Everyone wants to lead a peaceful life after retirement.

But a peaceful life at a period where you are unemployed, still needs a regular stream of guaranteed income.

This regular income is important to maintain your current lifestyle and to meet any of your medical expenses.

SBI Saral pension is an immediate annuity plan. It provides you with a regular income, with the return on the purchase price, without letting you make any compromises.

Can this plan be relied upon to have a golden retirement life?

Let us dive deep into this plan to better frame our judgement.

Table of Contents:

1.) What is SBI Life – Saral Pension Plan?

2.) Features of SBI Life – Saral Pension Plan

3.) Eligibility Criteria of SBI Life – Saral Pension Plan

4.) Annuity Options of SBI Life – Saral Pension Plan

5.) Other options of SBI Life – Saral Pension Plan

6.) Free look-up period of SBI Life – Saral Pension Plan

7.) Surrendering/Cancelling your SBI Life – Saral Pension Plan

8.) Advantages of SBI Life – Saral Pension Plan

9.) Disadvantages of SBI Life – Saral Pension Plan

10.) SBI Life Saral Pension Plan Taxation Explained

12.) IRR of SBI Life – Saral Pension Plan

13.) SBI Life – Saral Pension Plan Vs Other Investment Choices

14.) An Overview of Retirement Plan – Investment Strategy

What is SBI Life – Saral Pension Plan?

SBI Life – Saral Pension Plan is a single premium, individual, non-linked, non-participating, immediate annuity product.

It claims to provide you with regular income, with the return on purchase price. It also offers a Joint life option to cover your spouse as well.

It secures your retirement life with the guaranteed regular income to meet all your expenses including your medical expenses.

Many retirees exploring SBI pension plans for senior citizens prefer such annuity structures for predictable post-retirement income, especially when compared with volatile market-linked investments.

Features of SBI Life – Saral Pension Plan:

-

- It is a single premium plan.

- You can choose the annuity mode at inception – Monthly, Quarterly, Half-yearly or yearly.

- You can use your life cover individually or you can choose to cover your spouse as well in joint life option.

- Steady cash flow throughout the life of the annuitant.

- The purchase price (premium paid) is returned to the nominee or legal heir.

- You have the option to avail of the loan facility in case of any financial need.

- You have the option to avail the surrender facility on being diagnosed with a specified critical illness.

Eligibility Criteria of SBI Life – Saral Pension Plan:

|

|

Minimum |

Maximum |

|

Age at Entry |

40 Years |

80 Years |

|

Premium |

Such that the minimum annuity instalment can be paid as per the annuity payment mode. |

No limit, as per Board Approved Underwriting Policy |

|

Minimum Annuity Pay-out (per instalment) |

Monthly: ₹1,000 |

No limit, as per Board-approved Underwriting Policy |

|

Premium Payment Term |

Single Premium |

|

|

Annuity Payment Mode |

Monthly or Quarterly or Half-Yearly, or Yearly |

|

This flexibility makes the SBI Saral Pension Plan suitable for retirees who want pension income aligned with their monthly or yearly household expense requirements.

Annuity Options of SBI Life – Saral Pension Plan:

1.) Life Annuity with Return of 100% of Purchase Price (ROP):

Annuity is payable in arrears at a constant rate throughout the life of the Annuitant. On death of the Annuitant, all the future annuity pay-outs cease immediately and the purchase price is refunded to the nominee/legal heirs.

2.) Joint Life Last Survivor Annuity with Return of 100% of Purchase Price (ROP) on the death of the last survivor:

On the death of the primary annuitant, if the spouse is surviving, the spouse continues to receive the same amount of annuity for life until his/her death. On the death of the last survivor, the purchase price shall be payable to the nominee/legal heirs.

If the spouse has pre-deceased the primary annuitant, then on the death of the primary annuitant, the Purchase price shall be payable to the nominee / legal heirs.

Other Options of SBI Life – Saral Pension Plan:

Loan:

You can avail the loan option at any time after six months from the date of commencement of the policy.

Unlike many traditional pension schemes, the SBI Saral Pension Plan offers limited liquidity support through its loan feature after the lock-in period.

Higher Purchase price:

| Purchase Price Range | Price incentive per thousand Purchase Price |

| Less than 2,00,000 | Nil |

| 2,00,000 to less than 5,00,000 | Nil |

| 5,00,000 to less than 10,00,000 | 2.75 |

| 10,00,000 less than 25,00,000 | 3.75 |

| 25,00,000 and above | 4.25 |

Existence Certificate:

For annuities in payment, the Existence Certificate in the format prescribed by the Company is to be submitted by the Annuitant / Primary Annuitant / Secondary Annuitant as and when required by the Company. Annuity payments shall be released only on receipt of the Existence Certificate.

Free Look-up Period of SBI Life – Saral Pension:

If the policyholder is not satisfied with the terms and conditions of SBI Life – Saral Pension after purchasing the policy, then the policyholder can return the policy by stating the return within 15 days from the date of purchasing the policy.

The free look-up period will be 30 days if the policy was purchased through electronic mode.

Surrendering/Cancelling the SBI Life – Saral Pension Plan:

The SBI Life – Saral Pension Plan can be surrendered any time after six months from the date of commencement.

If the annuitant / primary annuitant /secondary annuitant, or spouse or any of the children of the annuitant is diagnosed to be suffering from any of the critical illnesses (as listed in the policy details), then 95% of the Purchase Price shall be paid to the annuitant. On payment of the surrender value, the policy stands terminated.

Advantages of SBI Life – Saral Pension Plan:

- Regular cash flow similar to salary structure is paid to the policyholder during the post-retirement period.

- Hassle free investment – Lumpsum investment option (one-time premium payment).

- You can avail the loan option after 6 months.

- You have the option to surrender the policy after 6 months in case of any critical illness.

- The return of purchase price is an in-built feature, which acts as a legacy to the nominee or legal heir.

Disadvantages of SBI Life – Saral Pension Plan:

- Though the income is regular, the return on investment is not on par with other fixed income products, which is available in the market.

- The annuity amount is constant throughout the policyholder’s lifetime, which may not be sufficient to meet the rising expenses down the lane.

- The annuity is taxable at the individual’s highest slab rate.

- Annuity is fully taxable. Any annuity purchased directly (other than proceeds of any pension plan like superannuation) becomes taxable under the head “Income from other sources” and not “Salaries” therefore not eligible for the standard deduction.

You can read further details of the SBI Life – Saral Pension Plan in its brochure.

SBI Life Saral Pension Plan Taxation Explained

One important factor many retirees overlook while purchasing the SBI Life Saral Pension Plan is taxation.

The annuity received from this SBI pension plan is fully taxable according to the individual’s income tax slab.

Since the pension income is treated under “Income from Other Sources”, retirees cannot claim the standard deduction benefit usually available for salary or family pension income.

This reduces the effective post-tax return from the annuity plan, especially for investors falling under higher tax brackets.

In comparison, alternatives like Senior Citizen Savings Scheme (SCSS) and bank fixed deposits may offer additional tax benefits under Sec 80TTB for senior citizens.

Therefore, while the SBI Life Saral Pension Plan provides guaranteed regular income for life, investors should also consider taxation, inflation, and liquidity before locking funds into a long-term annuity product.

Research Methodology:

Since we have all the relevant information we need, now it’s time to analyze this SBI Life – Saral Pension Plan by calculating its IRR for the two Annuity options this plan offers.

Then, let us compare the IRR of the SBI Life Insurance Child Plan with other alternate investments to see which gives you a better return in the long run.

IRR of SBI Life – Saral Pension:

Using an SBI Saral Pension Plan calculator or maturity calculator helps retirees estimate expected annuity income before making a long-term retirement commitment.

There are two options of Annuity, which we can see illustrated below at a glance.

|

Annuity Options |

Annual annuity amount |

Annuity amount as a % age of Purchase price |

Death benefit |

|

Option 1: Life Annuity with Return of 100% of Purchase price (ROP) |

62,400 |

6.24 |

10,00,000 |

|

Option 2: Joint Life Last Survivor Annuity with Return of 100% of Purchase Price (ROP) on death of the last survivor |

61,578 |

6.18 |

10,00,000 |

Investors comparing the SBI immediate annuity plan with other retirement products should carefully evaluate pay-out sustainability and inflation-adjusted income needs.

Let’s assume,

Annuitant age – 60 years.

Life expectancy – 85 years.

Now let us see the IRR for both the annuity options for the policyholder we have assumed above.

|

Age |

Option 1 |

Option 2 |

|

60 |

-10,00,000 |

-10,00,000 |

|

61 |

62,400 |

61,578 |

|

62 |

62,400 |

61,578 |

|

63 |

62,400 |

61,578 |

|

64 |

62,400 |

61,578 |

|

65 |

62,400 |

61,578 |

|

66 |

62,400 |

61,578 |

|

67 |

62,400 |

61,578 |

|

68 |

62,400 |

61,578 |

|

69 |

62,400 |

61,578 |

|

70 |

62,400 |

61,578 |

|

71 |

62,400 |

61,578 |

|

72 |

62,400 |

61,578 |

|

73 |

62,400 |

61,578 |

|

74 |

62,400 |

61,578 |

|

75 |

62,400 |

61,578 |

|

76 |

62,400 |

61,578 |

|

77 |

62,400 |

61,578 |

|

78 |

62,400 |

61,578 |

|

79 |

62,400 |

61,578 |

|

80 |

62,400 |

61,578 |

|

81 |

62,400 |

61,578 |

|

82 |

62,400 |

61,578 |

|

83 |

62,400 |

61,578 |

|

84 |

62,400 |

61,578 |

|

85 |

10,00,000 |

10,00,000 |

|

IRR |

6.13% |

6.05% |

This is one of the major SBI Saral Pension Plan disadvantages highlighted by retirees seeking inflation-beating retirement income.

For both the annuity options, the IRR works out to be around 6%, which is similar to the Bank FD rate for any individual. The bank FD rate for senior citizens is higher than this rate.

From the taxation point of view, the FD interest & the annuity, both are taxable. A deduction of up to Rs. 50000 on interest received from the Bank savings account & also Senior citizens can claim FDs under Sec 80 TTB.

Also, the bank FDs can be easily liquidated. In the rising interest rate scenario, locking funds for the long term at this rate of return is not advisable.

SBI Life – Saral Pension Plan Vs Other Investment Choices:

As the annuity is perpetually fixed till the lifetime of the annuitant, let’s compare it with other fixed income options like;

- Senior Citizen Savings Scheme (SCSS)

- Pradhan Mantri Vaya Vandana Yojana (PMVVY)

- RBI Floating Rate Bond

- Bank FD

SBI – Saral Pension plan

SCSS

PMVVY

RBI Floating rate Bond

FD

Average Return %

5.70%

8.20%

7.40%

8.05%

5.5% – 6.5%

Tenure

Perpetual

5 years

10 years

7 Years

Ranging from 12 months to 60 months

Frequency

Monthly or Quarterly or Half-Yearly or Yearly

Quarterly

Monthly or Quarterly or Half-Yearly or Yearly

Half-yearly

Monthly or Quarterly or Half-Yearly or Yearly

Maximum investment

No limit

15 lakhs

10 lakhs

No Limit

No limit

Minimum age at entry

40 years of age

60 Years of age

55 years of age to invest retirement benefit / 60 Years of age

No Limit

No limit

Annual annuity / Interest (Purchase price 10 Lakh)

₹ 62,400

₹ 82,000

₹ 74,000

₹ 80,500

Range 55K to 65K p.a

Tax benefit on investment

No benefit

Sec 80 C Rs. 1.5 lakh

Sec 80 C Rs. 1.5 lakh

No Benefit

No benefit

Taxation on income

Taxable at Slab rate

Sec 80 TTB Exempt – Rs. 50,000

Excess taxable at slab rateSec 80 TTB Exempt – Rs. 50,000

Excess taxable at slab rateTaxable at Slab rate

80 TTB Exempt – Rs. 50,000

Return of purchase price (On Maturity / Death)

Yes

Yes

Yes

Yes

Yes

Premature Withdrawal

After 6 months – On diagnosis of 20 listed critical illnesses

Allowed with a penalty

On diagnosis of critical illness, 98% of the purchase price is returned

Allowed for Senior citizens

Allowed with a penalty

Life Certificate

Required

Not required

Required

Not required

Not required

From the above, it is clear that government-backed schemes with the same fixed income options can give you better returns compared to SBI Life – Saral Pension Plan.

When compared with alternatives like SCSS, RBI Floating Rate Bonds, or the best annuity plans in India, the SBI Saral Pension Plan appears relatively conservative in return generation.

SBI Life – Saral Pension Plan doesn’t seem to give inflation-beating returns and also doesn’t seem like an adequate insurance product.

Let us look at investment strategies that could provide you with both regular incomes with better returns.

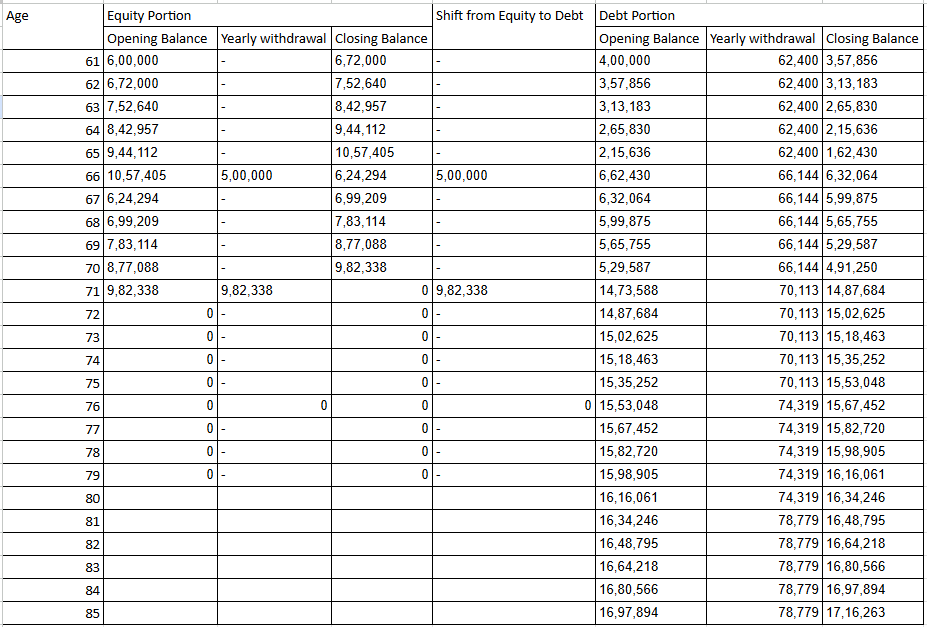

An overview of Retirement plan – Investment Strategy:

Throughout your working years, you might have built a considerable amount of corpus to be spent in the next phase of your life, which is your retirement period to help you sustain.

You must make the best use of such corpus to get an inflation-adjusted regular stream of income.

You can consider the following Investment Strategy to get an inflation-adjusted post-retirement income.

Corpus for Regular Income:

DEBT – Liquid fund (emergency corpus), Debt funds – for Systematic withdrawal (SWP), SCSS, PMVVY, RBI Bonds, Bank & Corporate deposits.

Corpus to Beat Inflation:

EQUITY – Indexed Funds, Hybrid – Aggressive, Dynamic Asset allocation fund.

A diversified retirement approach generally works better than depending entirely on a single pension policy or annuity plan for lifelong income needs.

Rebalancing your Portfolio:

Refill your debt portion once in 6 years from the equity portion. Your debt balance will remain the same as you take out the interest annually while equity might have doubled by that time.

So, rebalancing your portfolio at the regular interval mentioned above will help you to fetch higher annual withdrawal than before.

The following is an illustrative working example of the above strategy.

| Total corpus | 1,00,00,000 | ||

| Equity | 30% | Debt | 70% |

| Equity Investment | 30,00,000 | Debt Investment | 70,00,000 |

| Equity Int rate | 12% | Debt Int rate | 6% |

By following the above strategy, you will get an inflation-adjusted regular annual income. This will help you to keep pace with the inflation.

This advantage is missing in the SBI life – Saral pension plan where you get a fixed annual income throughout your life.

For conservative retirees, SBI Life Saral Pension may still provide psychological comfort through guaranteed lifelong income despite moderate return potential.

Final Verdict:

The sales pitch of any annuity scheme will be “GUARANTEED REGULAR INCOME FOR LIFE” during your post retirement period. Yes, it is a great advantage.

But if you take areas like taxation, liquidity and inflation into consideration, it makes SBI Life – Saral Pension plan look unattractive. There are other products with sovereign guarantee & better tax benefit, available in the market.

This is why many retirees compare SBI guaranteed pension plans with government-backed retirement schemes before locking funds into long-term annuity products.

The retirees should keep in mind that not only their regular cash flow but also their tax liability & corpus should outlive them.

The biggest challenge would be to build a portfolio with the right mix of various investment products. Considering the current inflation rate and the rising medical expenses, this annuity plan can’t be solely relied for your post-retirement income.

So, it would be better if you diversify across different investments & rebalance your portfolio as & when necessary to get an inflation-adjusted income during your post-retirement period.

You can also consult a Financial Advisor for better understanding as he can draft you a tailor-made retirement plan.

You can avail of our complimentary consultation with one of our financial planners by registering through the below link.

Leave a Reply