ICICI Pru Lifetime Classic is a ULIP policy, which seems to provide a lot of different options in its investment aspect.

The company claims it to be a potential policy to grow your money faster as compared to the other existing ULIPs!

How true is this claim, we will find this out in our analysis of this product!!

Also, in this article, we will critically review the key features and benefits of this policy and will arrive at the conclusion of whether you should buy this policy or not!!

Table of Content

1.) ICICI Pru Lifetime Classic: Key Features

2.) Charges under ICICI Pru Lifetime Classic

3.) ICICI Pru Lifetime Classic: Death and Maturity Benefits

4.) ICICI Pru Lifetime Classic: Basic Eligibility

5.) ICICI Pru Lifetime Classic: Illustration

6.) ICICI Pru Lifetime Classic: Analysis and Review

7.) ICICI Pru Lifetime Classic: Disadvantages

8.) Common Queries on ICICI Pru Lifetime Classic

9.) ICICI Pru Lifetime Classic – Good or Bad?

1.) ICICI Pru Lifetime Classic: Key Features

ICICI Prudential Life Time Classic is a Unit-Linked Insurance Plan (ULIP) that combines life insurance coverage with market-linked investment opportunities through a wide range of fund options.

With this plan, you get the option of investing in 25 different funds ranging from a low risk-low return to high risk-high returns.

|

S. no |

Fund Name |

Asset Allocation |

Risk Profile |

||

|

Equity and Equity-related Securities |

Debt |

Money market and cash |

|||

|

1 |

Focus 50 Fund |

90-100% |

0-10% |

0-10% |

High |

|

2 |

India Growth |

80-100% |

0-20% |

0-20% |

High |

|

3 |

Opportunities Fund |

80-100% |

0-20% |

0-20% |

High |

|

4 |

Multi Cap Growth Fund |

80-100% |

0-20% |

0-20% |

High |

|

5 |

Blue-chip Fund |

80-100% |

0-20% |

0-20% |

High |

|

6 |

Maximiser V |

75-100% |

0-25% |

0-25% |

High |

|

7 |

Maximise India Fund |

80-100% |

0-20% |

0-20% |

High |

|

8 |

Value Enhancer Fund |

85-100% |

0-15% |

0-15% |

High |

|

9 |

Multi Cap Balanced Fund |

0-60% |

20-70% |

0-50% |

Moderate |

|

10 |

Active Asset Allocation Balanced Fund |

30-70% |

30-70% |

0-40% |

Moderate |

|

11 |

Secure Opportunities Fund |

0% |

60-100% |

0-40% |

Low |

|

12 |

Income Fund |

0% |

40-100% |

0-60% |

Low |

|

13 |

Money Market Fund |

0% |

0-50% |

50-100% |

Low |

|

14 |

Balanced Advantage Fund |

65-90% |

10-35% |

0-35% |

High |

|

15 |

Sustainable Equity Fund |

85-100% |

0-15% |

0-15% |

High |

|

16 |

Mid-Cap Fund |

85-100% |

0-15% |

0-15% |

High |

|

17 |

Mid-Cap Hybrid Growth Fund |

65-80% |

20-35% |

0-15% |

High |

|

18 |

Constant Maturity Fund |

0% |

75-100% |

0-25% |

Moderate |

|

19 |

Mid-cap Index Fund |

90-100% |

0-10% |

0-10% |

High |

|

20 |

Mid-cap 150 Momentum 50 Index Fund |

90-100% |

0-10% |

0-10% |

High |

|

21 |

Multicap 50 25 25 Index Fund |

90-100% |

0-10% |

0-10% |

High |

|

22 |

MidSmall cap 400 Index Fund |

90-100% |

0-10% |

0-10% |

High |

|

23 |

MidSmallcap 400 Momentum Quality 100 Index Fund |

90-100% |

0-10% |

0-10% |

High |

|

24 |

Smallcap 250 Momentum Quality 100 Index Fund |

90-100% |

0-10% |

0-10% |

High |

|

25 |

India Consumption Fund |

90-100% |

0-10% |

0-10% |

High |

Popular funds under the ICICI Pru Life Time Classic Plan include Maximiser V, Value Enhancer Fund, Multi Cap Growth Fund, and Blue-chip Fund, each catering to different risk-return preferences.

Many policyholders track the ICICI Pru Life Time Classic Fund Value regularly to evaluate how their selected funds are performing over time.

Also, you get to decide on how much of your investment goes into debt funds, equity funds, and balanced funds.

This plan claims to provide flexibility so that you can control and make changes to your investment as per the change in your needs and priorities with time. We will review this flexibility aspect later in this article.

In this section let’s understand what does it consists of!

This flexibility comes in 2 ways:

- Though your money is locked for the first 5 years of the policy. But you can make an unlimited number of partial withdrawals from the 6th year onwards, as long as the total amount you withdraw in a year does not exceed 20% of the Fund Value in a policy year. For eg. If your Fund value is Rs.10 Lacs, your partial withdrawal amount will be Rs.2 Lacs. Partial withdrawals are free of cost.

- You can move your investment between 25 funds (equity, debt and balanced) as per your choice. These switches can be done online and are completely tax-free. You can switch your money between funds free of cost up to 4 times in a year.

How it is done is described next…

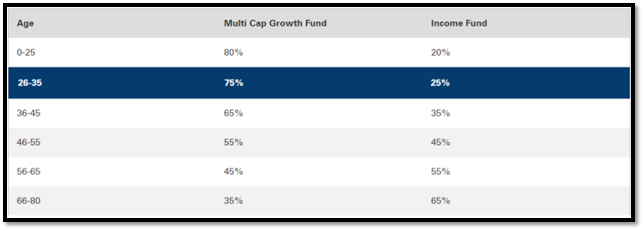

With ICICI Pru Lifetime Classic, you can choose from 4 portfolio strategies according to your investment styles to accomplish financial goals.

i. Lifecycle based Portfolio Strategy 2

In this case, you don’t need to actively manage your fund.

Here the strategy is personalized based on age. Allocation strategy with respect to age is shown below: Let’s say if you are 30 years old, then the allocation will be 75% towards Multi-Cap Growth Fund and 25% towards Income Fund.

Let’s say if you are 30 years old, then the allocation will be 75% towards Multi-Cap Growth Fund and 25% towards Income Fund.

Insight#1:

In simple words, you are giving full control to the company to manage your investments, now they will handle your money in their own ways whatever gives them the most profit.

We suggest you not get into this trap!!

ii. Fixed Portfolio Strategy

Here you have the flexibility to invest in your choice of 5 Equity, 2 Debt and 2 Balanced funds to get the potential for better returns over the policy term.

You can change the allocation whenever you want or you can apply in the company and ask the Fund Manager of ICICI Prudential to do it for you.

iii. Target Asset Allocation Strategy

This strategy allows you to select the asset allocation that best suits your risk appetite and retain it throughout the policy term.

You can split your premiums between any 2 of the funds in any proportion you want.

To guarantee that this asset allocation is maintained, your portfolio will be rebalanced every quarter.

On the last day of each policy quarter, the units must be rebalanced.

This option is available at policy inception or at any time during the policy term.

iv. Trigger Portfolio Strategy 2

The Trigger Portfolio Strategy 2 allows you to take advantage of significant equity market movements by investing on the “Buy low, Sell high” principle.

In this strategy, your money will be split 75:25 between two funds: Multi Cap Growth Fund, which is an equity-oriented fund, and Income Fund, which is a debt-oriented fund.

The ICICI Prudential Trigger Portfolio Strategy is designed to automatically rebalance investments during major market movements, although its effectiveness depends on market conditions and execution.

Insight#2: Our take on these strategies

Through all these 4 options you are giving control over your investment to the company in different ways.

There are better options available than the above 4 listed strategies.

We will discuss them in the analysis section later in this article.

- Tax benefits:

ICICI Pru LifeTime Classic and other ULIPs have the following tax-saving advantages under the IT Act 1961.

Tax benefits on premiums: You can get tax benefits up to Rs. 1.5 lakh on your insurance premiums, under Section 80C.

Tax-free maturity: The money you receive at the end of the policy or death of the policyholder is tax-free as per Section 10(10D).

The tax benefits available under ICICI Prudential Lifetime Classic are similar to those offered by many other ULIPs, subject to prevailing income tax regulations.

Note: The Finance Act, 2021, introduced certain provisions through amendments to Section 10(10D) to amend the taxability of ULIP maturity proceeds.

If you have paid a premium over Rs 2.5 lakh for any of the years during the tenure of the ULIP, then the amount received (including the bonus) at the time of maturity will be taxable.

- Bonuses:

In this scheme, there are 2 kinds of bonuses are available for you in the form of

- Loyalty Additions, and

- Wealth Boosters for staying invested longer. Bonuses are paid only after the payment of 5 years of premium.

Below are the company claims regarding these bonuses:

- Each Loyalty Addition will be a percentage of the average of daily Fund Values including Top-up Fund Value, if any, in that same policy year as mentioned in the table below.

- Wealth Boosters will be a percentage of the average Fund Values including Top-up Fund Value, if any, on the last business day of the last eight policy quarters.

- Loyalty Additions and Wealth Boosters will be allocated among the funds in the same proportion as the value of total units held in each fund at the time of allocation.

- The allocation of Loyalty Additions and Wealth Boosters is guaranteed and shall not be revoked by the Company under any circumstances.

- If the premium payment is discontinued any time after 5 years, the number of years for which premiums have been paid will be considered as the premium paying term to decide the Loyalty Additions & Wealth Boosters to be paid for the rest of the policy term as per the table above.

Let’s take a look at other features and flexibility options provided by ICICI Pru Lifetime Classic in the next section.

ICICI Pru Lifetime Classic Plan: Other Features

Fund Switch:

You can switch your investment between 25 funds (equity, debt and balanced) as per your choice.

You can switch your money between funds for free, up to 4 times each year.

In the event that you use more than 4 free switches in a policy year, you will be charged Rs.100 per switch.

The minimum switch amount is 2,000.

Top up:

If you have extra money that you’d want to put into this plan, you can do so at any point before the policy’s last 5 years.

Please keep in mind that from the date of Top Up, there will be a 5-year lock-in period.

You must top up with a minimum of Rs. 2,000 each transaction.

Increase/Decrease of Sum Assured:

If all due premiums have been paid to date, you can choose to increase or decrease your Sum Assured at any policy anniversary during the policy term.

Your insurance premium will not rise as a result of this.

Change in Portfolio Strategy:

You can change your portfolio strategy free of cost up to 4 times during the policy year.

Partial Withdrawal:

From the 6th year onwards, you can make an unlimited number of partial withdrawals as long as the total amount you withdraw in a policy year does not exceed 20% of the Fund Value.

Partial withdrawals are free of cost and are allowed only if the Life Assured is at least 18 years.

Each partial withdrawal must be worth at least Rs. 2,000.

As mentioned above, the ICICI Pru Lifetime Classic Plan offers guaranteed bonuses and a variety of flexible options.

However, there are complex charges in this plan that may outweigh the advantages of this plan, adding to the plan’s disadvantages.

ICICI Pru Life Time Classic Brochure: What Should You Check Before Investing?

Before purchasing the ICICI Pru Life Time Classic Policy, it is important to carefully review the product brochure rather than relying solely on benefit illustrations.

Pay special attention to the policy charges, including Premium Allocation Charges, Fund Management Charges, Policy Administration Charges, and Mortality Charges, as these can significantly impact your long-term returns.

You should also review the lock-in period, surrender conditions, partial withdrawal rules, available fund options, portfolio strategies, and the terms governing Loyalty Additions and Wealth Boosters.

Understanding these details will help you assess whether the policy aligns with your financial goals, risk appetite, and investment expectations before making a long-term commitment.

2.) Charges under ICICI Pru Lifetime Classic

i.) Premium Allocation Charge:

It is determined by two factors: Premium Payment Mode and Premium Payment Option.

Prior to the allocation of fund units, the Premium Allocation Charge is deducted.

As a result, it consumes a large portion of your investment capital.

This charge is based on a percentage of the premium.

- Single Pay: 3%

- Limited Pay and Regular Pay:

For annual mode of premium payment

For other than annual mode of premium payment

To understand the true impact of Premium Allocation Charges and Mortality Charges, investors should evaluate the net return rather than focusing solely on projected fund growth.

ii.) Fund Management Charge:

The Fund Management Charge is a percentage of the fund’s value that is deducted from the NAV (Net Asset Value) on a daily basis.

iii.) Policy Administration Charge:

It is imposed every month, regardless of market conditions, by the cancellation of your fund units.

- Single Pay: 60 p.m. (720 p.a.) for the first five policy years.

- Other than Single Pay:

It’s also important to note that this charge will be applied throughout the policy’s term.

iv.) Mortality Charge:

Every month, the ICICI Pru Life Time Classic plan redeems your fund units based on the Sum at Risk.

For all One Pay policies, Limited Pay policies, and Regular Pay policies with a entry age of 50 years or more.

Sum at Risk = Highest of,

- Sum Assured,

- Fund Value (including Top-up Fund Value, if any),

- Minimum Death Benefit

Less

- Fund Value (including Top-up Fund Value, if any)

For Limited Pay and Regular Pay policies with age at entry less than 50 years.

Sum at Risk = Highest of,

- Sum Assured, including Top-up Sum Assured, if any

- Minimum Death Benefit

Below are indicative annual charges per thousand life cover for a healthy male and female:

These are the pre-expenses in this policy which are being adjusted with bonuses such as Loyalty Additions and Wealth Boosters which are paid to you.

Charges for a 35-year-old investing Rs. 5,000 per month under Regular Pay works out as follows, after adjusting the Bonuses. Let’s take an example, if the Loyalty Addition is 0.1% for the 10-year Policy Term, with Premium Payment Term of 5 years.

Let’s take an example, if the Loyalty Addition is 0.1% for the 10-year Policy Term, with Premium Payment Term of 5 years.

Then the effective charge under this policy will be 2.14%.

But after adjusting the Loyalty addition in this charge, the policyholder will have to pay the effective charge of 2.04%!!

Insight#3

1. There is no point in declaring the Loyalty Addition which is simply getting adjusted with the expenses within this policy.

2. These are all the expenses in this policy, that will get deducted from your premiums.

3.) ICICI Pru Lifetime Classic: Review of Benefits

Review of Death Benefits

These are the benefits that will be paid to the nominee in case of death of the policyholder during the policy term.

A = Sum Assured including Top-up Sum Assured, if any (reduced by applicable partial withdrawals, if any)

B = Fund Value including Top-up Fund Value, if any

C = Minimum Death Benefit will be 105% of the total premiums paid including Top-up premiums if any.

Death Benefit for Single Pay Policies – Higher of A or B or C

Death Benefit for Limited & Regular Pay Policies (entry age < 50) – Higher of (A+B) or, C

Death Benefit for Limited & Regular Pay Policies (entry age => 50) – Higher of A or B or C

Insight#4

As you can notice from the above description, how much complexity this company has put into the death benefits!!

In one option they claim to provide 105% of the total premiums paid.

It simply means you will get back all your premiums (100%) plus a little more(5%)!

A common criticism in many ICICI Lifetime Classic Policy Reviews is that the complexity of charges and benefits can make it difficult for investors to estimate their actual returns.

ICICI Pru Lifetime Classic Vs Term Insurance

Let’s say if you have paid your premiums of Rs. 5000 p.m. for 10 years.

The total amount of premium paid will be Rs. 6 Lacs and in case of death, the nominee will receive 105%, that is, Rs. 6.3 Lacs as the death benefit.

Do you think it is a sustainable income after the death of a sole breadwinner of a family?

Whereas, in the case of Term Insurance, you can simply choose any insurance amount. Let’s say if you take term insurance of Rs. 1 Crore; here you only have to pay around Rs. 10,000 in a year, that is, approx Rs. 850 p.m.

So it is clearly proven that ICICI Pru Lifetime Classic Plan comes as a disadvantage to your investment plan and the Term Insurance comes as an advantage based on our above comparison.

So which one would you choose?

Review of Maturity Benefits

On maturity of the policy, you will receive the Fund Value including the Top-up Fund Value, if any.

You will have an option to receive the Maturity Benefit as a lump sum or as a structured pay-out using the Settlement Option.

For more details on pay-outs, you can refer to the product brochure.

Now let’s have a quick look at the basic eligibility criteria of this plan, then we will take an illustrative example to get better insights into this policy.

4.) ICICI Pru Lifetime Classic: Basic Eligibility Criteria

- Minimum and maximum age of entry is given below

- There are 3 Premium Payment options: Single Pay, Limited Pay, and Regular Pay. They come with the premium payment term as shown below:

- If you choose to pay your premiums through Limited or Regular Pay, you can choose any policy term shown in the table below, based on your current age

- Whereas, if you pay your premiums as a Single Pay, below are the policy terms available in years, subject to the maximum maturity age.

- The minimum and maximum amount of premium you can pay and the payment mode is given below:

- Minimum and Maximum Sum Assured for the Single Pay option is calculated as shown below:

- Minimum and Maximum Sum Assured for the Limited Pay and Regular Pay options is calculated as shown below:

- Premium and any benefits amount received under the policy will be eligible for tax benefit as per the prevailing income tax rules.

Investors looking for long-term market-linked growth often compare ICICI Pru Lifetime Classic with other ULIP policies based on fund performance, charges, and withdrawal flexibility.

5.) ICICI Pru Lifetime Classic: Illustration

In this section, we will discover and review the actual return(IRR) of this ICICI Pru Lifetime Classic, with the help of an illustration.

Let’s say Shahul is 30 years old, he wants to invest Rs. 1,00,000 p.a. for the premium, payment term of 15 years.

He is choosing a policy term of 15 years.

Putting all these values in ICICI Pru Lifetime Classic calculator, we will get the estimated returns as shown in the below snapshot.

As you can notice, the estimated returns are:

- Rs. 18.59 Lacs for 4% Assumed Rate of Return, and

- Rs. 25.67 Lacs for 8% Assumed Rate of Returns

Returns are non-guaranteed.

The ICICI Prudential Life Time Classic Return Calculator illustrates projected values at 4% and 8% rates of return, but the actual maturity value may differ depending on market performance and policy charges.

We will calculate the ICICI Pru Lifetime Classic IRR (Internal Rate of Return), by considering the assumed rate of return as 8% p.a. it is shown below:

|

At 8% p.a. |

|||

|

Age |

Year |

Annualised premium / Maturity benefit |

Death benefit |

|

30 |

1 |

-1,00,000 |

10,00,000 |

|

31 |

2 |

-1,00,000 |

10,00,000 |

|

32 |

3 |

-1,00,000 |

10,00,000 |

|

33 |

4 |

-1,00,000 |

10,00,000 |

|

34 |

5 |

-1,00,000 |

10,00,000 |

|

35 |

6 |

-1,00,000 |

10,00,000 |

|

36 |

7 |

-1,00,000 |

10,00,000 |

|

37 |

8 |

-1,00,000 |

10,00,000 |

|

38 |

9 |

-1,00,000 |

10,00,000 |

|

39 |

10 |

-1,00,000 |

10,00,000 |

|

40 |

11 |

-1,00,000 |

10,00,000 |

|

41 |

12 |

-1,00,000 |

10,00,000 |

|

42 |

13 |

-1,00,000 |

10,00,000 |

|

43 |

14 |

-1,00,000 |

10,00,000 |

|

44 |

15 |

-1,00,000 |

10,00,000 |

|

45 |

25,67,000 |

||

|

IRR |

6.46% |

||

As shown in the above table, Shahul is paying Rs. 1,00,000 p.a. for the Premium Payment Term of 15 years, starting from the Year 2025 until his policy mature after 15 years, that is, in Year 2040!

Remember we are taking the best-case scenario at 8% Assumed Rate of Returns into account, so we are getting a 6% return rate, as a resulting IRR…

Based on this observation, if we take 4% as an assumed rate of return, the IRR will be just 2%!!

Based on the illustration, the ICICI Lifetime Classic Policy delivers returns that are lower than the assumed fund growth because of various policy-level charges deducted throughout the tenure.

Please note that all these returns are non-guaranteed and depend on the fund performance in the particular year!!

We have already discovered the actual returns(IRR) of this plan.

However, to provide a complete review of this plan, it is necessary to analyze and compare the ICICI Pru Lifetime Classic Plan Pros, Cons, and Returns to some other competent Fund.

6.) ICICI Pru Lifetime Classic: Analysis and Review

In this section we will review a couple of important aspects of this policy:

i. Lower Returns

As you have seen in the illustration that ICICI Pru Lifetime Classic provides the actual return(IRR) of 6% in the best-case scenario.

That is, if this policy is able to generate 8% (Rate of Returns), then you may get 6% (non-guaranteed returns).

But, due to additional pre- and post- expense charges within this policy you will end up getting the returns in the range of 2% to 6%!

Moreover, if you are looking for higher returns from the funds then why not consider investing in ELSS Mutual Funds?

Here’s a comparison of ICICI Pru Lifetime Classic Returns VS ELSS Mutual Fund Returns.

Comparison of ICICI Pru Lifetime Classic Plan against ELSS Mutual Funds:

ELSS Mutual funds will start generating returns from the time you start investing in them.

Therefore, our advice to you is:

If you have a high risk tolerance and looking for an investment aspect to grow your money, then start investing in Mutual Funds instead of investing in this ULIP.

In Mutual Fund you will get the highest level of flexibility and you will experience better control over your investment.

Investors looking for long-term wealth creation should compare ICICI Pru Lifetime Classic ULIP with direct mutual fund investments before making a decision.

You can read this Comprehensive Guide to Mutual Fund Investment to find the right pick for you.

Let’s say if you invest 1 lakh p.a. in ELSS Mutual Funds for 15 years.

The returns from Mutual Funds are shown below.

|

Age |

Year |

ELSS |

|

30 |

1 |

-1,00,000 |

|

31 |

2 |

-1,00,000 |

|

32 |

3 |

-1,00,000 |

|

33 |

4 |

-1,00,000 |

|

34 |

5 |

-1,00,000 |

|

35 |

6 |

-1,00,000 |

|

36 |

7 |

-1,00,000 |

|

37 |

8 |

-1,00,000 |

|

38 |

9 |

-1,00,000 |

|

39 |

10 |

-1,00,000 |

|

40 |

11 |

-1,00,000 |

|

41 |

12 |

-1,00,000 |

|

42 |

13 |

-1,00,000 |

|

43 |

14 |

-1,00,000 |

|

44 |

15 |

-1,00,000 |

|

45 |

38,56,537 |

|

|

IRR |

11.11% |

The future value of your investment will be Rs. 4,175,328/- (Pre-tax value – assumed at 12% CAGR).

Whereas if you invest the same amount in this ULIP, your corpus will remain exactly the same, you may get some non-guaranteed benefits.

However, I must admit that, despite the ELSS Mutual Fund’s 1.5 lakh exemption under Section 80C, the return is not totally tax-free.

Is the LTCG tax going to affect the ELSS Mutual Fund Returns?

ELSS Mutual Fund Post-Tax Return:

|

ELSS Tax Calculation |

|

|

Maturity value after 20 years |

41,75,328 |

|

Purchase price |

15,00,000 |

|

Long-Term Capital Gains |

26,75,328 |

|

Exemption limit |

1,25,000 |

|

Taxable LTCG |

25,50,328 |

|

Tax paid on LTCG |

3,18,791 |

|

Maturity value after tax |

38,56,537 |

The ELSS Mutual Fund has a post-tax return of 38.56 lakhs.

Even after deducting the 12.5% LTCG tax, the ELSS returns are still 12.89 lakhs higher than the ICICI Pru Lifetime Classic Returns.

Therefore, you should not consider any ULIP as your investment vehicle.

You can watch this video for more details.

And, if you want a good Insurance scheme, then you should look for Term Insurance Plan.

Read this cheat sheet to select the best term insurance plan for you.

Also, have a look at our reviews on HDFC Life Click 2 Protect 3D Plus and ICICI Pru iProtect Smart Policy.

ii. Complexity

This policy or any other ULIP basically provides 2 functions: investment and insurance.

The company has made it complex in such a way that it will work only in their own favour.

They have created and presented this policy in such a way that a common man will be lured to take it up in the expectation of something magical after 5 years!

But, the truth is they are slowly taking full control over your money and all the investment.

Though they have given 4 investment strategies for you to choose; but these strategies themselves are created by them!!

In Death benefits, this policy has given you multiple options to declare the final post-death pay-out amount to the nominee.

Whereas in Term insurance you can pay a much lower premium to get the cover of a higher amount and there is a faster settlement of claims in Term Insurance schemes.

Our advice to you is to take up a separate Investment and Term Insurance scheme for yourself, instead of investing in this Complex product which comes with significantly higher charges.

iii. No Transparency in the charges and the returns

In the earlier section, you have seen the charges under this policy are approx. 2% of the fund value for the policy term of 10 years, for someone who is 35 years old and pays Rs. 5000 per month.

Now how it will vary if we increase the premium amount or age, it is not clear!!

Also, on what basis does the returns are calculated by the online calculator is not clear!!

The ICICI Pru Lifetime Classic calculator will display the return rates at 4% and 8% assumed rate of return, but you will never know how much return you will get!!

7.) ICICI Pru Lifetime Classic: Disadvantages

In the earlier sections, we have already mentioned key features, benefits along with detailed illustration and analysis.

Now let’s have a look at the disadvantages of this policy:

- This policy has a fixed lock-in period of 5 years. That is, you can’t touch your money for the first 5 years in this policy. 5 years is a long period!!

- Charges are not transparent.

- Estimated Returns range between 2% to 6% and none of them are guaranteed.

- You will start receiving bonuses only after completing 5 years in this policy, which doesn’t make any sense.

- By investing in this ULIP you are giving complete control of your money to the policy managers, their ways of calculating the returns are not transparent.

- ULIPs are regulated by IRDA. And, IRDA’s regulations are predominantly focused on the Insurance aspect rather than the investment aspect. The investment aspect is monitored by SEBI and SEBI has no role to play in ULIPs.

In the next section, we will answer some common queries on this policy.

8.) Common Queries on ICICI Pru Lifetime Classic

i. Is ICICI Pru Lifetime Classic a good Policy?

It is not a recommended policy. It gives you non-guaranteed returns in the range of 2% to 6%.

Also, you have to pay the higher charges to keep your policy going. You can check the detailed analysis in this article.

ii. Is it possible to increase or decrease the policy term or Premium Payment Term?

Yes, it is possible to change the Policy Term or Premium Payment Term, provided that you have paid all your earlier premiums on time.

You can change the term by contacting the company.

iii. What is the Top-up option in ICICI Pru Lifetime Classic? Is it recommended?

According to the Top-Up option, if you have excess savings that you want to invest in this plan, you can do so at any time before the last 5 years of the policy term.

Please keep in mind that there will be a lock-in period of 5 years from the date of Top Up.

You will have to top up with a minimum of Rs. 2,000 at a time.

No, it is NOT recommended to opt for the top-up.

iv. How to surrender/cancel ICICI Pru Lifetime Classic?

You can cancel and withdraw your money completely from the policy at the end of the lock-in period of 5 years.

- If you surrender before the lock-in period, then Fund Value including Top-up Fund Value, if any, after deduction of applicable Discontinuance Charge, shall be transferred to the Discontinued Policy Fund (DP Fund).

- If you surrender after the lock-in period, you will be entitled to the fund value including Top-up Fund Value, if any.

9.) Is ICICI Pru Lifetime Classic Plan Good or bad?

Though this policy claims to bring a lot of good features of investments, where you have the flexibility to choose your own fund among equity, balanced, or debt funds.

But if your focus is on flexibility then why not choose the highest level of flexibility?

Therefore, instead of choosing investment funds through this ULIP, why not choose your most preferred fund directly through Mutual Fund; if you are planning for long term investment of 5+ years.

Mutual Funds will provide the highest degree of flexibility without any fixed lock-in period.

So, our advice is to keep your investment and insurance as a separate vehicle.

Therefore, you should avoid investing in this ULIP and invest in a standalone Mutual Fund and Term Insurance separately.

After reviewing the benefits, charges, fund options and projected returns, our ICICI Prudential Life Time Classic Review suggests that investors may find more efficient alternatives by keeping insurance and investments separate.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30 Minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

I have paid 5 primiums and lock up period is over , fund value is 5.70 lac after 6 yrs and paid 5 Lac.( Five out of 7). Please suggest should I hold as is , pay next two primium or withdraw and invest some where else.

Also suggest if fund value will increase with time.

Hi, what did you do? I’m in the same situation now. Paid 5/7 premiums and lock in period is over. What is the benifit/loss of I surrender now? Paid 5L and fund at 6.9L now. Will I be getting the full 6.9L if I withdraw?

“Thanks for sharing your situation. 🙏

If your lock-in period is already over, in most cases you should be eligible to receive the prevailing fund value on surrender. However, the exact amount depends on factors such as policy terms, fund value, surrender rules, tax implications, and whether any charges are applicable.

Since you’ve paid ₹5L and the fund value is ₹6.9L, it’s worth evaluating the numbers carefully before taking a decision.

👉 Feel free to book a free consultation and we’ll help you review the policy objectively:

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

A proper analysis can help you decide whether to continue or surrender based on your goals and overall financial plan.”

I already paid premium for 2 years. should I discontinue now? if i discontinue now how much i will get after 5 years. now my fund value is 102000/-rs.

Since it is a ULIP plan, you will get the fund value as of the date of surrender. However, you will get a refund only after the end of the lock-in period.

Information about policy given precisely..even icici bank employees not given this much information…

Thank you

I have invested in this policy for the last three years i.e. 5K per month. For the first two years the returns were negative. I was actually losing money. Now at the end of third year, I have 1% in returns. So ~1.75 lac invested I now have a total of ~1.76 lac. An recurring deposit pays much better interest than this.

Even in future I’m not expecting anything magical happen which would double or even slightly increase the amount.

Based on your knowledge can you suggest how do I get out of this with minimal loss and invest in something better?

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the times, option 1 is better.

As for the investment option, you can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Nice article

Can we switch to other from this ULIP to mutual funds ?

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners regarding your personalized investment plan.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Approximately, how much refund will be paid and when if I end the policy just now.

Policy Details

Total instalment premium (Rs.) 1,20,000

Policy Term (In Years) 10 Periodicity of Payment of Premium Yearly

Risk Commencement Date July 22, 2019 Premium Payment Term (In Years) 7

Maturity Date July 22, 2029 Premium Payment Option Limited Pay

Policy sourced by Distance Marketing N Due date of Last Premium July 22, 2025

Category Non-Medical Sum Assured (Rs.) 8,40,000

Since it is a ULIP plan, you will get the fund value as of the date of surrender. However, you will get a refund only after the end of the lock-in period.

I AM ALREADY PURCHASE THIS POLICY, NOW AFTER READING YOUR REVIEW, I M CONFUSED. SO WHAT CAN I DO NOW, CAN I WITHDRAWAN MY MONEY NOW OR AFTER FIVE YEARS.

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the times, option 1 is better.

As for the investment option, you can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

I have already paid 3 premiums now what would be the wisest decision further with this policy?

Please check with your financial planner.

You can also book a slot with our financial planner for an initial complimentary consultation.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/