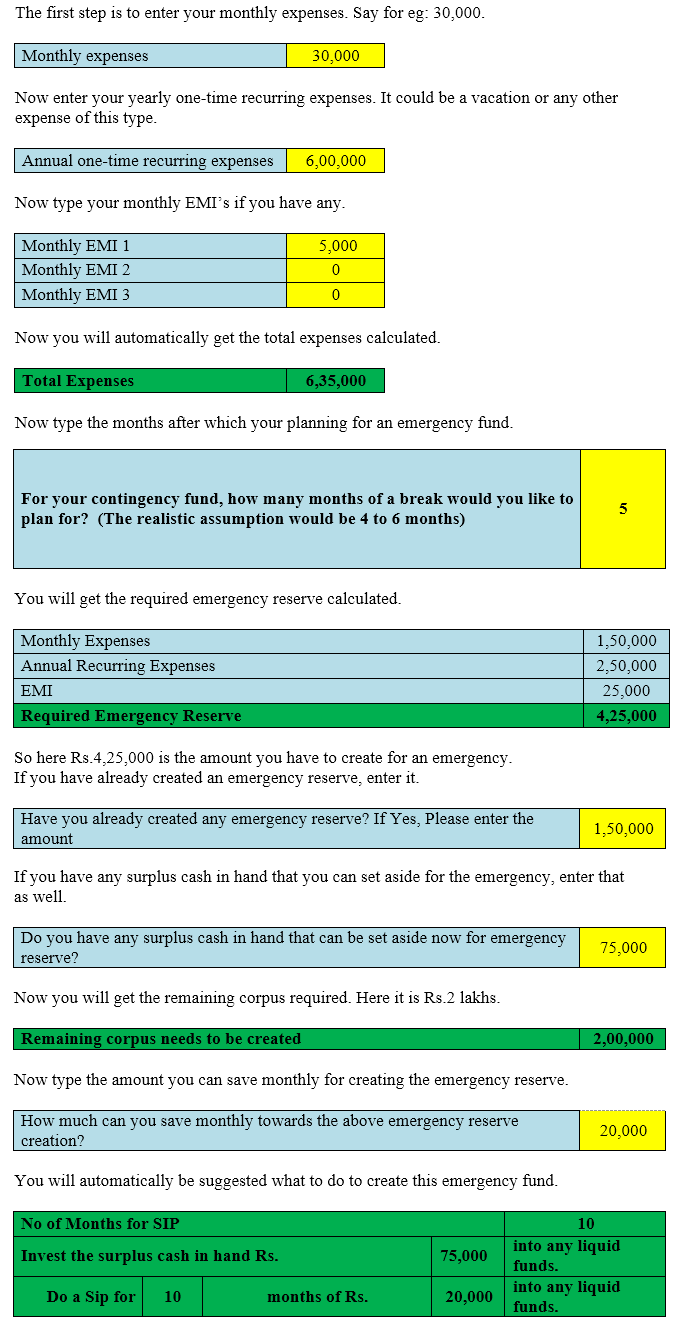

Click here to download a “Planner for Emergency Reserve Creation.”

Here is a SureFire Way to Start an Emergency Fund

1. List your monthly expenses

The first step is listing all your monthly expenses. Differentiate between expenses that are a must and which are not. Considering unnecessary expenses will help you cut down these and increase your savings. Include all kinds of expenses like rent, electricity bills, movies, dinner out, clothing, etc.

2. Decide your emergency fund

How much to set aside as an emergency fund?

Keeping aside 3 to 6 months’ worth real living expenses is a thumb rule. If you have a stable income (e.g. you have a govt job and there is job security) you may plan for the lower figure i.e. 3 months. If your credit limit is near and your income is less secure (job insecurity), you must plan to save for the higher figure i.e. 6 months.

E.g. you earn Rs. 1,00,000 a month and you spend Rs. 50,000 for meeting your expenses, then your emergency fund should be in the range of Rs. 1,50,000 to Rs. 3,00,000.

To calculate the exact amount, you need to calculate what 3 or 6 months worth of expenses is for you. Add up what you spend each month and multiply by 6 (if taken for 6 months) and 3 months (if taken for 3 months).

Download the calculator here! This emergency reserve calculator is very easy to use. Let’s see how it works.

This is the suggestion:

To create Rs. 2 lakhs, you can invest Rs. 20,000 in a SIP for 10 months.

3. Plan to save

You have to develop a plan to save for your emergency. Your plan should include specific and measurable targets. Like how you saw in the above example, you have to decide whether you have to save for 3 or 6 months.

✔ If you are the only breadwinner in your family :

You will have to save a bigger sum of emergency funds. Because if you lose your job, there will be no income at all. So you will need it as there is no one to support you.

✔ If you have an unstable job :

You must have a larger emergency fund as the chances of losing your job is higher and you should be prepared.

✔ If you or your family have serious health issues :

You should have a higher emergency fund as you may incur a lot of medical expenses.

Also, click here and download “income and expense tracker along with the Planner for Emergency Reserve Creation”.

Each and every penny counts. And so is your sudden bonuses, little cash prices, dividend from small investments and tax refunds.

It is always a smarter move to divert all these cash towards your emergency reserve corpus. This would in turn help you to achieve your emergency fund target in a much shorter span.

4. Make emergency fund accessible

It is better to put your funds in a liquid asset, as it is easily convertible into cash. If you invest in non-liquid assets like land, real estate, etc, it will be hard to liquidate them and take months to receive cash from sales. So saving for an emergency means easy availability of cash and it’s not about the returns.

So for emergency funds, it is best to invest in liquid assets as you will be able to withdraw it when you need it with no delay. You should also ensure you are not fined.

It may be a savings account that provides return and lets you withdraw at any time without penalty.

5. Follow the plan

If your goals are realistic, sticking to the plan is easy.

✔ One way is to set up a systematic transfer from your savings account. The emergency fund should be separate from your regular savings account so you are not tempted to spend it and also don’t think you have more cash than you do.

✔ Another way is to assign your future bonus or increments for the emergency.

✔ And one more way is to take a lump sum from any of your investments and set it aside for the emergency.

6. Auto debit

Want to have an absolute hands free process with your cash?

Yes, we all do. Because manually attending your cash grabs a lot of brain work every time you deal with your cash.

Having an auto debiting mode activated in your account could save you a lot of time by deducting the said cash from your income account and transfer it to your emergency reserve investments, automatically. Also, this would create a schedule for your disciplined investment.

7. Reviewing your emergency fund

It is always an advantage to be assured of how sufficient is your emergency fund holding, time to time.Life can change at any moment, after all it is all you’re planning. Whether it be welcoming a new member into your family or building your own sweet home, we always have to be prepared for what’s coming.

And to face these situations, its best suggested to review your emergency funds on a regular basis for at least a year. This would help you to be well aware of your own needs and thus providing you a better clarity.

Questions you must ask yourself before using the Emergency Fund

-

a) Is it an emergency?

b) Is it a need or a want?

c) Do you need it now?

So only when in an emergency, this money should be used.

Underestimated Benefits of Emergency Fund

Peace of Mind

There is psychological power in knowing you have funds to rely on, in case of unexpected expenses. This emergency fund can give you peace of mind by assuring you that you can manage an unexpected expense.

Financial stress can affect your health and life. By minimizing financial stress, you can improve other areas of your life. Experts say all should have an emergency fund, regardless of their financial situation, because it protects you against all the unexpected expenses that may damage your financial plans.

It helps maintain discipline in investing.

It will help you in the habit of saving regularly. As it becomes a routine, you will always save and have enough money for an emergency. You will look for reducing your daily expenses, so you will have more money to invest. This will stop you from being in debt and also pave the way for spending on things that are most important to you.

The protective layer of your financial life.

It helps protect your financial life, as you are ready for any emergency that could come your way. Your finances will not be affected due to crisis, as you have saved for all your emergency needs. You will be financially safe if there are future mishappenings or unexpected expenses.

Avoid costly loans

If you have emergency funds, in case of emergencies, like house repairs and other such expenses, you wouldn’t swipe your credit cards or go for loans, instead, you will rely on the emergency funds. Thus avoiding costly loans, which will take you months to repay.

Less panic

If you have emergency funds, you wouldn’t have to panic much. For example, you lose your job, you would be much better if you saved for an emergency because you have enough time to search for your next job. Till then you can make use of your emergency funds to pay off your groceries, rent, EMI’s, etc. Another example is, in case of a major accident to a family member, there may be a panic, but with emergency funds, you will have a source to pay off your medical bills and that would be a bit of a relief.

Discover Where to Invest Your Emergency Reserve

Some options to invest would be:

Savings bank account

This is liquid, as it is available in cash through an ATM. But it should not be kept in the same bank account, as you would do for the rest of the money. It would become difficult to track your money and also not to use it for some other purpose.

E.g. you go shopping, see a beautiful piece of clothing that costs around Rs. 25,000 and the money you have in savings is Rs.1,00,000. You would immediately buy it, thinking there is enough money; you would have forgotten that it’s a part of your emergency fund.

This is why you should be saving emergency funds in another account. So you wouldn’t mix up with your original savings account and use it.

A savings account will earn 4% to 6% of interest depending on the bank.

Bank Fixed Deposits

Money can be invested in bank fixed deposits as it can be taken anytime there is an emergency. You can deposit in bank fixed deposits but not in company fixed deposits, as they are not emergency-friendly. Company Fixed Deposits are not liquid and are not easily convertible into cash. Bank FDs have safety, flexibility, stable returns and liquidity.

Liquid Funds

You can invest in ultra-short-term debt funds and liquid funds. This is the most preferred investment as it is easily convertible into cash. It also acts as a great option to earn you higher returns compared to other investment options.

They are flexible enough to charge you less tax incidence. Hence, liquid fund is your go to option when it comes to setting up your emergency fund.

Liquid funds are safe mutual funds with better returns than bank savings account.

E.g. You have Rs. 1,00,000 as your emergency fund. You can keep 20,000 in cash at home, Rs. 20,000 in your savings bank account and invest the remaining Rs.60,000 in liquid funds.

Credit cards

This can be used in case of real emergencies. Use it only as a last option when all other options are not available. E.g. you are in an emergency, but banks are closed due to strike, election or holiday. In this case, you can use a credit card.

Conclusion

As you have seen the Importance of Emergency Fund, it is suggested you set aside some money for this purpose. If it is used for some other purpose, then in an emergency, you will not have funds, especially if it is a huge sum.

So on the safer side; it is better not to use it for any other purpose. When in need, you will have the funds to use. You will not suffer much as you have already planned.

You can save 3 to 6 months’ worth of real living expenses, according to your requirements. You can invest in a savings account, fixed deposit or liquid funds.

Also, it’s best advisable to be aware of your own financial vulnerability and save accordingly. No matter if your said target as emergency fund is achieved, if you feel you may still have to have some more, then plan appropriately and go for it.

What in case you are still not saving an emergency fund?

When emergencies happen, you will not be able to manage and fail badly. You will have no safety and no way to access cash. Not able to pay an emergency can cause personal and relationship stress as well. Ending up in debt can be the worst you can face.

Why take this risk? Are you ready to start saving for emergencies?

Once you have 3 to 6 months of living expenses set aside; you will have peace of mind. You will be happy you saved for an emergency.

Leave a Reply