ICICI Pru Easy Retirement is a Unit Linked pension plan or ULPP. ULPPs are similar to ULIPs but they do not

In this article, we will analyze its key features in-depth, which will help you to make the right buying decision.

Table of Content

- ICICI Pru Easy Retirement Plan: How does it work?

- Eligibility conditions in ICICI Pru Easy Retirement Plan

- ICICI Pru Easy Retirement Plan: Key Features and Insights

- ICICI Pru Easy Retirement Plan: Illustration

- ICICI Pru Easy Retirement Plan: Analysis & Review

- ICICI Pru Easy Retirement Plan Vs. Other Alternatives

- ICICI Pru Easy Retirement Plan: How to cancel this policy?

- Conclusion

ICICI Pru Easy Retirement Plan: How does it work?

You can sign up for a pension either through a single premium or through regular premiums. There is a fixed lock-in period of five years.

The plan passes through 2 phases, elaborated below:

Accumulation Phase

In the accumulation phase, you have to pay the premiums for your chosen premium paying term and this way the funds for your retirement will get accumulated. You can also invest any available residual money you might have through the Top-up option in this plan.

Income Phase – you can choose vesting age (or your retirement age) from any of the below options –

-

- Regular Income – Purchase an annuity with the accumulated value and receive regular income.

- Commutation Plus Regular Income – receive lump sum amount up to one-third of the accumulated amount and the balance can be used to buy the annuity for providing you the regular income.

- Postponement of vesting age – It provides the flexibility to change the vesting date, provided the age is below 55 years.

- Invest in a single premium deferred pension product – use the accumulated amount to purchase a single premium deferred pension product.

Insight#1: Though there are 4 different options for you to choose from in the income phase BUT you should not make any buying decision based on these options.

At this point, please understand and analyze this overall plan in greater detail, before even considering their way to pay!!

Eligibility conditions in ICICI Pru Easy Retirement Plan

ICICI Pru Easy Retirement Plan: Key Features and Insights

Lock-in Period: There is a fixed lock-in period of 5 years in this plan. In case, if you want to surrender the plan or stop paying premiums in this time period, your money will be moved to the Pension Discontinued Policy Fund after deducting discontinuance charges, where it earns 4% per year. It remains in the fund for a period of five years and thereafter it will be paid out to you.

How your funds will be Invested?: This plan allows you the choice of two fund options. You can switch between these funds using the switch option provided in this plan. The details of the funds are given in the table below:

Sum Assured: At maturity, you will get at least 101% of the sum of all the premiums that you have invested. It simply means you will get your premiums back plus 1% additional money!!

Sum Assured: At maturity, you will get at least 101% of the sum of all the premiums that you have invested. It simply means you will get your premiums back plus 1% additional money!!

Flexibility in choosing Premium Paying Term: You have an option to pay premiums for 5 years, 10 years or throughout the policy term.

Partial withdrawal: This policy does not allow partial withdrawals.

Death Benefits: Guaranteed Death Benefits are 105% of all the premiums paid.

Insight#2: There is no point taking up Death Benefits from this Plan, here you are simply getting the premiums that you have paid, these are the benefits WITH COST. We suggest you to choose a Term Insurance to get the life cover of the higher amount and lower premium, it will be discussed later in this article.

Pension Boosters: There will be guaranteed pension boosters on completion of the 5th & 10th policy year, they will be allocated between Easy Retirement Balanced Fund and Easy Retirement Secure Fund, at 5% of the average daily fund value over the preceding 12 months.

Insight#3: Pension Boosters is a small addition which only starts from 10th Policy year and added after every 5 years of the policy. In other words, it is just a hook to keep you invested for the long term!

Top Up Option: You have an option to put additional savings to boost the fund value. Top-up will be added along with your paid premium.

Income Tax Benefit – Life Insurance premiums paid up to Rs. 1,50,000 are allowed as a deduction from the taxable income each year under section 80C.

Freelook Period – If the policyholder is not convinced with the Terms and Conditions, there is a provision of canceling the policy within 15 days from the date of receipt of the policy document.

Charges Under ICICI Pru Easy Retirement Plan:

1. Premium Allocation Charge

This charge will be deducted from the premium amount at the time of premium payment and units will be allocated thereafter. Premium Allocation Charges, as percentages of premium, are as follows:

All the Top-ups are subject to Premium Allocation Charges of 2%.

All the Top-ups are subject to Premium Allocation Charges of 2%.

2. Policy Administration Charge

The Policy Administration Charge will be a percentage of the annual premium and will be levied every month for the first ten policy years. Policy Administration Charge is capped at Rs. 6,000 per annum, as required by IRDAI. These charges will be made by redemption of units. The Policy Administration Charge will be as set out below for yearly and another premium payment modes:

3. Fund Management Charge (FMC)

The following Fund Management Charge will be adjusted from the NAV on a daily basis. This charge will be a percentage of the Fund Value

There will be additional charges of 0.50% p.a. and 0.10% p.a. towards the investment guarantees for Easy Retirement Balanced Fund and Easy Retirement Secure Fund respectively. These charges will be adjusted from the NAV on a daily basis, like the previous one.

There will be additional charges of 0.50% p.a. and 0.10% p.a. towards the investment guarantees for Easy Retirement Balanced Fund and Easy Retirement Secure Fund respectively. These charges will be adjusted from the NAV on a daily basis, like the previous one.

Insight#4: Above are the 3 solid charges that will get deducted from your annual premium amount: Premium Allocation Charge, Policy Administration Charge, and Fund Management Charge. All these charges will sum up to 5% with an additional 2% charge on top-ups if you have any.

In other words, you are paying more charges than the benefits you are getting from this policy!

4. Switching Charges

Four free switches are allowed every policy year. Subsequent switches would be charged `100 per switch. Any unutilized free switch cannot be carried forward to the next policy year. These charges will be made by redemption of units.

5. Discontinuance Charges

There is a fixed lock-in period of 5 years. If you want to discontinue your policy within 5 years, the following Discontinuance Charges will be applicable:

Where AP is Annualised Premium, excluding Top-ups, if any, and FV is Fund Value excluding Top-up Fund Value, if any, as on the Date of Discontinuance.

Where AP is Annualised Premium, excluding Top-ups, if any, and FV is Fund Value excluding Top-up Fund Value, if any, as on the Date of Discontinuance.

ICICI Pru Easy Retirement Plan: Illustration

Let’s take an example with the following assumptions:-

Gender – Male,

Age – 37 years,

Policy Term – 20;

Premium Paying Term – 10 years

Annual premium – Rs.1,30,000

Assured Benefit– Rs.14,30,000,

Investment fund option – Easy Retirement Balanced Fund (100%)

We are choosing a pension option where policyholders will get the pension for a lifetime!

Using ICICI Pru Easy Retirement Plan Online Calculator, after putting above values we will get the following returns at 8% Assumed Rate of Returns:(below screenshots are taken from Online Calculator)

At 4% Assumed Rate of Returns, the returns will be as follows:

At 4% Assumed Rate of Returns, the returns will be as follows:

Following points are worth noticing from the above example:

Following points are worth noticing from the above example:

-

- The policyholder is receiving Rs. 2.93 Lacs per annum in the best case scenario, and Rs. 95,350 per annum in an average case scenario, (that is, when company is getting 4% returns from the market) and none of these returns are guaranteed!!

- The only Sum assured in this example will be 101% of the Premium paid, that is, Rs.14.3 Lacs.

- In case of the death of the policyholder during the policy, the nominee will receive 105% of the premium paid, which is Rs.1,36,500.

- Pension Boosters are guaranteed additions and they will be allocated between Easy Retirement Balanced Fund and Easy Retirement Secure Fund, at 5% of the average daily fund value over the preceding 12 months.

Its value fluctuates drastically; with the current NAV rates, we can get the approximate value of Rs.18,000 worth of Policy Booster in the 10th Policy year in the given example.

We will do a detailed analysis of this illustration and will arrive at the conclusion whether this policy is good for you or not in the next section!!

ICICI Pru Easy Retirement Plan: Analysis & Review

Since this policy invests in 2 options, Easy Retirement Balanced Fund and Easy Retirement Secure Fund. Let’s have a look at their performance till 31st Jan 2024 since their inception:

From the above data, you can see that the Easy Retirement Balanced Fund has generated 8.6% returns and Easy Retirement Secure Fund provided 9.03% returns since their inception.

From the above data, you can see that the Easy Retirement Balanced Fund has generated 8.6% returns and Easy Retirement Secure Fund provided 9.03% returns since their inception.

But there are additional charges that will be deducted from your premium as described in the earlier section. If you sum all the charge expenses, it comes out to be 5%+, which will be deducted each year from your premiums.

So, there is no way you will ever get these 8%-9% returns!!

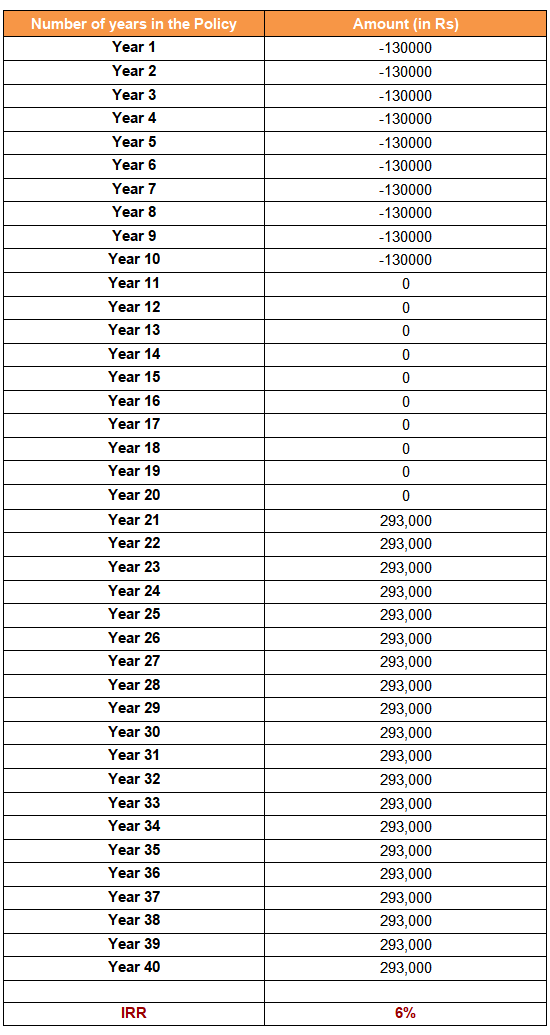

Now, let’s analyze the example we have discussed in the illustration in the previous section, with the additional assumption that the policyholder dies at the age of 77;

So, he is paying the annual premium of Rs. 1.3 Lacs for 10 years. The policy term is 20 years and after completing the policy term, he will receive his pension between 57 years and 77 years, which is for 20 years!

Let us see, how much IRR or average rate of return he will receive through this policy in all these years!!

After taking all the Premium payments and payouts into account all throughout these 40 years, we will find the average return to be only 6%!!

After taking all the Premium payments and payouts into account all throughout these 40 years, we will find the average return to be only 6%!!

Please note that these returns are considered under the best-case scenario of an 8% assumed return rate, where the payouts are Rs.2,93,000!!

However, if we take a 4% assumed rate, the annual payouts will be Rs. 95,350 and the average returns or IRR will be just 2%!!

Now, do you really think it is a good policy to invest for your retirement?

Please note all these returns are NON-GUARANTEED. The only thing guaranteed is the Sum Assured which is 101% of the premium, it comes out to be Rs. 14.3 Lacs! It simply means that you are getting all the premiums back plus 1% more on top!

ICICI Pru Easy Retirement Plan Vs. Other Alternatives:

What are the good options to choose as an alternative to ICICI Pru Easy Retirement plan?

We recommend you to invest your money in PPF or Mutual Funds to get a better value of your money and secure your retirement life.

Below are the comparative details:

(i) PPF Vs. ICICI Pru Easy Retirement Plan:

Since the minimum term in PPF is 15 years, so let’s say you are investing Rs.65,000 (half of Rs.1.3 Lacs) per annum in PPF for 20 years, which gives you the guaranteed returns of 8%. Therefore, the returns from the PPF will be Rs. 32,12,490/-.

PPF Returns after 20 years: ₹ 32,12,490

Don’t you think, these guaranteed returns are far better than the assured sum from ICICI Pru Easy Retirement Plan?

(ii) Mutual Fund Vs. ICICI Pru Easy Retirement Plan:

In case of Mutual funds, let’s say you accumulate Rs. 13 Lacs and invest this amount as a lumpsum payment in a good equity Mutual Fund that will generate 12% average returns. You can use this Mutual Fund Online Calculator to find the Mutual Fund Returns.

Mutual Fund Returns after 20 years: ₹ 1,41,60,320

Have you noticed it? You have the potential to grow your 13 Lacs up to Rs. 1.41 Crores, if only you choose to utilize your money wisely!

Below table summarizes, what we have analyzed above:

Should you purchase ICICI Pru Easy Retirement Plan? Yes or No!

Should you purchase ICICI Pru Easy Retirement Plan? Yes or No!

There is NO point in taking up this Plan. It is simply a ULIP, being sold under a Retirement Plan. You will end up loosing money in this plan!

We recommend you to invest your money in PPF or Mutual Funds to get a better value of your money and secure your retirement life.

Along with your investment, we suggest you take up a separate Term Insurance Policy. You can read this cheat sheet to select the best term insurance plan for you. Also, have a look at our reviews on HDFC Life Click 2 Protect 3D Plus and ICICI Pru iProtect Smart Policy. These articles will help you to choose a better Term Insurance Policy for you!

ICICI Pru Easy Retirement Plan: How to cancel this policy?

There is a free-look period for 30 Days, if you have purchased this policy through Distance Marketing mode. Distance Marketing means:

-

- (i) Voice mode, which includes telephone-calling

-

- (ii) Short Messaging service (SMS)

-

- (iii) Electronic mode which includes e-mail, internet and interactive television (DTH)

-

- (iv) Physical mode which includes direct postal mail and newspaper & magazine inserts and

- (v) Solicitation through any means of communication other than in person

If you have taken this policy from ICICI Pru Branch office or through any agent, there will be the Free Look Period of 15 Days.

In case, if you have crossed your free-look period and you want to discontinue, then you must know that there is a fixed lock-in period of 5 years. If you want to discontinue your policy within 5 years, the Discontinuance Charges will be applicable as defined in the earlier section.

To surrender your policy, you can visit the nearest ICICI Prudential Life branch with these documents:

-

- 1.

-

- 2. Policy Documents.

-

- 3. Signed Copy of Photo Identity Proof of the policy holder, i.e. PAN Card, Aadhaar Card etc. Please carry an original copy of the Identity proof.

- 4. Cancelled Cheque of the Bank account in which you wish to receive the surrender amount. Please ensure that your name is printed on the cheque.

For more details you can have a detailed look at the product brochure.

Conclusion

You should avoid taking up ICICI Pru Easy Retirement Plan, this plan consumes a higher premium from your side along with significant charges associated with the policy.

The company is simply selling you a ULIP in the name of the Retirement Plan. The guaranteed Sum is 101% of the premium paid, and if you consider the 6% p.a. inflation aspect, you are losing your hard-earned money with this policy!!

You should rather invest in Mutual Fund and Term Insurance as the standalone policies, where you will gain more and experience the true value of your money as discussed in the analysis section above!!

If you have any more queries on this policy feel free to drop them in the comment below.

To get the suggestion about the right investment and insurance policy customized for your needs, you can book the FREE Complimentary Consultation Call with us by clicking the link below:

I for all time emailed this weblog post page to all my contacts, since if like

to read it next my contacts will too.

Hey there, You have done a fantastic job.

I will definitely digg it and personally suggest to my friends.

I’m sure they’ll be benefited from thus web site.

Excellent site you have got here.. It’s difficult to find high quality writing like yours nowadays.

I seriously appreciate individuals like you! Take care!!

I have taken the Easy Retirement plan dated 18/10/2019

Yearly premium Rs.2,00,000

Premium payment term – 5 years

Policy Term – 10 years

I want to surrender. The ICICI branch has counselled for payment of 2nd premium of Rs.2,00,000 on 18/10/2020 and thereafter await expiry of lock in period of 5 years (which is compulsory) to gain more benefits. I wish to take full exit (I do not want Pension or Annuity payment).

Kindly advise whether I should pay the 2nd premium as advised. What is the easiest and quickest way to exit?

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the times, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here!

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/