Should you look to invest in HDFC Life Sanchay Par Advantage Plan for your Financial Goals?

Is HDFC Life Sanchay Par Advantage Plan a good or bad investment choice?

HDFC Life Sanchay par Advantage Plan is a Non-Linked, Participating Life Insurance Plan. The unique feature of this plan is that you will l receive the advantages of this policy until you reach 100 years of age!!

The company claims it to be a Sanchay (means save and grow) Plan with advantages.

In this article let’s discuss whether it’s good or bad for your future well-being., we will do a detailed analysis of its ‘Sanchay’ aspect and have a look at any disadvantages on their claimed ‘advantage’!

In this HDFC Life S anchay P ar A dvantage review, we will first analyse the HDFC Life Sanchay Par Advantage Pros (advantages) and Cons (disadvantages).

Then we will move to calculating the potential returns to get better insights.

This critical research study will guide you in making wise investment decisions.

Let’s read on and figure out what this plan has for you in its basket!!

Table of Contents:

What are the Key Features of HDFC Life Sanchay Par Advantage Plan?

HDFC Sanchay Par Advantage: Immediate Income option

HDFC Sanchay Par Advantage: Deferred Income option

HDFC Life Sanchay Par Advantage: Analysis and Review

‘Disadvantage’ of HDFC Life Sanchay Par Advantage

HDFC Life Sanchay Par Advantage: How to cancel this plan?

Common Mistakes to Avoid When Buying HDFC Life Sanchay Par Advantage

Final Verdict on HDFC Life Sanchay Par Advantage Plan

What are the Key Features of HDFC Life Sanchay Par Advantage Plan?

Below are the key features and Basic Eligibility Criteria of this plan:

HDFC Life Sanchay Par Advantage policy comes with 2 plan options:

(i) Immediate Income Option; and

(ii) Deferred Income Option

- Life cover protection till the age of 100 years,

- Basic eligibility criteria are shown in the below table:

| Eligibility Criteria | Minimum | Maximum |

| Age at Entry (years) | 0 years(30 days)ꜛ |

|

| Age at Maturity(years) | 100 years Maximum | |

| Premium Payment Term Years |

|

|

| Policy Term(years) |

|

|

| Minimum Sum Assured on Maturity(₹) | ₹3,00,000 | |

| Maximum Sum Assured on Maturity(₹) | No limit, subject to Board Approved Underwriting Policy (BAUP) | |

- The policy term will be 100 minus the age of entry. Let us say, you are 30 years old, then your policy term will be 100-30=70 years!

- The Minimum Death Benefit shall be 105% of the Total Premiums Paid as of date of the death.

- The minimum premium per installment is Rs.25,000; you can choose to pay it annually, half-yearly, quarterly, or monthly as shown below.

| Frequency | Minimum Premium Per Instalment |

| Annual | ₹ 25,000 |

| Half-Yearly | ₹ 12,750 |

| Quarterly | ₹ 6,500 |

| Monthly | ₹ 2,188 |

If you’re exploring whether the HDFC Life Sanchay Par Advantage review indicates it is suitable for long-term investing, it becomes important to analyse its IRR, bonus structure, and policy flexibility before making a decision.

Many investors compare HDFC Sanchay Par Advantage plan details with other traditional plans to understand how its income options, bonus pay-outs, and policy tenure align with their financial goals.

Let’s have a look at this brief video description reviewing all the major aspects of the HDFC Life Sanchay par advantage plan and whether it’s good or bad.

Before relying on the HDFC Life Sanchay Par Advantage brochure PDF, investors should carefully compare actual pay-out structures with their long-term financial requirements.

For details continue reading this article.

Now, let us discuss the 2 options provided by this HDFC Sanchay Par A dvantage policy.

We will start with an Immediate Income option.

HDFC Sanchay Par Advantage: Immediate Income Option

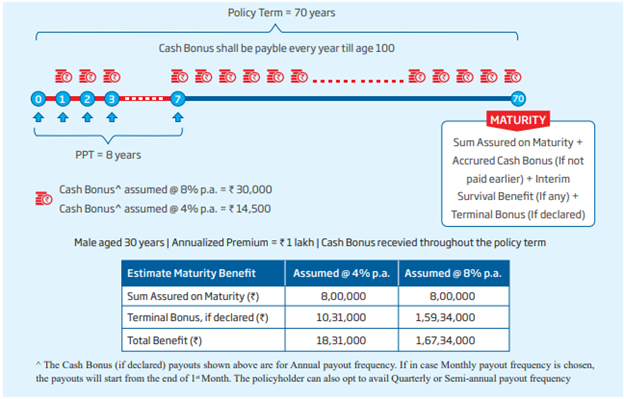

Let us say you are 30 years old, and choose to pay an annualized premium of Rs. 1 Lakh for the premium payment term (PPT) of 8 years.

As the policy option name suggests, HDFC Sanchay Par Advantage will start paying cash bonuses immediately upon completion of the first premium payment. And it will continue to pay the cash bonuses upon completion of each policy year.

The policy Term will be 70 years. That is, you will receive Cash Bonuses throughout the policy term of 70 years. The amount of cash bonuses varies based on the company’s performance history in the given year.

You can get the Cash Bonus at a different rate of returns, as shown below:

| Assumed Rate of Return | Cash Bonus |

| 8% | Rs. 13,000 |

| 4% | Rs. 14,500 |

The HDFC Life Sanchay Par Advantage immediate income plan attracts investors looking for early cash flows, but the long-term sustainability of returns depends on bonus declarations rather than guaranteed pay-outs.

Please note that the Cash Bonuses are NOT the guaranteed bonuses!

The below image shows the description (Image Source: Product Brochure)

As you can notice from the above description in the image:

- The assured sum will be Rs. 8 Lakh s.

- And, there will be a terminal bonus of

- Rs. 10,31,000 at a 4% assumed rate of return, or

- Rs. 1,59,34,000 at an 8% assumed rate of return.

Note that terminal bonuses are not guaranteed as well.

But if we take the best-case scenario of an 8% assumed rate of return, you will receive

- Rs. 30,000 per annum throughout the policy term, and

- The non-guaranteed terminal bonus of Rs. 1,59,34,000 at maturity.

We will do a detailed illustration and analysis of this best-case scenario to see what all the advantages ‘HDFC Life Sanchay Par Advantage Plan’ can provide!!

Before we get into illustration, let’s have a look at the other option of this plan, which is a deferred income option.

The HDFC Life Sanchay Par Advantage immediate income plan may appear attractive for those seeking regular pay-outs, but investors must understand that a major portion of the income depends on non-guaranteed cash bonus declarations.

HDFC Sanchay par Advantage: Deferred Income Option

Let us take the same example as given in the previous option.

Let us say you are 30 years old, and choose to pay an annualized premium of Rs. 1 Lac for the premium payment term (PPT) of 8 years.

In this option, you will receive a guaranteed income along with Cash Bonuses, once you finish your premium paying term.

You have to pay your premium payments for the 8th year, then you will start receiving the guaranteed income from next year onwards till 25 years along with non-guaranteed bonuses, as described below:

For 25 Years, you will receive:

- the guaranteed income of Rs. 28,400.

- Cash Bonus of Rs. 42,600 p.a. (assumed at 8% returns), or Cash bonus of Rs. 1,100 p.a. (assumed at 4% returns). [Cash bonuses are not guaranteed.]

After the 25 years’ duration,

You will only receive non-guaranteed Cash Bonuses as shown in this table:

| Assumed Rate of Return | Cash Bonus |

| 8% | Rs. 71,000 |

| 4% | Rs. 2,500 |

If declared, then you may receive this bonus amount throughout the policy term of 70 years.

Apart from guaranteed income and non-guaranteed bonuses, this option will also provide the non-guaranteed terminal bonuses, at maturity as shown in this table:

| Assumed Rate of Return | Cash Bonus |

| 8% | Rs. 53,60,000 |

| 4% | Rs. 15,22,000 |

Calculation of Guaranteed Income:

There is a process of declaring the amount of Guaranteed Income. You are getting the guaranteed income of Rs. 28,400 for 25 years because your premium payment term is 8 years and you are 30 years old.

When evaluating the HDFC Life Sanchay Par Advantage deferred income option, understanding the balance between guaranteed income and non-guaranteed cash bonuses is critical for realistic expectations.

For different entry ages and for different Premium Payment Terms, Guaranteed Income is calculated as shown in the table below:

| Guaranteed Income Rate (As a % of Annualized premium) | |||

| Age at Entry | Premium Payment Term (PPT) | ||

| 8 | 10 | 12 | |

| Up to 25 years | 28% | 40% | 50.8% |

| 26 to 35 years | 28% | 40% | 50% |

| 36 to 40 years | 28% | 40% | 50% |

| 41 to 45 years | 28% | 40% | 50% |

| 46 to 50 years | 28% | 40% | 50% |

| 51 to 55 years | 27.6% | 40% | 50% |

| 56 years and above | NA | 40% | 50% |

We have calculated the Guaranteed Income Rate (as a % of annualized

premium) in the above table.

Now, we will calculate the average returns provided by both options of this policy.

We will consider the same examples with the best-case scenario… that is at an assumed rate of return of 8%.

The Assured Death Benefits in the above example for both options will be Rs.12,50,000 in both options.

For more details on death benefits, you can refer to the HDFC Life Sanchay Par Advantage Product Brochure.

Our core objective in this post is to make you aware of the investment aspect of this plan.

When reviewing HDFC Life Sanchay Par Advantage plan details, many investors assume the deferred income option offers fully guaranteed returns, whereas only a portion of the income is fixed and the remaining benefits depend on future bonus declarations.

Whether you should invest or avoid this plan!

Let’s do a real analysis of both options in the next section.

HDFC Life Sanchay Par Advantage: Analysis and Review

This HDFC Life Sanchay Par Advantage review will guide you in making informed investment decisions to help reach your financial goals smarter and faster.

A detailed HDFC Life Sanchay Par Advantage IRR analysis helps uncover the actual earning potential of the plan beyond the projected illustrations shown in the brochure.

From the above description, it may seem like this policy has truly covered the lifetime until you become 100 years old; by providing regular income throughout 70 years. But if you notice it closely you will find that:

1. In the deferred income option,

For calculating, we are taking the best- case scenario at an 8% assumed rate of returns, as shown in this table:

| Policy Duration | Guaranteed Income | Cash Bonuses(non- guaranteed) |

| During 25 years | Rs 28,400 | Rs 42,600 |

| After 25 years of Maturity | Nil | 71,000 |

Using the above data, we calculated the IRR to be around 4.8%!!

Please note, that this IRR is for the best-case scenario of an 8% assumed rate of returns. It is better not to consider the worst-case or even the average- case scenario for this option!!

This HDFC Sanchay Par Advantage review clearly indicates the lack of potency of HDFC Sanchay Par Advantage plan in generating substantial returns for the investors in the long run.

Even saving bank FD accounts can give you better returns at this amount.

Moreover, it involves only minimal risk and is considered a safe investment vehicle compared to other market-linked products.

4% return rate in 70 long years!! Don’t you think that there are better options available to you, if only you care to explore a bit further you will find better investment opportunities aligning with your investment objective.

HDFC Sanchay Par Advantage review also highlights the fact that knowing the potential return plays a key role in choosing an investment vehicle.

We will review alternative options in the later section.

Now, let’s have a look at the immediate income option.

2. In the immediate income option, the best-case scenario is that you are receiving a cash bonus of Rs. 30,000 per annum (at 8% rate of interest) until you are 100 years old!

The below table (shortened version) shows the overall duration of 70 years, from the year 2020 till 2090, here we will calculate the average returns of your investment in this policy.

| Year | Premium Payment | Cash Bonus(at 8% assumed rate) |

| 2020 | -1,04,501 | |

| 2021 | -1,02,251 | 30,000 |

| 2022 | -1,02,251 | 30,000 |

| 2023 | -1,02,251 | 30,000 |

| 2024 | -1,02,251 | 30,000 |

| 2025 | -1,02,251 | 30,000 |

| 2026 | -1,02,251 | 30,000 |

| 2027 | -1,02,251 | 30,000 |

| 2028 | 30,000 | |

| 2029 | 30,000 | |

| 2030 | 30,000 | |

| 2040 | 30,000 | |

| 2050 | 30,000 | |

| 2060 | 30,000 | |

| 2070 | 30,000 | |

| 2080 | 30,000 | |

| 2090 | 1,59,34,000(on maturity | |

| IRR | 5% | |

The immediate income option provides you with an IRR of 5% as their best cash bonuses are assumed at 8%.

Along with all premium payments you have to pay the GST charges.

Do you think it is a great deal for your financial future?

With both of these variants, you are getting returns in the range of approximately 5%!

Being a Market-Linked scheme that too with a longer time horizon the returns generated from this HDFC Sanchay Par Advantage plan are not that satisfactory.

Those looking at HDFC Life Sanchay Par Advantage returns should evaluate post-tax returns and inflation-adjusted returns rather than focusing only on maturity illustrations.

Based on multiple scenarios, the IRR of Sanchay Par Advantage typically remains in the lower range, raising concerns for investors seeking inflation-beating returns.

The worst part is that the returns doesn’t even come par with Debt Instrument Returns or Bank FD Returns for that matter.

So having a clear vision of future financial goals helps you stay away from choosing investment products like HDFC Life Sanchay Par Advantage Plan. Be it any investment vehicle or investment product, only when its returns surpass the inflation rate it becomes more beneficial to an investor.

HDFC Life Sanchay Par Advantage Vs Other Plans

HDFC Life Sanchay Par Advantage Plan vs HDFC Life Sanchay Plus.

“Sanchay Par” gives Guaranteed Income during the income term that increases every year whereas “Sanchay Plus” is for Steady retirement income with Life Long Income Option.

The HDFC Sanchay Plus review often becomes relevant because investors compare HDFC Life Sanchay Plus vs HDFC Life Sanchay Par Advantage to understand whether guaranteed income or participating bonuses offer better predictability.

Please read our review of HDFC Life Sanchay Plus.

‘HDFC Life Sanchay par Advantage Plan’ vs ‘LIC Jeevan Umang’.

In LIC Jeevan Umang, a 100% yearly premium will be paid every year till the demise of the life assured which is guaranteed 8% on the sum assured.

After the demise of the policyholder entire sum assured along with bonus and additional bonus will be given to the nominee.

Click here to read our LIC Jeevan Umang review.

‘HDFC Life Sanchay Par Advantage Plan’ vs PPF

Let’s assume, that instead of buying this HDFC Sanchay Par Advantage policy, you choose to invest in the Public Provident Fund (PPF) and buy a term insurance plan for life cover.

This investment in PPF to meet your financial goals.

The term insurance plan will give you the same insurance coverage that you will get under your ‘HDFC Life Sanchay Par Advantage’ but at a much lesser premium charge.

The PPF account is a long-term, low-risk investment and the interest earned on these investments is tax-free.

‘HDFC Life Sanchay Par Advantage’ vs ELSS

ELSS Mutual Fund is, once again, solely an investment vehicle. It does not offer life cover like ‘HDFC Life Sanchay Par Advantage’.

However, you can buy a term insurance plan for the same life cover.

You can also keep invested for any number of years and your principal amount will get compounded. You can also choose to invest through SIPs if you don’t want to pay the lump-sum payment.

‘HDFC Life Sanchay Par Advantage’ vs ‘HDFC Life Sanchay Fixed Maturity Plan’

“HDFC Life Sanchay Fixed Maturity Plan”, is a life insurance plan that promises to provide guaranteed returns in the form of a lump sum benefit to help you attain your milestones.

When comparing HDFC Life Sanchay Par Advantage vs HDFC Life Sanchay Fixed Maturity Plan, investors should clearly understand the difference between guaranteed maturity benefits and non-guaranteed bonus-linked returns.

Click here to read more about “HDFC Life Sanchay Fixed Maturity Plan”

Insights on HDFC Life Sanchay Par Advantage and other Insurance Plans:

After a thorough review of all the different alternative plans for ‘HDFC Life Sanchay Par Advantage’, We can conclude that ELSS and PPF along with term insurance seem to be better options both in terms of liquidity and returns as well.

So what you should do if you want greater returns for a long term of 60-70 years?

Well, if you are looking for long- term investment then you must consider investing in Equity Mutual Funds. There you will get long- term returns in the range of 12% to 15% and you will experience the power of compounding in your invested capital. Let’s do an analysis to find out

You choose to invest Rs. 8 Lacs as a Lumpsum payment into an equity Mutual Fund, within 25 years the future value of your investment will be Rs. 1,58,30,773, at the assumed rate of return of 12%! Have you noticed it? Just Rs.8 Lacs can make you 1.5 crores within the 25-year duration.

You can keep invested for any number of years and your principal amount will get compounded. You can also choose to invest through SIPs if you don’t want to pay the lump-sum payment.

You can use this Online Mutual Fund Calculator to find the future value of your desired investment value and investment duration, by assuming the returns in the range of 12% to 15%.

If you are risk-averse then, instead of investing in this policy, you can deposit Rs.1,00,000 per annum for any number of years you want into the PPF account or FD Scheme. Here, you will get the assured returns in the range of 7% to 8%. That will make you Rs.1.3 crores in 35 years with Rs.8 Lacs invested capital!

‘Disadvantage’ of HDFC Life Sanchay Par Advantage

In the Immediate income option, you are getting a nominal amount of Rs. 14,500 per annum.

In the Deferred Income option, you are receiving merely Rs. 2,500 per annum for 70 years long term!

This clearly raises concerns when evaluating the HDFC Life Sanchay Par Advantage disadvantages, particularly in terms of low income pay-outs and long lock-in periods.

It is like, your friend asks you for Rs.8 Lacs and promises to pay back any random small amount every single year till you attain the age of 100 years!! Will you lend money to your friend with such a vague promise?

Of course NOT!

In the best-case scenario, this policy promises you to pay Rs. 1.5 crores at maturity. That is, if you start investing from the year 2020, you will get Rs.1.5 crores (non-guaranteed) in the year 2090!! Still, the average return rate will be merely 5%, which can’t even beat the rate of inflation, which is growing rapidly!

Even after considering bonuses, the HDFC Life Sanchay Par Advantage returns struggle to match inflation-adjusted expectations over long durations.

Talking about the HDFC Life Sanchay Par Advantage maturity bonus which is calculated at Rs.1.5 crores, which you may get from this policy in 70 long years!! But as you have seen the analysis discussed in the previous section:

- With Mutual funds, you will generate Rs.1.5 crores within 25 years of investment duration.

- PPF will generate Rs.1.5 crores in 37 years, and these are guaranteed returns!

I hope now you have understood that though they claim it to be an “Advantage” Plan, actually it is a “Disadvantage” Plan.

A financial advisor would have calculated whether this policy is good or bad after a detailed review. But still, have you ever thought as to why your Financial Advisor is still trying to sell you this product?

If your Financial Advisor recommends or convinces you to buy it, BEWARE! it’s because they may get a commission of 30-40%. If your premium is 90,000, your advisor may get around 27,000 to 36,000 as commission out of your premium.

So it is for the commission they are selling you and not for your interest or because it meets your financial goals. Also, be careful of agents who try to impose this on you for their High – Agent C ommission.

So always check about the product, its review, returns, if it beats inflation, and especially if it meets your financial needs. If not, then do not opt for it just because your advisor tells you to do so.

If your Bank Relationship Manager also tries selling you this product, NOT TO WONDER, the bank also gets a commission. Relationship managers have pressure to sell these kinds of products and also have targets, hence there is a lot of misselling happening.

They missell saying that there is around 8 to 9% returns from these products. (Nowadays the complaints about bank misselling have increased) Hence before you buy a product verify the truth on the HDFC Life website as to what the actual returns are.

There is a lot of marketing and advertisements to attract customers but if you are not an ignorant customer, you wouldn’t fall prey to these kinds of products.

Many are behind complicated products thinking that it must be good, but it is not so. PPF, Mutual Funds, and Term Insurance though are old and boring and have no marketing gimmicks in them.

They are simple and easy to understand and also fulfils their purpose. Complexity kills transparency. Less transparency makes it easier to mis-sell.

One more place where it becomes easier to missell is when the investors have no much knowledge of these products, they often tend to believe whatever is said to them. So never be an ignorant investor.

Buy a product only if you can understand it. Avoid complicated investment products like HDFC Life Sanchay Par Advantage.

Tax Benefit – all the paid premiums and the benefits received under the HDFC Life Sanchay Par Advantage Plan is eligible for tax exemption which comes under, section 80C of the Income Tax Act, 1961.

Even after reviewing HDFC Life Sanchay Par Advantage bonus history, investors should remember that past bonus declarations do not guarantee similar future returns.

How much is really guaranteed in HDFC Life Sanchay Par Advantage?

Returns are guaranteed only if you complete the payment: If you miss to pay the premium or surrender the policy, the policy benefits will be reduced`.

They portray the guaranteed part, but how much is guaranteed?

Check your final returns, it’s only 4 to 5%.

Understanding the HDFC Life Sanchay Par Advantage policy details is crucial to identify what portion of returns is truly guaranteed versus bonus-dependent.

GST: You will also have to pay the GST on the premium, after that the returns will become even lower.

Liquidity: Investment will be locked until the income period starts.

The usual lock-in period of ULIP policies is 5 years.

If you are looking for wealth creation, then this is not the right product: PPF would give higher returns.

How will this plan even benefit you?

Do you still think this is a good plan?

YES, If you feel that 4% is enough to meet your financial goals, and does it current beats inflation rate?

Definitely Not Right!

YES, you can still invest, only i f you feel that no other investment can give you 4% returns or more.

If your answer was NO, then don’t opt for it. If you have already purchased it, here is a way to cancel it.

HDFC Life Sanchay Par Advantage: How to cancel this plan?

If you have signed up for this policy without Reviewing the complete details of this policy or you signed up because your bank relationship manager pushed it to you, there is a way out. You can come out of this policy.

There will be a free look period of 15 and 30 days as defined below

If you have taken this plan directly from the company, then you have the option to return the policy by stating the reason within 15 days from the date of receipt of the policy.

Whereas, if you have taken this policy through some other medium such as online, or telephone, which does not involve face- to- face interaction, then you will have a free look-in period of 30 days.

Upon receipt of your letter along with the original policy document, you will get the refund of your paid premium, but it will be subject to a deduction of the proportionate risk premium for the period on cover, the expenses incurred by the company for stamp duty and medical examination if any.

There are no cancellation charges for ULIP policies after completing five years.

Many policyholders specifically look for the HDFC Life Sanchay Par Advantage surrender value calculator to estimate how much they may receive upon early exit, but surrender values vary based on policy year and premium payment term.

As this is not a ULIP plan, i n case if you want to cancel this policy during your policy term, then the deductions will be as shown in the below table:

(Surrender value is calculated based on deductions.):

| Policy Year | Premium Paying Term | |||

| 6 years | 8 years | 10 years | 12 years | |

| 0 | 0% | 0% | 0% | 0% |

| 1 | 0% | 0% | 0% | 0% |

| 2 | 30% | 30% | 30% | 30% |

| 3 | 35% | 35% | 35% | 35% |

| 4 | 50% | 50% | 50% | 50% |

| 5 | 50% | 50% | 50% | 50% |

| 6 | 60% | 50% | 50% | 50% |

| 7 | 65% | 50% | 50% | 50% |

| 8 | 75% | 60% | 65% | 58% |

| 9 | 80% | 65% | 70% | 65% |

| 10 | 80% | 75% | 75% | 73% |

| 11 | 80% | 80% | 80% | 80% |

| 12+ | 90% | 90% | 90% | 90% |

So, what is the surrender value of ‘HDFC Life Sanchay Par Advantage’?

Surrender value is based on your Premium Paying Term and Policy year when you want to cancel, the surrender value factors as a percentage of your premium paid will be calculated, as shown in the table.

For example, if you want to cancel your policy in the 4th policy year, & your PPT is 8 years; then you will receive 50% of the premium that you paid to the company.

For more details, you can visit hdfclife.com

Also, you can call their Toll free number (from 9 am till 9 pm, all days): 1800-266-7227

Common Mistakes to Avoid When Buying HDFC Life Sanchay Par Advantage

One of the biggest mistakes investors make while choosing the HDFC Life Sanchay Par Advantage plan is assuming that the illustrated returns are guaranteed.

In reality, a significant portion of the benefits depends on future bonus declarations, which are non-guaranteed and can vary over time.

Another common mistake is focusing only on the regular income component without evaluating the overall return (IRR).

While the idea of lifelong income sounds attractive, the actual returns often fall in the range of 4%–5%, which may not be sufficient to beat inflation over long periods.

Many investors also overlook the long policy term and liquidity constraints.

With commitments extending up to 70 years or even age 100, the money remains locked in for decades, limiting financial flexibility and access to funds during emergencies or changing life goals.

Relying solely on agent recommendations or promotional illustrations is another critical error.

These plans are often sold highlighting best-case scenarios, without clearly explaining the risks, costs, and realistic return expectations.

Lastly, combining insurance and investment in a single product can dilute the effectiveness of both.

Instead of opting for bundled plans like HDFC Life Sanchay Par Advantage, separating insurance (via term plans) and investments (via mutual funds or PPF) can lead to better protection, higher returns, and improved financial control.

Common Complaints About HDFC Life Sanchay Par Advantage Plan

A common issue buyers face is the gap between sales promises and actual returns.

Many investors are attracted by projected maturity values and lifetime income claims, only to later realise that a large portion depends on non-guaranteed cash bonuses and terminal bonuses.

Another major complaint is the low IRR, which often falls in the 4%–5% range in many scenarios—making it difficult to beat inflation over long periods.

Liquidity concerns are also frequent.

Investors looking into HDFC Life Sanchay Par Advantage surrender value often realise that exiting early can significantly reduce returns.

Many buyers also complain about mis-selling, where agents highlight high projected returns but fail to explain lock-in periods, bonus uncertainty, and overall product limitations.

Final Verdict on HDFC Life Sanchay Par Advantage Plan

HDFC L ife Sanchay Par Advantage good or bad?

In short, you should AVOID investing in HDFC Life Sanchay Par Advantage.

Though they claim it to be a “Sanchay” Policy with “Advantage”; it is a “Vyaya” policy with “disadvantage”, as you might have noticed in the analysis and illustration given above!!

Also, they claim to pay Cash Bonuses for 70 long years but all these bonuses are not guaranteed!

In the best-case scenario, this HDFC Life Sanchay Par Advantage Plan policy offers returns in the range of 4%-5%, which can’t even beat the rate of inflation.

Even the returns provided by your Saving Banks are better than this policy, as they are assured!

Therefore, as an alternative, you must invest in equity Mutual Funds, as you are planning to invest for the long term.

If you’re wondering is HDFC Life Sanchay Par Advantage good or bad, the answer depends on your priorities—income stability vs wealth creation—but the plan may fall short for aggressive long-term growth.

Overall, the HDFC Life Sanchay Par Advantage plan review highlights that while it offers structured pay-outs, its return potential may not justify the long lock-in period.

A final HDFC Life Sanchay Par Advantage review suggests that investors seeking higher growth and flexibility should consider alternative investment strategies.

Before investing, reviewing the HDFC Life Sanchay Par Advantage brochure and analysing real-life scenarios can help avoid mismatched expectations and improve financial decision-making.

For investors focused on wealth accumulation, HDFC Life Sanchay Par Advantage may not outperform simpler alternatives like term insurance + mutual funds, PPF, or even fixed-income instruments.

For better clarity on Mutual Fund investment, you must read this Comprehensive and Complete Guide to Mutual Funds.

Please don’t conclude your review of the ‘HDFC Life Sanchay Par Advantage Plan’ just by surfing through social media sites like Quora, Twitter, Facebook, etc. It is always wise to take the help of a professional financial planner.

You can also check out the review of HDFC Life Sanchay plus.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

I have forgotten to remind you.

Also what as a result?

In the table under the heading. 2. In the immediate income option, the terminal bonus of Rs 1,59,34,000 is added but SA of 8,00,000 is also paid out. Shouldn’t this also be added while calculating IRR?

It was a nice presentation. I was about to opt for the same. I was not sure as i m not finance person. Its a eye opener. Instead i will invest in Mutual Fund HDFC Top 100

I am glad that it helped you

I used to be recommended this blog by way of my cousin. I’m now not certain whether

or not this submit is written through him as nobody else understand such

distinct about my problem. You are incredible! Thanks!

Thanks on your marvelous posting! I actually enjoyed reading it, you’re a great author.

I will always bookmark your blog and definitely will come back down the road.

I want to encourage one to continue your great job, have a

nice afternoon!

Hii, I have taken this policy today for 6 years by investing 1 lakh every year. They say me that every year I will get 25,000 as cash bonus. And after 6 years if I surrender then I will get 6 lakh 10 thousands. But did they minus my cash bonus from these amount and give me 3,90,000 as my guarantee return instead of 6,10,000 rs.

Excellent explanation. It was very useful to make a wise decision. Thank you and look forward to many more

Respected Sir,

Very nice and easy to understand illustrations. Sir I have already invested 1st premium ₹ 1.5L , II don’t want to continue and stop paying further premiums. How much amount I will get after stopping now

Please check the Guaranteed Surrender Value in the article.

Thanks for the Post. I thought of investing. However I made lot of research in the internet and found your blog. Absolutely good post with clear explanation.

Really appreciate.

Hi.Sanjay par advantage insurance how to terminate this poly for second year because the insurance fully cheated so many fake promises 10.03.2021.this time will I did not received my insurance policy original bond

We have posted a detailed video on how to surrender your HDFC life insurance plans. You can watch it here.

https://youtu.be/K8rFZLwHjcc

Hi,

In the immediate income plan, my understanding as below

I pay a premium of Rs 2 Lakhs/ year for 8 years

I get Rs 64K starting from the 2nd year

After completion of the last premium, i.e. in the 9th year, i would get

Rs 16 Lakhs(sum assured) + 2% of sum assured for every year i.e. 32K * 8 = 2.56 lakhs

My final pay out in the 9th year is 16 lakhs + 2.56 = 18.56 lakhs

this, assuming the bonus i am getting is only 2%, if it is more than that then the final pay out can increase significantly

I dont have to stay invested for 70 years as you have mentioned above

Could you please help me understand if i am right?

If you have surrendered your policy on the 9th policy term, then you will receive all the benefits you have mentioned. However, the cash bonus rates, if any, will be declared at the end of the valuation period.

Hi,

My Bank Manager asking me to pay 1lack per year for 10 years and i will get 37K per year guaranteed cash bonus for 30 years and the final amount at end of policy will approx 15Lack.

Kindly suggest on this🙏🏻

It is advisable to work out the outcome and proceed with the better option.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Hi , thank you for this post. However, I have already made the mistake of taking it as I believed the insurance agent (entirely my fault) and thought what he was saying was the truth. I have already paid 52250 one year premium with tax.

Now they are calling me 5 times a day to pay the 2nd year premium. If I dont pay, I lose all of my investment. The lock in period is 2 years, after that if I surrender, I will get assured 30000 only(from my 1 Lakh investment).

So my question is should I stop paying now and consider 50 thousands to be the payment for my foolishness or should I continue?

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the time, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

hi.

thank u for the analysis. Actually when i calculated the IRR it came to around 5-6% again and as I was told it is tax free it considered a 8-9% net return decent.

But my Qs is this

– I was told that my PPT is 6 years with deferred income option, so if i withdraw in 8th year i will get 100% premium paid + cash bonus incurred every year * 5% (interest every year)

Do you think it’s a lie ?

Hi

To answer your 1st question, PPF returns are also tax-free. The post-tax returns from Mutual Fund ELSS will be higher.

To answer your 2nd question, please check your PPT. The minimum PPT starts at 7 years. And yes you will receive the same but the 5% is not a guaranteed return.

Considering the insurance aspect which no mutual fund gives, par advantage is worthy on the aspect of diversification. Considering one pays 50k for year 1 and dies next year, which can’t be judged by IRR

Jyoti, That’s why we always suggest a combination of Term Insurance + PPF or ELSS. In this combo, you get the insurance cover and the investment value.

Hi, they told me that 7.1% return is guaranteed. Apart from that they will give cash bonus of 80,000 every year( when I will invest 2L per annum, if 1L per annum then 40,000 per year).

Did he completely lied to me?

Hi,

There are two types of options available in this policy.

Option:1 Immediate Income Option. In this option, you will receive a cash bonus (non-guaranteed) from your 2nd PPT onwards. And you will receive a terminal bonus at the end of maturity.

Option: 2 Deferred Income Option. In this option, once your PPT end, you will get a sum of guaranteed return for 25 years plus a non-guaranteed cash bonus. After that, you will receive only a cash bonus. And you will get the terminal bonus when the policy matures.

From your description, I think it is a Deferred Income Option.

However, 7.1% which was told to you is on the higher side. Please ask them to share the workings and check.

Thanks for this in-depth analysis! I was intrigued by the promises and could not believe them.

Glad to know that we can help you by providing some useful information.

I already purchased this policy last year

Now I want to know if I continue paying the premium for 6 years or I cancel the policy, if I pay the premium for 6 years can I surrender after 6 years how much amount I get

Since you have already taken this insurance plan, then you have two options.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the time, option 1 is better.

Also, if you have decided to surrender the policy after 6 years, then you will get 60% of the premium you have paid.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Hello, thank you for this post. However, I have already made the mistake of taking it as I believed the insurance agent (entirely my fault) and thought what he was saying was the truth. I have already paid 1 year premium on 1Lakh + 4500 tax.

Now they are calling me 5 times a day to pay the 2nd year premium. If I dont pay, I lose all of my investment. The lock in period is 2 years, after that if I surrender, I will get assured 60,000 only(from my 2 Lakh investment).

So my question is should I stop paying now and consider 1 Lakh to be the payment for my foolishness or should I continue?

Hi Raj,

It is advisable to work out the outcome of both the options and proceed with the better option.

If you want, you can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

you should be continue as i have invested in mutual fund and i thought in the same way which describe in this article but my money is now 0. At least you will get some amount in worst scenario.

Sorry to hear this. Mutual Fund will need time to get a better return. You will not get a 12% assumed rate of return in a short period. And, compared to the worst-case scenario, you can get a better return in your savings bank, Bank Fds, RBI Bonds, PPF, and other government schemes, if you don’t want to take any investment risk.

Thanks for such details. I was looking it as bank personnel suggested me this policy. But whenever I asked them IRR they bypass me. I was about to calculate that but find that in your post. Thank you.

Insurance is there that’s why 5% irr is overlooked

Hi!

We have taken the same investment contribution and split it between investment and insurance to see which performs better.

So, the Insurance cover and returns are not overlooked.

You are welcome.

You said that one cam gey better return in FD and PPF. Do you think that interest rate would by 7-8% after 50 yrs from now. Because internet rates are falling continuously.

“Hi Ashok Singh,

As you said there is no guarantee that FD and PPF interest rate be the same after 50 yrs.

But Mutual Fund investment can give you better return for long-term investment. It is better to compare various investment schemes before investing.”

This is so so helpful. Thanks a lot for illustrating this. My RM just tried to sell this, I am so glad I read this. Going to bash this guy now for selling lies

Hello sir, My advisor saying If u take policy of 30k per year, the next year onwards itself you will get 11,400/- not after 8yrs as you said. Please clarify

“Hi Muzammill,

Thank you for notifying us. Actually there are two options available in HDFC Life Sanchay Par Advantage.

Option: 1 Immediate Income Option and

Option: 2 Deferred Income Option

In option-1, you can get cash bonus from the 1st premium term onwards. But on the other hand, in option-2,you can get cash bonus once you finish your premium paying terms.

So, please clarify the options from your advisor before making a decision. “

Hello

Hats off, You are a libra. Your in depth analysis has helped many people. Its a worth reading. Thank you

You are welcome.

What if I exit this plan on 13th year, as their of 1L/ year illustration and 4.8L as money back every year and 8% of guaranteed bonus + Terminal Bonus. 17L altogether?

Hi Dinesh,

If you are completed your PPT, then you will receive 90% of the premium you have paid once you surrender the policy.

Thank you for detailed analysis. Can you please suggest any good similar plans with higher returns other than MF/SIP. I am inclined to buy one such policy. Please advice.

“Hi,

For personalized advice, you can schedule a free financial plan consultation with our Certified Financial Planners.

Please click link and register for our 30-minute Complimentary Financial Plan Consultation to get your appointment.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/“

HDFC LIFE Sanchay Par Advantage is a mistake. Please do not take it based on the advice of an agent, especially your Bank manager or relationship manager. In my case, they did not send the policy kit like for other insurance policies. They claim they send an ecopy of the proposal form which I never received. So I could not revoke during the freelook period. Their service is hopeless. Please be careful.

Thank you for sharing your Experience, Sapna Pillai. Please be cautious before choosing investment plans.

In your case, you can also escalate to the insurance ombudsman for a resolution.

i just got a call from my RM to convince on the same. I have kept on the hold saying will get back to you on this. good did not fall for it.

Good to know

Hi I am really confused and regretting now. Today itself I have got this plan but what they are saying is completely different. They asked me to pay one lac for each year and do not have to pay for 7th and 8th year. Also I can withdraw my money / surrender my policy anytime I want but they did not mention that they will deduct some amount. ??? Could you please guide me. what will be the final amount if I term the plan lets say in 3rd or 4th year and after let say 8 years? what will be the exact amount that I will be getting?

Hi,

Once you purchase a premium plan, either you can continue or surrender your insurance plan.

Based on your Premium Paying Term and Policy year when you want to cancel, the surrender value factors as a percentage of your premium paid will be change.

If you want to surrender your plan in the 3rd or 4th year, then you will get 35% to 50% of the premium you have paid.

After 8 years, you will get 60% to 80%

For more details, you can visit hdfclife.com

Hai sir, last year I took this policy…. the manager told me to pay 1 lakh rupees every year for 10 years and from the 12th year, he told that I would get around 80000 rupees per month and I took the policy and paid the first year premium and now I am thinking to stop this policy due to less monetary benefit!! Plz guide me whether to continue or stop this policy!!!!

Hi,

You can submit your cancellation or complaint request in an Online or Offline Format. A written request or an email with the registered email id is mandatory. You can send your e-mail to service@hdfclife.com.

For more details, you should read this current official document of HDFC Life Sanchay Par Advantage.

All grievances (Service and sales) received by the Company will be responded to within the prescribed regulatory Turn Around Time (TAT) of 14 days.

How to cancel this policy , I just purchased two days back

There is a free look period of 15 and 30 days to cancel the policy.

If you have taken this plan directly from the company then you have the option to return the policy by stating the reason within 15 days from the date of receipt of the policy.

Whereas, if you have taken this policy through some other medium such as online, telephone, which does not involve face to face interaction, then you will have a free look-in period of 30 days.

On receipt of your letter along with the original policy document, you will get the refund of your paid premium, but it will be subject to deduction of the proportionate risk premium for the period on cover, the expenses incurred by the company for stamp duty and medical examination if any.

i bought this policy on 25th march 2020 and want to surrender now on 6march 2021. is it good to surrender or i shall continue.

Hi,

It is better to work out the outcome of both the options and proceed with the better option.

If you want, you can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

But what about life coverage i.e. Death benifit?

Yes, this plan also covering life coverage. For more details on death benefits, you can refer to the HDFC Life Sanchay Par Advantage Product Brochure.

https://www.holisticinvestment.in/hdfc-life-super-income-plan-review-should-you-buy-or-not/

Immediate Income Option – as per your illustration cash bonus is paid out after the premium payment term of 8 years, but when I enquired in the bank, they are saying the cash bonus is paid out right after the year of inception i.e. if I pay premium this year 2021, I will get the bonus in 2022 and so on. can you please clarify this?

Hi,

In the Immediate Income Plan, you will receive the cash bonus from your 2nd premium payment term onwards. So, yes what the bank officials said is true.

I came across this policy name, but the scheme provided to me is different.

I need to pay premium of 1L pa for 6 years and I start getting 1840/- (monthly) from the 2nd month of investment [5578/- (quarterly) 11270/- (half year) or 23000/- (yearly)] continuously for 6 years (same amount). AND if I double the annual premium, the monthly amount too doubles with some interest added (3760/- monthly). THEN “on survival upto Maturity at the age of 100 years” ::

Sum Assured 6 lacs || Accrued terminal bonus 8329000|| Total Benefit Received 8929000.

Do you think is this some variation of above plan or a different plan altogether and it is beneficial?

This plan was advised to me via bluechipindia.co.in || are you aware of this company and can perhaps tell us if they are legit.

Hi!

The cash bonus rate is declared at the end of every financial year. So, the cash bonus may change… it is better to check the plan brochure.

can you give more clarity on the Immediate Income Option. Your illustration shows the cash bonus receipts only after the PPT of 8 years, but the bank manager says we will get the bonus right after from next year i.e. if I paid the premium this year 2021, I will get the cash bonus in 2022 for Rs.30,000. Can you clarify if this is the case?

Thank you for notifying us Abdul. As your Bank Manager said, you will get your cash bonus from the next year onwards.

Hi

I took this policy with a yearly premium of 1 Lac and for 6 years, opted for immediate income. Now after reading this i have realized i have made a big mistake.

My 1year will be completing in this Feb’21.

Shall I discontinue with this policy.

Hi Ishita Gupta,

It is advisable to work out the outcome before you decide. Because if you decided to surrender your insurance plan, then you might need to some amount will be deducted from the premium you have paid.

If you want, you can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

I have opted for 1 lakh per year for 6 year option and I was asked to make the first premium of 1 lakh. Subsequently, they have agreed to make it in 4 quarter i.e. 25000 x 4 + GST and they have issued the policy. I was not satisfied with the policy details. I have approached offices of HDFC Life Insurance as a customer looking for this policy and none of them could give any proper explanation about the quantum of returns and the surrender value. Their illustration shows 23500 cash bonus per annum. I was assured that besides the annual income, on 7th year I will get back the invested amount of Rs. 6 lakh but at one branch I was told that I will be getting only Rs.4.87 lakhs or so. It seems neither the brokers nor the company people are in a position to give any concrete explanation. The illustration shows cash bonus at 8% is non guaranteed and none of them could give any satisfactory explanation. Now I am planning to cancel the policy within 15 days. Your analytical approach seems to convincing. Thanks.

Glad to know that we can help you by providing some information.

You are welcome.

You are welcome

Yesterday I was fully convinced after meeting the bank guy…thank god i read you review today, A big NO to them.

Thanks a lot for the detailed explanation, i became more aware now.

Good to hear

i invested in this policy in december 2020 considering my RM suggestions and then realised that i have fallen prey. Is there any way i can save myself now?

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the times, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here!

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Hi,

My Father’s age is 65 and if he takes the policy, will it be advantages to take the hdfc life sanchay par advantage plan

The income received will be fixed and not inflation adjusted. It is advisable to work out the outcome and proceed with the better option.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Hello,

I have been misguided by banker and now its already 6 months since i have purchased this policy.

Can i do something to stop this policy?

Will i get refund of premium that i have already paid?

You can cancel the policy during the free look period of 15 and 30 days.

On receipt of your letter along with the original policy document, you will get the refund of your paid premium, but it will be subject to deduction of the proportionate risk premium for the period on cover, the expenses incurred by the company for stamp duty and medical examination if any.

Thank you for the review. Quite helpful. It might be a vague query but can you give some idea about what possibly can be the best Investment options seeing Market conditions today.

Hi,

For personalized advice, you can schedule a free financial plan consultation with our Certified Financial Planners.

Please click the link and register for our 30-minute Complimentary Financial Plan Consultation to get your appointment.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

So only you are the genuine one to say invest in mutual fund that you recommend, which will give Gauranteed return of 12% as mentioned in your review.

And people should believe this .

Where is the gaurantee in equity investment for 12%

You are just using this platform to demarket another brand and market your products .

Hi Kishore,

it’s our genuine review. We are not aiming to demarket any brand. It’s upto investors to choose their investment plans. As financial planners, we are just giving them suggestions to ease their work.

Thanks alot for the Info, Yesterday my VM called & recommended this, Now I understood the policy thoroughly

Gald to know that we can help you!

Have gone through the reviews and really confused. If I take this policy with 1 lakh premium per year for 6 years, I will be receiving monthly income of Rs. 900 + approximately whereas if it was in my daughter’s name the monthly payouts will be Rs. 1700 + approximately. Suppose if I am taking the policy in my daughter’s name and opt out after 6 years, I will be getting back the 6 + lakhs as the surrender value. Looking into the current FD rate, is it not worth to opt this scheme.

Thank you for sharing your point of view.

Then which one I’ll be the best option to invest

Hi,

For personalized advice, you can schedule a free financial plan consultation with our Certified Financial Planners.

Please click the link and register for our 30-minute Complimentary Financial Plan Consultation to get your appointment.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Really an eye opener for all the investors, preventing them losing hard earned money at the hands of there mis sellers. They are really mean even being known faces around you.

Glad to know, we can help you.

When the RM told me about this policy today, I couldn’t understand anything. So, I said I’ve to read the policy details and will get back. I tried to understand this policy, but couldn’t. I somehow landed on your website and tried to go through the policy details and am still lost. Maybe I’m not that investment savvy to understand such intricate things. The only thing I understood from the entire writeup is ‘Don’t Invest’ in this product and that’s enough for me. Thanks for the heads up.

Hi, if you need personalized advice to choose the right investment plan, then you can get advice from certified financial planners.

Or

You can schedule a free financial plan consultation with our Certified Financial Planners.

Please click the link and register for our 30-minute Complimentary Financial Plan Consultation to get your appointment.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Hi, if you need personalized advice to choose the right investment plan, then you can get advice from certified financial planners.

Or

You can schedule a free financial plan consultation with our Certified Financial Planners.

Please click link and register for our 30-minute Complimentary Financial Plan Consultation to get your appointment.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

You are welcome

I took this policy about a month back on 4th Nov 2020 , now I want to cancel. May I know the procedure to cancel this. Please help me on this. Thanks in advance.

There is a free look period of 15 and 30 days to cancel the policy.

After the free look period, you can submit your cancellation or complaint request in an Online or Offline Format.

A written request or an email with the registered email id is mandatory.

You can send your e-mail to service@hdfclife.com.

For more details, you should read this current official document of HDFC Life Sanchay Par Advantage.

All grievances (Service and sales) received by the Company will be responded to within the prescribed regulatory Turn Around Time (TAT) of 14 days.

On receipt of your letter along with the original policy document, you will get the refund of your paid premium, but it will be subject to deduction of the proportionate risk premium for the period on cover, the expenses incurred by the company for stamp duty and medical examination if any.

Hi,

I am 58 years old and wanted to have confirm income after retirement as I am working in private company and will not have enough pension. As you rightly pointed out, HDFC person sold this policy to me. I have applied for this policy on 4th Nov 2020 and paid a premium of Rs 10 lakh with GST Rs 45000/= but now after going through your review, I want to cancel this policy.

Kindly gudie me how to go about

Hi,

You can submit your cancellation or complaint request in an Online or Offline Format. A written request or an email with the registered email id is mandatory.

You can send your e-mail to service@hdfclife.com.

For more details, you should read this current official document of HDFC Life Sanchay Par Advantage.

All grievances (Service and sales) received by the Company will be responded to within the prescribed regulatory Turn Around Time (TAT) of 14 days.

Hi, should I opt this policy for short term say 6 years? As yesterday only I bought this plan.

Advisor told me to invest for 6 years (Rs 1 lakh per year upto 6 years) and enjoy the return of Rs 24k per year.

I was looking this for short term only. Will take out the money after completion of 7 years.

Kindly note- Have invested few amount if MF /Equity already.

It is best to avoid investing in HDFC Life Sanchay Par Advantage.

They claim to pay Cash Bonuses for 70 long years but all these bonuses are not guaranteed!

In the best-case scenario, this policy offers returns in the range of 4%-5%, which can’t even beat the rate of inflation. Even the returns provided by your PPF are better than this policy, as they are assured!

How you are getting the IRR @ 4.8% in the deferred plan? i am able to see 7.1% IRR till maturity in case if we consider 8% return. is there something i am missing?

Below details:

Age of entry:34,

PPT: 10 years,

Premium amt: Rs 5 lacs,

Guaranteed Survival benefit P.a. = Rs 2,06,000 from 12th to 36 years,

Non guaranteed Cash Bonus p.a. = Rs 3,09,000 from 12th to 36 years and

= Rs 5,15,000 from 37th to 66 years.

Guaranteed Maturity amount = Rs 50,00,000

Total Maturity Incl Terminal Bonus = Rs 1,81,45,000.

Hi, since you have already purchased the policy, then you can check the return in HDFC Life website by using your policy number.

I have already purchased this for 1.5 lakhs for 12 years, and it been 2 months now. I can’t quit as look in period is over (no one told me about the look in period until now). Is there any way i can escape from this?

Hi,

You can submit your cancellation or complaint request in an Online or Offline Format. A written request or an email with the registered email id is mandatory.

You can send your e-mail to service@hdfclife.com.

For more details, you should read this current official document of HDFC Life Sanchay Par Advantage.

All grievances (Service and sales) received by the Company will be responded to within the prescribed regulatory Turn Around Time (TAT) of 14 days.

I can surrender the term at any point of time after PPT. Let’s say my term is 8 and paying around 60K and surrendering after 10 years. As said I will be getting cash bonus of 18K every year and surrender amount is around 5.3L so total is 7.1L. It is still good right. Or am I wrong ?

If you are paying 60k per annum for 8 years, then you will get 75% of your overall premium paid as a Guaranteed Surrender Value. And, the Cash Bonus is not a guaranteed one.

When can the policy be surrendered earliest after having paid all premia

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both options and proceed with the better option.

80% of the times, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Hi,

A seller suggested this product for my son who is 18 yrs.

His explanation was as follows:

I pay annual premium of Rs.1 lac for 12 yrs.

From the second year I get annual bonus of Rs. 40500 till my son turns 100 yrs.

Is it true?

They say bonus @ 8% is 40500. They never explained 8% of what is 40500.

Can you advise me pl.

Regards

Raja

Yes it is true. As per the cash bonus, 8% is not a guaranteed one. It is the assumed rate of return. 8% of your annualized premium.

I want to surrender my HDFC Life Sanchay Par ADvantage Policy I have paid 1 premium of Rs.16000/-

There is a free look period of 15 and 30 days to cancel the policy.

If you have taken this plan directly from the company then you have the option to return the policy by stating the reason within 15 days from the date of receipt of the policy.

Whereas, if you have taken this policy through some other medium such as online, telephone, which does not involve face to face interaction, then you will have a free look-in period of 30 days.

After free look period, you can submit your cancellation or complaint request in an Online or Offline Format.

A written request or an email with the registered email id is mandatory.

You can send your e-mail to service@hdfclife.com.

For more details, you should read this current official document of HDFC Life Sanchay Par Advantage.

All grievances (Service and sales) received by the Company will be responded to within the prescribed regulatory Turn Around Time (TAT) of 14 days.

On receipt of your letter along with the original policy document, you will get the refund of your paid premium, but it will be subject to deduction of the proportionate risk premium for the period on cover, the expenses incurred by the company for stamp duty and medical examination if any.

In your case, you can surrender your plan without deduction within 2 years.

Yesterday I took this policy, now I want to cancel. May I know the procedure to cancel this. Please help me on this. Thanks in advance.

Hi Bharathi,

Good that you realised it early. You have 15 days free looking period for the policy. Within that 15 days, you can surrender the policy without any charges.

Please go ahead and surrender asap.

Its usefull if your annual interest earning is greater than 40-50 k in FD or 1L in mutual fund on yearly basis as the payout which comes from life insurance policies are exempted under section 10(10) D of Income tax law of EEE ( exempt at inception ( Section 80 C , exempted at regular payout as benefit ( Guaranteed / non guaranteed both ) under section 10(10) D and the maturity as well under section 80C .

Its a different segment of saving as every individual is having different perspective of saving and investment for his or her short term / mid term / long term financial planning .

The returns from PPF is also tax-free.

THe post-tax returns of ELSS are better than the returns of this policy.

When better returns can be earned from similar investment options, I am not seeing a point in investing in this policy.

Thank you. I reverted back after reading your review and discussing with the manager. Not really beneficial.

We are glad that our article help you take a better financial decision. Thanks for sharing your experience.

I think this best plan to invest

Thank you for sharing your opinion. But, it is advisable to work out the outcome (less life cover and less returns) and proceed with the better option.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

I didn’t understand one thing, they say 28%pa, 40%pa as guaranteed income, but why we calculate using 8%pa and 4%pa

Instead of relying on what they say. We can rely on the benefit illustration generated from their website.

thank you for response. But in the illustration table only they have mentioned 22%, so still I am not able to understand your points. Can you please clarify more.

It will be clearer if you read the brochure. 22% is the Guaranteed Income you receive from the policy. 22% of your annualized premium.

By mistake I have taken this policy,

Now How many years I have to pay to To get my money With minimum loss

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans like PPF or MF.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the times, option 1 is better.

You can consult a financial planner to choose the better option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

I was about to invest in this. Good that I read your review before investing. Now i don’t invest in this. Thanks a lot for your in depth analysis.

Thanks for your feedback.

Glad that it helped you!

I have received the policy document today and after reading your article I have decided to cancel it ,will I get back my full premium without any deduction my premium amount is 150000

There is a free look period of 15 and 30 days to cancel the policy.

On receipt of your letter along with the original policy document, you will get the refund of your paid premium, but it will be subject to deduction of the proportionate risk premium for the period on cover, the expenses incurred by the company for stamp duty and medical examination if any.

Your IRR calculation is wrong. And the policy Premium paying term can be chosen by customer. Two options# Limited(30 to 40 yrs) and life time

And now FD/RD rate is very low.ie, 4.9 percent only. Instead of putting in FD , we can invest in Sanchay Par.

In the worst-case scenario, the return in HDFC Life Sanchay Par Advantage Plan is lower than bank FDs. The return from the best-case scenario is not a guaranteed one.

Thanks for the detailed anlysis , this really helps

Glad to know that Krishna.

I am paying 2lakh per annum as premium for 10 years and I want to surrender after 10 years only. How much will I receive at the end of 10 years along with the cash bonus?

You will get 75% of your overall premium paid and based on your policy option, you will receive 4% – 8% of cash bonus p.a. plus guaranteed return (only in Deferred Income Option).

Well explained to take decision for Investment. Was very helpful. Thanks for sharing same

You are welcome Pratik

Thanks for your in-depth analysis. Saves me from falling prey to misselling.

Hi Guha,

We are happy that, it helped you.

Thanks for this article , my HDFC relationship manager is forcing me to take this policy.

now i will not take this policy , who know what will be return after 5 years , there is no guarantee return mentioned in Policy

only either 4% or 8 % , its better invest in post office some good scheme is there.

Glad to know that we can help you!

As per the HDFC RM the guaranteed income payout of 28% starts immediately after completion of the first year but you have mentioned that it will start after the last premium amount has been paid. Could you please clarify? Also, is there any tax benefit if invested in this scheme? If yes what would that be?

Hi!

Guaranteed income is only available in the Deferred Income Option. And you will receive the Guaranteed income payout only after one year of the completion of all your PPT. Please confirm the policy option with your RM. Because there are two income policies are available under this policy on the premium you pay and its benefits.

Also, yes there is a tax benefit available under the policy. It is advisable to consult your tax advisor to avail of tax benefits on this policy.

I have paid 1L annually in HDFC life progrowth plus for 3 yrs. I didn’t see any returns till now even after 3 yrs. RM suggesting to continue plan as 5 yrs lock in period. If you surrender now, some % will be deducted after 5 yrs maturity. What can I do now. I have no interest continuing this plan. Now RM is saying to opt sanchay or sanchay par advantage because it is guaranteed. He said immediate returns. I don’t have confident to take. Looking for LIC Jeevan Anand 15yrs premium paying plan. I need it investment wise and also to show in 80C. Your comment on this .

Since you have already taken this insurance plan, then you have two options.

Option: 1 You can surrender and encash the policy. And reinvest the surrender value and future premium money with better investment plans.

Option: 2 You can continue with the insurance plan until the policy matures.

It is advisable to work out the outcome of both the options and proceed with the better option.

80% of the time, option 1 is better.

You can consult a financial planner to choose the better investment option.

Or

You can take advantage of our free complimentary financial plan consultation and talk to our financial planners.

Get your appointment here: https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Thanks for your explanation! it helps me a lot

Very useful reviews the rm was so efficient in convincing.

What is your view on Bajaj Allianz Life Income Assure ?

Hi,

We are planning to write more review articles in the future. We will keep this policy on our list.

Until then if you need personalized advice, you can schedule a free financial plan consultation with our Certified Financial Planners.

Please click link and register for our 30-minute Complimentary Financial Plan Consultation to get your appointment.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Omg. I was about to sign up for this. Got to see your review just now.

Excellent article educating on annuity investment products…. what ends attracting for many is the fact that the money is locked and so you dont end up frittering away… So long one disciplined in savings and investment then this or any life product is not worth.

Rgds

Thank you for sharing your view with us.

have invested in this policy in jan 2020, 5 lakhs annually , will complete 1 year on 3rd jan 2021. how do i cancel it ? and if i cancel it will I get my paid premium fully or how much deduction will be there.

took the 6 year plan .

Hi,

There is a free look period of 15 and 30 days to cancel the policy.

In your case, you can surrender your plan without deduction within 2 years.

After the free look period, you can submit your cancellation or complaint request in an Online or Offline Format.

A written request or an email with the registered email id is mandatory.

You can send your e-mail to service@hdfclife.com.

For more details, you should read this current official document of HDFC Life Sanchay Par Advantage.

All grievances (Service and sales) received by the Company will be responded to within the prescribed regulatory Turn Around Time (TAT) of 14 days.

On receipt of your letter along with the original policy document, you will get the refund of your paid premium, but it will be subject to deduction of the proportionate risk premium for the period on cover, the expenses incurred by the company for stamp duty and medical examination if any.

Thanks much…I was about to check about this plan as my RM suggested. Thank god accidentally check this review.

HDFC LIFE SANCHAY PAR ADVANTAGE

They are promising an annual payout of 36% for people between the age group of 35 to 45 years for an investment of 1 lakh with a policy term 12 years.

How the payout is caculated and if this 36% is true , what would be my income from hdfc’s payout for the above scenario.

Please could you comment and do advise a best investment plan that yields 2.5 % or more as guaranteed monthly income .

Hi,

For personalized advice, you can schedule a free financial plan consultation with our Certified Financial Planners.

Please click the link and register for our 30-minute Complimentary Financial Plan Consultation to get your appointment.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

If my premium is 33,333 p.m then how much fixed amout return benefit per month i get from hdfc life till i surrender policy .

Please check the return on HDFC Life Sanchay Par Advantage plan calculator in their website.

Hi, can you please also suggest on the below plan ADITYA BIRLA SLI Guaratee 360 solution plan. I am not able to see any reviews online… so need some guidance

Hi,

We are planning to write more review articles in the future. We will keep this policy in our list.

Until then if you need personalized advice, you can schedule a free financial plan consultation with our Certified Financial Planners.

Please click the link and register for our 30-minute Complimentary Financial Plan Consultation to get your appointment.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Hi, Thanks a lot for detailed information. I was trying to see how is LIC Jeevan Umang. I didn’t see that information in your website. Could you please give some details on LIC Jeevan Umang, Plan wise it is almost same as HDFC Sanchay Par Advantage deferred income option. But not sure are they really same or different. Which one is better?

Thanks a lot in advance.

You are really doing a great job by giving wonderful details. Really appreciate all your help to the community

How to get in touch with you for advise?

Hi,

We are planning to write more review articles in the future. We will keep this policy on our list.

Until then if you need personalized advice, you can schedule a free financial plan consultation with our Certified Financial Planners.

Please click the link and register for our 30-minute Complimentary Financial Plan Consultation to get your appointment.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation//

thank you, very helpful.

Glad we can help you Shilpa.

Thanks for the clarification on this! Great I came across this article as I was very confused.

You are welcome Rohit.

Thank you so much Holistic for this feedback. You have helped me out of a real jam

Keep up the good work

Thank you for your appreciation.

Sir,I want to invest 1 lack INR per annum in MF but don’t know how.kindly guide me.

Hi,

For personalized advice, you can schedule a free financial plan consultation with our Certified Financial Planners.

Please click the link and register for our 30-minute Complimentary Financial Plan Consultation to get your appointment.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/

Thanks for the info. Definitely it gives a balanced view. We are warned not to fall for RM who pushes this product.

Glad we can help you Sandhya.