Max Life Smart Wealth Plan.

Is this insurance policy the smartest way to create wealth?

How can you take an informed decision, about whether you should invest in this insurance policy or not?

What are the pros and cons of this plan?

To make the decision-making easy for you, this is our honest Max Life Smart Wealth Plan Review.

Table of Contents:

- Features of Max Life Smart Wealth Plan

- Max Life Smart Wealth Lumpsum Plan Review

- Max Life Smart Wealth Short term Income Plan Review

- Max Life Smart Wealth Long-term Income Plan Review

- Max Life Smart Wealth Whole Life Income Policy Review

- Max Life Smart Wealth Plan vs Other Investment Plans

- Max Life Smart Wealth Plan: Pro or Con?

- How to Surrender/Cancel your Max Life Smart Wealth Plan?

- Max Life Smart Wealth Plan: Good or Bad

This article explains the key aspects, benefits, and returns of the Max Life Smart Wealth Plan.

You will also discover if Max Life Smart Wealth Plan is superior to most plans in the market in terms of Return Rate and flexibility or not.

By the end of this article, you will be able to take a more informed decision regarding whether you should invest in this plan or not.

The video below will offer you a quick overview of the Max Life Smart Wealth Plan and its key aspects. Let’s take a closer look.

Features of Max Life Smart Wealth Plan

Max Life Smart Wealth Plan is a savings plus insurance plan from Max Life Insurance. A savings plus insurance plan means that it has the features of both a savings plan and a life insurance plan.

The Investment Side of Max Life Smart Wealth Plan Review:

You invest a certain amount every year in this plan. At the time of the maturity of the plan, you will get a lump sum amount or periodic income for the investments that you made in the plan during its term.

The Insurance Side of Max Life Smart Wealth Plan Review:

If during the term of the plan you die, your dependents will get life insurance like payment from the plan. This payment is meant to ensure that they are compensated for the loss of income because of your unfortunate and untimely death.

Product Nature of Max Life Smart Wealth Plan Review:

Max Life Smart Wealth Plan is a non-linked product. Non-linked product means that it does not invest in stocks or the stock market. Being a non-linked product, Max Smart Wealth Plan gives you assured, guaranteed returns.

Max Life Smart Wealth Plan Option Review:

There are four plans option in Max Life Smart Wealth Plan.

Investors can choose as per their needs.

i) Lumpsum plan.

ii) Short-Term Income Plan.

iii) Long-Term Income Plan.

iv) Whole Life Income Policy.

The Eligibility conditions for each of these plans are stated in the table below.

The Eligibility conditions for each of these plans are stated in the table below.

|

Eligibility Criteria |

Plan Option |

Minimum |

Maximum |

|

Age at Entry (Years) |

Lumpsum |

0 (91 Days) |

65 |

|

Short Term Income |

5 |

65 |

|

|

Long Term Income |

4 |

65 |

|

|

Whole Life Income |

Single Pay- 45 (Younger life) |

65 (Older Life) |

|

|

Regular pay- 40 (Younger Life) |

65 (Older Life) |

||

|

Age at Maturity (Years) |

Lumpsum |

18 |

85 |

|

Short Term Income |

18 |

73 |

|

|

Long Term Income |

18 |

74 |

|

|

Whole Life Income |

50 |

71 |

|

|

Minimum Premium |

Lumpsum |

Annual |

Rs. 11,000 |

|

Semi Annual |

Rs. 5,583 |

||

|

Short Term Income |

Quarterly |

Rs. 2,814 |

|

|

Long Term Income |

Monthly |

Rs. 943 |

|

|

Whole Life Income |

Single Pay |

Rs. 2,50,000 |

|

|

Regular Pay (Annual) |

Rs. 50,000 |

||

|

Regular Pay (Semi Annual) |

Rs. 25,375 |

||

|

Regular Pay (Quarterly) |

Rs. 12,790 |

||

|

Regular Pay (Monthly) |

Rs. 4,285 |

||

|

Maximum Premium |

All Options |

No Limit |

|

|

Premium Payment Mode & Modal Factors |

Lumpsum |

Annual, Semi Annual, Quarterly & Monthly |

|

|

Premium Payment Mode |

Modal Factors |

||

|

Annual |

1 |

||

|

Semi Annual |

0.5075 |

||

|

Quarterly |

0.2558 |

||

|

Short Term Income |

Monthly |

0.0857 |

|

|

Long Term Income |

|||

|

Whole Life Income |

Single Premium & Regular Pay |

||

|

Premium Payment Mode |

Modal Factors |

||

|

Annual |

1 |

||

|

Semi Annual |

0.5075 |

||

|

Quarterly |

0.2558 |

||

|

Monthly |

0.0857 |

||

|

Gender |

Male, Female and Transgender |

||

Source: Max Life Smart Wealth Product Broucher

1. Max Life Smart Wealth Lumpsum Plan Review

Under this plan, you will receive a fixed sum at the time of maturity of the plan. So you will invest a fixed amount every month or year into the plan during the term of the plan. At the time of maturity, you will get a fixed amount. This fixed amount will include the periodic (monthly or yearly) investments of your savings that you made in the plan. It will also include a return over this fixed amount for the investments that you made in the plan.

The added benefit is that if you die at any time during the term of the policy your dependents or family members will get a lump sum amount as a life insurance/death benefit.

This amount will be the highest of,

- 11 times the sum of all premiums that you had to pay on the policy or

- 105% of total premiums that you had paid till the time of your death or

- The amount that you chose is the one that your dependents should get in the event of your death.

Analysis of Max Life Smart Wealth Lumpsum Plan Returns:

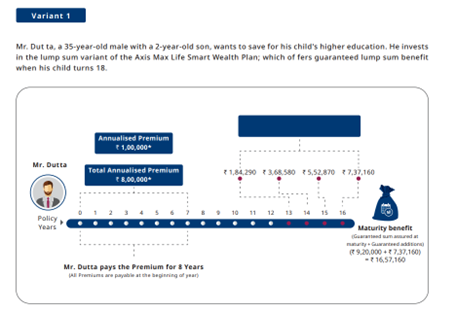

Under the lump sum investment option, you pay a premium for a limited period and receive the maturity benefit at the end of the term. Here, he pays an annual premium of ₹ 1 Lakh for 8 years and gets the Guaranteed sum assured on maturity and guaranteed additions of ₹ 16.57 Lakhs.

An IRR of 5.93% is low for a long-term investment. You will get higher returns even if you invest in a completely risk-free asset, such as a government bond or PPF.

So based on our evaluation, Max Life Smart Wealth Lumpsum Plan is not so a smart option for even the most conservative investor.

Let’s analyze if other options of this Smart Wealth Plan are better or even worse.

2. Max Life Smart Wealth Short-Term Income Plan Review

If you choose this plan of Max Life Smart Wealth Plan, then you will get a periodic income for a short period after the maturity of this product. This income can be monthly, quarterly, six-monthly, or annually depending on what you choose.

There are many options under this plan in terms of the period for which you will get the income.

- Guaranteed period income for 6 years.

- Guaranteed income for 8 years.

- Guaranteed income for 10 years.

- Guaranteed income for 12 years.

The amount of income that you will get will depend on the periodic savings that you put into this plan and the length for which you put these savings.

This plan too has a life insurance benefit. If you die during the policy term of this plan, your dependents or family members will get a lump sum amount as a death benefit.

This amount will be the highest of

- 11 times the sum of all premiums that you had to pay on the policy or

- 105% of total premiums that you had paid till the time of your death or

- The amount that you chose is the one that your dependents should get in the event of your death.

Analysis of Max Life Smart Wealth Short-term Income Plan Returns:

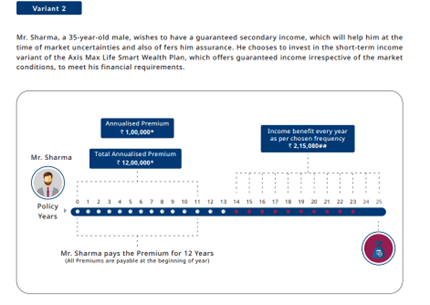

If you are a 35-year-old male and take this policy for 13 years and pay an annual premium of ₹1,00,000 every year for 12 years, then you will get an annual income of ₹2,15,080 for 12 years after the end of the policy term of 13 years.

The IRR (Internal Rate of Return)that you will get is a mere 6.08% per annum.

Max Life Smart Wealth Short-term Income Plan IRR is much higher than the Lumpsum Plan. Yet, it is still a much lesser return compared to the 7.1% of the Govt. of India guaranteed PPF returns.

3. Max Life Smart Wealth Long-Term Income Plan Review

Under the long-term income plan of Max Life Smart Wealth Plan, there are two options.

- There is a guaranteed income plan where you will get guaranteed income for 30 years after the end of the policy term of the plan.

- There is also a plan where you will get guaranteed income for 25 years after the maturity of the term of your plan.

The amount of income that you will get will depend on the periodic savings or premiums that you choose to make into this plan.

Like in other plans, you will get the life insurance benefit under this plan too. In case you, unfortunately, die during the term of this plan, your dependents will get a lump sum amount as a death benefit.

This amount will be the highest of,

- 11 times the sum of all premiums that you had to pay on the policy or

- 105% of total premiums that you had paid till the time of your death or

- The amount that you chose is the one that your dependents should get in the event of your death.

Analysis of Max Life Smart Wealth Long-term Income Plan Returns:

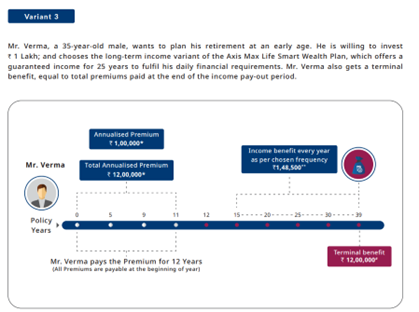

Suppose you are a 35-year-old male.

You buy this policy for 15 years with a premium payment term of 12 years. You pay an annual premium of ₹1,00,000 for 12 years in this plan. At the end of 15 years, your policy will mature. From the 16th year onwards you will start getting an annual income of ₹1,48,500. This annual income you will get up to the 40th year. This means that you will get an annual income for 25 years. Your Internal Rate of Return (IRR) will be just 6.7%.

It is the third Max Life Smart Wealth policy plan and the one with a long payout period. But even with a long payout period, it offers returns only at a rate of 6.7% (policy term 40 years)

Next, we’ll discover whether the Whole Life Income option of Max Life Smart Wealth is good or bad in terms of returns.

4. Max Life Smart Wealth Whole Life Income Policy Review

Under this plan you can insure yourself and one other person, such as your spouse.

The policy will keep on giving lifetime income until the death of both of you.

Also, at the time of the death of the last surviving of the two persons for which life insurance cover has been taken, a lumpsum amount will be paid to the nominee or the surviving members of your family.

This lump sum amount will be higher by 1.25 times the single premium you had to pay on the policy or the lump sum amount that you agreed to at the time of taking the policy.

Analysis of Max Life Smart Wealth Whole Life Income Plan Returns:

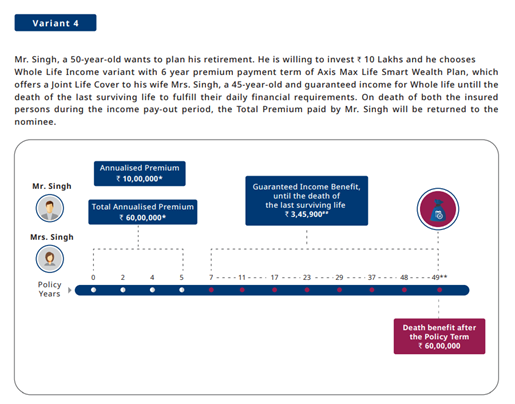

Suppose you are a 50-year-old married male.

You take this whole life income policy. You take joint life insurance coverage with your spouse as part of this policy.

Your wife is 45 years old. You invest ₹10,00,000 in this policy for 6 years. This means that you pay the entire premium of ₹60,00,000.

The term of the policy that you have taken is 6 years. From the 7th year onwards you will get an income of ₹3,45,900 annually.

This annual income payment will continue till the death of both you and your wife.

After the death of both of you, the premium of ₹60,00,000 that you paid at the time of taking the policy will be returned to the nominee as life insurance benefit.

Now, the average life expectancy in India currently is around 85 years.

If we assume that both you and your wife die when each of you turn 85 years old, this policy will pay income for 28 years.

Your IRR from this policy is around 4.4% per annum. And it is the lowest return rate of all the Max Life Smart Wealth Plan options.

The IRR is a below-par average for such a long-term of investment. In comparison, even the Govt. of India assured PPF offers far better returns at a 7.1% interest rate as of Q1 2025.

Max Life Smart Wealth Plan vs Other Investment Plans

Comparison of Max Life Smart Wealth Plan vs PPF

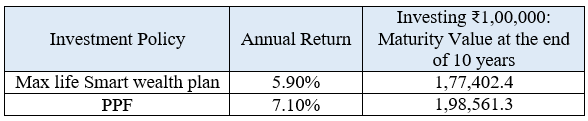

Among the four plans of the Max Life Smart Wealth Plan, we chose the Lump sum variant for easy comparison.

Its IRR is 5.9%.

Let’s compare this IRR to the annual return of the Public Provident Fund (PPF)—that is, if you invested the same amount in PPF instead of the Max Life Smart Wealth Lump sum Policy.

The prevailing annual interest rate on PPF currently is 7.1%. You will earn guaranteed returns at a 7.1 % annual interest rate in PPF in comparison to just a 5.9% interest rate in Max Life Smart Wealth Plan’s Lump sum whole life income policy.

The much interesting part is that you can take a portion of the money and buy a term insurance plan before investing in PPF.

Advantages of PPF + Term Insurance Combination:

- i) Higher Life Cover with Term Insurance Plan

- ii) Still Higher Returns From PPF on Maturity

It is one of the best approaches to satisfy your life insurance policy and investment needs. By keeping your insurance policy and investments separate, you have superior flexibility and control over your finances.

Comparison of Max Life Smart Wealth Plan Vs ELSS Mutual Fund

PPF + Term Insurance is ideal for conservative investors with low-risk appetite.

But you have an even better investment strategy if you have a better risk tolerance.

But I should remind you, investment risk tolerance is not an inherited trait. It is a learnable trait—much like a skill.

Your other better option is the ELSS Mutual Fund + Term Life Insurance Policy combination.

If you had put this money in an equity-linked mutual fund (ELSS), the average CAGR would be 12%.

You can see that the return is almost twice that of the Max Life Smart Wealth Plan.

It is often even more than 12% CAGR, depending upon the performance of that particular mutual fund scheme.

However, ELSS mutual funds are more volatile investment instruments, and their returns are not guaranteed like PPF. Its returns are dependent on the returns of the broader stock market.

Hence, it is a must to evaluate your investment risk tolerance level before choosing to invest in ELSS Mutual Funds.

But, you can always approach a Certified Financial Advisor. They can evaluate your investment risk tolerance level and help you decide what is good and bad for you based on your needs.

Max Life Smart Wealth Plan vs Max Life Smart Wealth Advantage Guarantee Plan(SWAG)

A non-linked, non-participating, individual life insurance and savings plan is the Max Life Smart Wealth Advantage Guarantee Plan (SWAG).

Through their “Early Wealth” version, you have the choice to start receiving money as early as the first year.

Read the complete review below with IRR(Internal Rate of Return) analysis with illustration and precise calculation of Surrender Value.

Max Life Smart Wealth Advantage Guarantee Plan(SWAG) Review – Is It a Smart Investment Choice?

Max Life Smart Wealth Plan vs Max Life Smart Wealth Income Plan

A non-linked, participating individual life insurance savings plan is the Max Life Smart Wealth Income Plan. You have three plan alternatives to pick from, depending on whether you want your income now or in a few years.

Read the complete review of this plan below for a better comparison against every aspect like Surrender Value.

Max Life Smart Wealth Income Plan Review: Is It Worth Investing?

Max Life Smart Wealth Plan vs other investment plans – a comprehensive review

If you have attentively read the review up to this point, you may have drawn a conclusion. Yes! Max Life Smart Wealth Plan is by significantly inferior to ELSS or PPF + Pure Term Insurance.

We should assess and contrast it with other investment possibilities rather than getting swept away by the marketing of a new plan on the market. This in turn will assist us in reviewing and determining the best course of action for our future.

Max Life Smart Wealth Plan: Pro or Con?

The definite answer is CON!

This Max Life Smart Wealth Plan Review clearly clarifies that this plan is neither smart nor wealth-creating for investors.

The argument can be given that this Max Life Smart Wealth Plan also offers life insurance benefits. But you can get these exact life insurance benefits at much lower annual premiums by buying a term insurance plan.

The savings that you make on the life insurance premiums by buying a term insurance plan and not Max Life Smart Wealth Plan can be invested in a PPF account or ELSS mutual fund.

You can thus make higher returns on your savings than what you will make by investing in Max Life Smart Wealth Plan.

How to Surrender/Cancel Your Max Life Smart Wealth Plan?

It is very apparent that the Max Life Smart Wealth Plan is neither smart nor creates wealth for you.

No smart investor would buy the Max Life Smart Wealth Plan.

But what if you already have bought this Plan?

Surrendering Max Life Smart Wealth Plan: Free-Look Period

The freelook period of any life insurance policy is 15 days.

This means that after buying the plan, you will have 15 days to return the policy, if you are not satisfied with its terms and conditions, review it. Your premium amount will be returned minus any expense Max Life incurred on underwriting, such as the cost of any medical examination.

Surrendering Max Life Smart Wealth Plan: After Free-Look Period

In case your free look period has ended, and you want to surrender it now, you just need to call Max Life Smart Wealth Plan.

They will provide you with a surrender form. You have to fill in the necessary details and submit it.

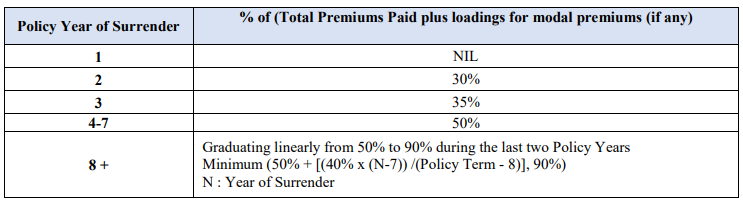

The surrender value of your policy will include all the premiums that you have paid till the time of surrender, after deducting the relevant expenses that they have incurred in managing your policy.

See the table below for the Guaranteed Surrender Value calculation of the Max Life Smart Wealth Plan.

You may not be sure whether it is financially a better decision to surrender or not.

You may not be sure whether it is financially a better decision to surrender or not.

But as a general rule, it is always good to surrender your policy in the early years when you have better alternate investment options.

This way you can earn more if you invest the money that you get from surrendering the policy, in PPF or ELSS. You will be able to recover any loss that you incurred because of surrendering your Max Life Smart Wealth policy before maturity.

If you are concerned about the complications in surrendering the policy, approach a Certified Financial Advisor. They can give you financially sound advice based on your financial situation and requirements.

For more surrender value and other details about the Max Life Smart Wealth Plan, you can download the Max Life Smart Wealth Plan Brochure PDF.

Max Life Smart Wealth Plan: Good or Bad?

- Max Life Smart Wealth Plan is not superior to most plans in the market in terms of Return Rate and flexibility. As a result, according to our evaluation, it is a mediocre product with more disadvantages than advantages.

- It is not the right choice for life insurance or investments. And you have seen the calculation in solid numbers.

The returns Max Life Smart Wealth offers are lower than the returns offered by PPF and ELSS mutual funds. You can always get your insurance covered with a term insurance policy at much lower premiums. Never fall for any financial products that will not make your financial life better in any way.

Always look for better options, do your own research, and make a sound financial decision.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30-minute FREE Financial Plan Consultation. Click the ‘‘BOOK YOUR SLOT NOW!’’ button below.

Very nicely explained. Would like to mention two points:

1. Over the past few years, Max Life SWP has improved on income part for same premium amount. For eg, A policy having annual premium of Rs 50000(+GST) with PPT of 12 years and PT of 14 years is giving annual income of Rs 64515/- for a period of 25 years.

2. When you compare Life Insurance product with PPF and talk about guaranteed long term income or whole life income, you should keep in mind that even a scheme backed by GOI like PPF can have interest reduced to any value like 6.5% or less with cooling of Inflation and other factors in future. Whereas for Insurance product with commitment of 25+ years gives you guaranteed income. Its all about risk appetite of the investor to make a decision.

Thank you for your insights! While insurance products like Max Life SWP offer guaranteed income over a long period, PPF remains a strong contender for many investors due to its triple tax exemption (EEE) status and sovereign guarantee. Although PPF interest rates can change, they have historically remained competitive. Additionally, PPF offers flexibility, safety, and tax benefits, making it a solid choice for risk-averse investors looking for stable returns over the long term.

Great analysis. How does the calculations change if you are contributing more than 1.5 lakhs per year and you are in the 30 percent slab. For example if I contribute 5 lakhs a year , I get 30 Percent tax savings on additional 3.5 lakhs that I won’t get through PPF contribution.

“Hi!

For PPF or ELSS or Insurance Premium, the maximum limit given under sc 80 c for tax saving is 1.5 lacs. There seem to be some wrong assumptions in your question.

you can take advantage of our 30-minute complimentary financial plan Consultation to talk with our certified financial planner.

Please click the link to get your appointment.

https://www.holisticinvestment.in/complimentary-financial-plan-consultation/“