“You can’t afford to go wrong when it comes to planning for one’s Life Goals…”

It is a compelling statement from the Bajaj Allianz Goal Assure policy brochure.

Well, I agree!

And it is exactly why I chose to review this policy. After all the ULIP policy is suggesting Goal Assurance in its name.

Can the Bajaj Allianz Life Goal Assure help you achieve your goals optimally?

Buying Bajaj Allianz Life Goal Assure is a good or bad investment for your future?

What are the pros and cons of this plan?

Let’s find out through a detailed review of Buying Bajaj Allianz Life Goal Assure with Fund Value, Fund performance, Charges, Benefits, etc. All of this with precise calculations and illustrations!

Table of Contents:

1.)Key features of Bajaj Alliance Life Goal Assure Review

2.)Funds of Bajaj Allianz Life Goal Assure Policy Review

3.)Investment Strategies of Bajaj Allianz Life Goal Assure Review

4.)Benefits Review of Bajaj Allianz Life Goal Assure Policy

5.)Maturity Benefit of Bajaj Allianz Life Goal Assure

6.) Review of Charges under Bajaj Allianz Life Goal Assure

7.)Taxation of Bajaj Allianz Life Goal Assure Review

8.) Bajaj Allianz Life Goal Assure vs PPF: Review

9.) Bajaj Allianz Life Goal Assures vs ELSS Mutual Fund: Review

- Bajaj Allianz Life Goal Assures vs Bajaj Allianz Life Long-life Goal Plan

- Bajaj Allianz Life Goal Assures vs Bajaj Allianz Life Assured Wealth Goal

- Bajaj Allianz Life Goal Assures Vs Other Investment Options – Review Conclusion

10.) Who Should Consider Bajaj Allianz Life Goal Assure?

11.)Verdict Bajaj Allianz Life Goal PlanVerdict: Good or Bad?

12.)How to surrender your Bajaj Allianz Life Goal Assure Policy? An Analysis

13.)Conclusion

Bajaj Alliance Life Goal Assure is a Unit Linked Insurance Plan (ULIP). And this Bajaj Allianz Goal Assure review is probably the most detailed one with illustrations and examples.

So let’s start with…

1.) Key features of Bajaj Alliance Life Goal Assure: Review

The table below shows the key features and the eligibility criteria for the Bajaj Allianz Goal Assure policy.

The Bajaj Allianz Life Goal Assure minimum premium and premium payment options are designed to suit different long-term financial goals and investment preferences.

The other notable features of the Bajaj Allianz Goal Assure policy are:

Option to reduce the premium amount—after the completion of the 5-year lock-in period.

Option to change the premium paying term—after the completion of the 5-year lock-in period.

Option of partial withdrawal—with certain restrictions as mentioned in the policy document.

Option to top-up your premium—in the form of a lump-sum payment.

Option to reduce your Sum Assured—provided it is not lesser than 10x of your annual premium.

On surviving the policy term, all the mortality charges will be paid back on policy maturity.Option to receive maturity benefits in instalments—over a maximum period of 5 years.

Read more about the Bajaj Allianz Goal Assure in the official policy brochure pdf in detail.

2.) Funds of Bajaj Allianz Life Goal Assure Policy: Review

The Bajaj Allianz Goal Assure policy offers 10 different fund options with varying return-risk levels.

This will help you to switch funds according to Fund Performance.

Regularly reviewing the Bajaj Allianz fund fact sheet and Bajaj Allianz fund performance can help policyholders make informed fund-switching decisions based on market conditions.

The funds in this policy are listed below.

|

Asset Allocation |

|||||

|

S no. |

Fund Name |

Equity |

Debt |

Money Market |

Risk profile |

|

1 |

Equity Growth Fund II |

Not less than 60% |

0% – 40% |

0% – 40% |

Very High |

|

2 |

Accelerator Mid-Cap Fund II |

Not less than 60% (at least 50% in Mid cap) |

0% – 40% |

0% – 40% |

Very High |

|

3 |

Pure Stock Fund |

Not less than 60% |

0% – 40% |

0% – 40% |

Very High |

|

4 |

Pure Stock Fund II |

Not less than 75% |

— |

0% -25% |

Very High |

|

5 |

Asset Allocation Fund II |

40% – 90% |

0% – 60% |

0% – 50% |

High |

|

6 |

Blue-chip Equity Fund |

Not less than 60% |

0% – 40% |

0% – 40% |

High |

|

7 |

Bond Fund |

— |

40% – 100% |

0% – 60% |

Moderate |

|

8 |

Liquid Fund |

— |

— |

100% |

Low |

|

9 |

Flexi Cap Fund |

65% – 100% |

0% – 35% |

0% – 35% |

Very High |

|

10 |

Sustainable Equity Fund |

65% – 100% |

0% – 35% |

0% – 35% |

Very High |

There is also the feature of a fund booster in this policy.

The fund booster is that, at the time of maturity, the insurer will pay a non-guaranteed bonus under certain conditions.

If your policy premium is ₹5 lakh p.a. or above with the policy term 10 years or more, your policy will be eligible for loyalty additions.

The loyalty additions available under Bajaj Allianz Life Goal Assure IV can further enhance the maturity corpus for eligible long-term investors.

3.) Investment Strategies of Bajaj Allianz Life Goal Assure: Review

This policy gives you the option to choose from four portfolio investment strategies. Your premiums will be invested according to the portfolio investment strategy that you have chosen. The four portfolio investment strategies that you can choose from are:

- Investor Selectable Portfolio Strategy

- Wheel of Life Portfolio Strategy

- Trigger-Based Portfolio Strategy

- Auto Transfer Portfolio Strategy

The availability of multiple investment strategies makes Bajaj Allianz Goal Assure suitable for investors with different market outlooks and financial objectives.

Investor Selectable Portfolio Strategy: Analysis

Under the Investor Selectable Portfolio Strategy option, you can choose to invest your premium in any of the 8 funds available.

No specific investment strategy will be employed by the policy in this option.

Wheel of Life Portfolio Strategy: Analysis

In the Wheel of Life portfolio strategy, your premiums will be invested across equity and debt funds based on years to maturity.

If the years to maturity is higher, a higher allocation is given to the equity funds and vice versa.

This helps in reducing the portfolio volatility as the policy nears maturity.

Trigger-Based Portfolio Strategy: Analysis

In the Trigger-based portfolio strategy, your investments will follow a fixed 75%: 25% asset allocation ratio.

That is 75% towards Equity Growth Fund II and 25% towards the Bond fund.

Whenever the equity allocation increases by 15%, the asset allocation will be rebalanced.

By rebalancing periodically, this strategy helps book profit by moving funds from the high-risk equity fund to the low-risk Bund fund.

Auto Transfer Portfolio Strategy: Analysis

In the auto-transfer portfolio investment strategy, your premium is invested in a low-risk bond or liquid fund.And at the beginning of every month, the money in the low-risk fund will be transferred to a high-risk/high-return fund of your choice systematically.

You can switch from your selected portfolio investment strategy to another portfolio investment strategy during the term of your policy.

This systematic investment approach works similarly to staggered investing and helps reduce the impact of short-term market fluctuations over the policy tenure.

4.) Benefits Review of Bajaj Allianz Life Goal Assure Policy:

Since the Bajaj Allianz Goal Assure is an investment insurance policy.

The benefit can be either the death benefit or the maturity benefit.

As a unit-linked insurance plan, Bajaj Allianz Life Goal Assure combines life insurance protection with market-linked investment opportunities under a single policy.

Let’s see what’s inside each of these benefit alternatives.

Death Benefit: Analysis

The nominee will receive the death benefit in case of the policyholder’s demise while the policy is active.

The death benefit will be the higher sum assured in the policy or the fund value on that date.Suppose you take a Bajaj Allianz Life Goal Assure policy with a policy term of 15 years. Your premium payment term is 10 years.

And your annual premium is ₹50,000.

Your assured benefit is likely to be 10 times the annual premium. I.e., the Sum Assured will be ₹5 Lakhs.

The applicable cover amount depends on the policy terms and premium selected at the inception of the Bajaj Allianz Life Goal Assure policy.

5.) Maturity Benefits Review of Bajaj Allianz Life Goal Assure:

On surviving the policy term, you will receive the maturity value of your policy.

The maturity value will be the fund value of the policy as of the maturity date.

Returns assumption at 4% and 8% are non-guaranteed.

A Bajaj Allianz Life Goal Assure calculator or benefit illustration can provide investors with projected maturity values under different return assumptions before purchasing the policy.

For example, let’s assume that you buy the Bajaj Allianz Goal Assure policy.

The policy term is 15 years with a 10-year premium paying term.

And you are paying ₹50,000 per annum as the policy premium for a life cover of ₹5 lakhs.

We shall assume that your Bajaj Allianz Goal Assure fund choice and Fund Performance gives an 8% CAGR—as suggested in the official policy brochure.

In that case, the maturity benefits at the end of 15 years will be ₹9.70 Lakhs.

It looks pretty straightforward.

However, if we calculate the actual return from the policy, things get complicated.

The table below shows the actual net IRR from the Bajaj Allianz Goal Assure policy in the hand of the investor. I.e., it accounts for the different hidden charges levied on your premium amount and the fund value & Fund Performance over the years.

|

At 4% p.a. |

At 8% p.a. |

||||

|

Age |

Year |

Annualised premium / Maturity benefit |

Death benefit |

Annualised premium / Maturity benefit |

Death benefit |

|

35 |

1 |

-50,000 |

5,00,000 |

-50,000 |

5,00,000 |

|

36 |

2 |

-50,000 |

5,00,000 |

-50,000 |

5,00,000 |

|

37 |

3 |

-50,000 |

5,00,000 |

-50,000 |

5,00,000 |

|

38 |

4 |

-50,000 |

5,00,000 |

-50,000 |

5,00,000 |

|

39 |

5 |

-50,000 |

5,00,000 |

-50,000 |

5,00,000 |

|

40 |

6 |

-50,000 |

5,00,000 |

-50,000 |

5,00,000 |

|

41 |

7 |

-50,000 |

5,00,000 |

-50,000 |

5,00,000 |

|

42 |

8 |

-50,000 |

5,00,000 |

-50,000 |

5,00,000 |

|

43 |

9 |

-50,000 |

5,00,000 |

-50,000 |

5,00,000 |

|

44 |

10 |

-50,000 |

5,00,000 |

-50,000 |

5,00,000 |

|

45 |

11 |

0 |

5,00,000 |

0 |

5,00,000 |

|

46 |

12 |

0 |

5,00,000 |

0 |

5,00,000 |

|

47 |

13 |

0 |

5,00,000 |

0 |

5,00,000 |

|

48 |

14 |

0 |

5,00,000 |

0 |

5,00,000 |

|

49 |

15 |

0 |

5,00,000 |

0 |

5,00,000 |

|

50 |

6,50,581 |

9,70,742 |

|||

|

IRR |

2.51% |

6.36% |

|||

This difference between gross fund returns and net investor returns is an important aspect to consider while comparing ULIPs with other long-term investment options.

Understanding the actual IRR instead of only the projected fund value gives a clearer picture of the effective investment return after policy charges.

In the above illustration, the Net Return Rate is calculated at 6.36%.

For an 8% fund return, your policy will give you a return of only 6.36%.

It is often even lesser since the IRR calculation here has accounted only for the Policy administration charge and the fund management charge.

If we include the risk charge, other miscellaneous charges, and the 18% GST on all the charges, it will be significantly lesser than 6.36%.Hidden charges are one of the most misleading and unattractive features of Bajaj Allianz Life Goal Assure or any other ULIP.

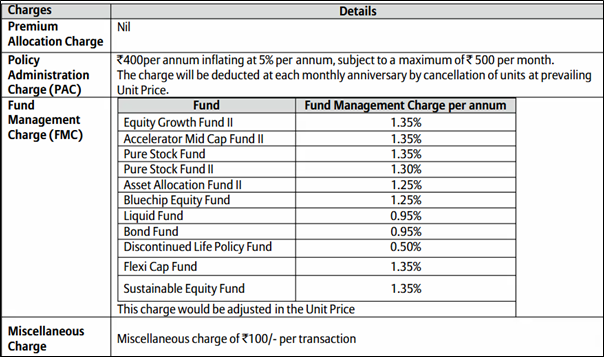

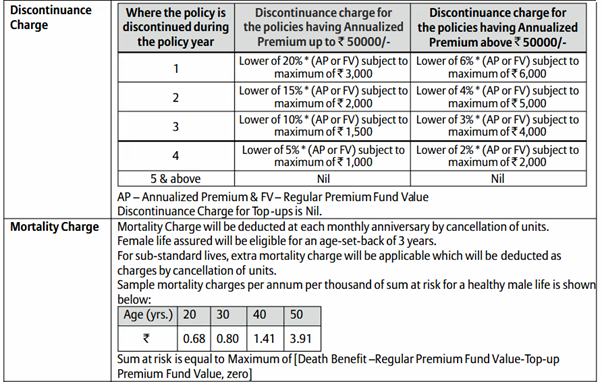

6.) Review of Charges under Bajaj Allianz Life Goal Assure:

Investors should carefully review the benefit illustration and charge structure to understand the long-term impact of these deductions on policy performance.

You should also note that, even though ULIPs have tax benefits, an 18% GST is levied on all the charge deductions.

And it shall be payable from the hands of the investor.

7.) Taxation of Bajaj Allianz Life Goal Assure: Review

Premium payments up to ₹1.5 Lakhs per annum are exempt from income tax u/s 80C.

The entire maturity benefits from Bajaj Allianz Goal Assure are exempt under section 10(10D).

For high-premium policies, investors should evaluate both the tax implications and expected post-tax returns before making an investment decision.

However, this exemption is applicable only if the annual premium is less than ₹2.5 Lakhs—per The Financial Act 2021.

In case the annual premium is over₹2.5 Lakhs, a 10% LTCG tax will be levied on the capital gains—with an exemption on ₹1 lakh of the capital gains.On the other hand, the Sum Assured for the death benefit is entirely exempt from income tax u/s 10(10D).

8.) Bajaj Allianz Life Goal Assure vs PPF: Review

Before making any long-term investment or financial decision you should do some comparison checks.

Let’s compare the investment aspect of Bajaj Allianz Goal Assure against PPF.

Since PPF does not offer life cover, like the Goal Assure plan, you can buy a term insurance plan for the same sum assured for a far lesser premium.

For example, the annual premium for a life cover of ₹5 lakhs of a term insurance policy will be lesser than ₹4,300 per annum.

Public Provident Fund is an investment instrument offered by the Govt. of India giving guaranteed returns.

The current interest rate of PPF is set at 7.1% p.a.

Unlike market-linked ULIP plans, PPF offers stable and government-backed returns, making it a preferred choice for conservative investors.

Investments in PPF also have the same benefit of tax exemption u/s 80C up to ₹1.5 lakh per annum.

The table below shows the return from PPF Fund Performance for the same investment amount, for the same investment period as shown in the policy illustration.

|

Term Insurance + PPF |

|||

|

Age |

Year |

Term Insurance premium + PPF |

Death benefit |

|

35 |

1 |

-50,000 |

5,00,000 |

|

36 |

2 |

-50,000 |

5,00,000 |

|

37 |

3 |

-50,000 |

5,00,000 |

|

38 |

4 |

-50,000 |

5,00,000 |

|

39 |

5 |

-50,000 |

5,00,000 |

|

40 |

6 |

-50,000 |

5,00,000 |

|

41 |

7 |

-50,000 |

5,00,000 |

|

42 |

8 |

-50,000 |

5,00,000 |

|

43 |

9 |

-50,000 |

5,00,000 |

|

44 |

10 |

-47,500 |

5,00,000 |

|

45 |

11 |

-500 |

5,00,000 |

|

46 |

12 |

-500 |

5,00,000 |

|

47 |

13 |

-500 |

5,00,000 |

|

48 |

14 |

-500 |

5,00,000 |

|

49 |

15 |

-500 |

5,00,000 |

|

50 |

9,56,730 |

||

|

IRR |

6.23% |

||

This comparison highlights why many investors review Bajaj Allianz Life Goal Assure returns alongside guaranteed investment options before making a long-term commitment.

In the above illustration, the returns that we get from Investment in PPF @ 7.1% p.a. is calculated at ₹9.56 Lakhs. (PPF requires a minimum contribution of ₹500 p.a., so adjustments were made accordingly).

The return from PPF Fund Performance is almost similar to the return from Bajaj Allianz Goal Assure as shown in the illustration earlier.

Also, the return from PPF is guaranteed, and is entirely exempt from income tax.While Bajaj Allianz Life Goal Assure offers insurance protection and market participation, PPF remains attractive for investors seeking predictable wealth accumulation.

On the other hand, there is no guarantee of the return that you will generate on your Bajaj Allianz Life Goal Assure policy.

You may end up getting a return as low as 4% or even lower.

Also, the returns that you will get on PPF are exempt from taxation.

9.) Bajaj Allianz Life Goal Assures vs ELSS Mutual Fund: Review

ELSS mutual funds are equity-linked funds that invest in shares.

As an alternate option to the Goal Assure plan, you can choose a mix of term life insurance policy and ELSS Mutual Fund.

Many investors compare Bajaj Allianz Life Goal Assure with ELSS funds because both aim for long-term wealth creation while offering tax-saving benefits under Section 80C.

Many financial planners compare Bajaj Allianz ULIP plans with ELSS funds because both are long-term wealth creation instruments with equity exposure.

Equity mutual funds on average offer 12%-15% CAGR. Assuming a conservative 12% CAGR, the potential return from an ELSS mutual fund is shown in the table below.

Unlike bundled insurance products, ELSS investments provide a transparent cost structure and allow investors to track portfolio performance independently.

|

Term insurance + ELSS |

|||

|

Age |

Year |

Term Insurance premium + ELSS |

Death benefit |

|

35 |

1 |

-50,000 |

5,00,000 |

|

36 |

2 |

-50,000 |

5,00,000 |

|

37 |

3 |

-50,000 |

5,00,000 |

|

38 |

4 |

-50,000 |

5,00,000 |

|

39 |

5 |

-50,000 |

5,00,000 |

|

40 |

6 |

-50,000 |

5,00,000 |

|

41 |

7 |

-50,000 |

5,00,000 |

|

42 |

8 |

-50,000 |

5,00,000 |

|

43 |

9 |

-50,000 |

5,00,000 |

|

44 |

10 |

-50,000 |

5,00,000 |

|

45 |

11 |

0 |

5,00,000 |

|

46 |

12 |

0 |

5,00,000 |

|

47 |

13 |

0 |

5,00,000 |

|

48 |

14 |

0 |

5,00,000 |

|

49 |

15 |

0 |

5,00,000 |

|

50 |

14,57,841 |

||

|

IRR |

10.31% |

||

This comparison is particularly useful for investors reviewing Bajaj Allianz Life Goal Assure performance against standalone market-linked investments.

In the above illustration, the ELSS Mutual Fund (12% CAGR) returns are calculated at ₹14.57 Lakhs.

This illustrates why investors often compare Bajaj Allianz ULIP returns with equity mutual fund returns before making a long-term investment decision.

You can see that the ₹14 Lakh return from the ELSS fund is almost ₹5 lakhs more than the Bajaj Allianz Goal Assure plan.

Even more, interestingly enough, ELSS mutual funds do not have any hidden charges.

Greater transparency in cost structure is one reason many investors prefer combining term insurance with mutual fund investments instead of bundled insurance products.

Hence, the return you see is what you get.

In contrast, the net returns from Bajaj Allianz Life Goal Assure may vary after deducting policy administration charges, mortality charges, and fund management expenses.

Additionally, ELSS mutual funds have a lock-in period of only 3 years.

Whereas, Bajaj Allianz Life Goal Assure has a lock-in period of 5 years.

ELSS mutual funds have the same tax benefit as the Bajaj Allianz Goal Assure u/s 80C. Investments up to ₹1.5 lakh per annum are exempt from income tax.

However, the returns from the ELSS mutual funds are not entirely tax-free.

Even if the investment is below ₹1.5 lakhs per annum. And the capital gains are taxed at 10% for the long-term gains.

Should this make a difference to an investor?

Let’s find out!

Capital Gains on your ELSS investment are tax-exempt to the limit of ₹1.25 Lakh in a financial year.

Capital Gains over and above ₹1.25 Lakh are taxed at 12.5%.

The table below shows the post-tax return from the ELSS mutual fund investment.

|

ELSS Tax Calculation |

|

|

Maturity value after 15 years |

15,82,961 |

|

Purchase price |

4,57,000 |

|

Long-Term Capital Gains |

11,25,961 |

|

Exemption limit |

1,25,000 |

|

Taxable LTCG |

10,00,961 |

|

Tax paid on LTCG |

1,25,120 |

|

Maturity value after tax |

14,57,841 |

In the above illustration, the Post Tax Return of ELSS Mutual Fund is calculated at ₹14.57 lakhs.

Even with LTCG tax @ 12.5%, ELSS mutual funds deliver a far higher return than the Bajaj Allianz Goal Assure policy—₹9.56 lakhs more return. And the risk involved is the same as the policy.

And to be fair, with the implementation of ‘The Finance Act 2021’, the tax treatment of ULIP plans and ELSS Mutual Funds are not much different from each other.

It is explained above under the Taxation of Bajaj Allianz Goal Assure

The fact is very clear now. Almost all of the time, ULIP policies are affecting your investment portfolio, instead of helping it.

- Bajaj Allianz Life Goal Assures vs Bajaj Allianz Life Long-life Goal Plan

‘Life Goal Assures’ is a ULIP that has 8 different fund options whereas ‘Long-life Goal’ is a Non-participating, Life, Individual, Whole Life, Unit-Linked, Regular Premium Payment, and Endowment plan which has 10 different fund options.

Comparing the Bajaj Allianz Life Long Life Goal brochure and the Bajaj Allianz Life Goal Assure brochure can help investors understand the difference in policy design and investment approach.

Click below to read the complete review of this ‘Long-life Goal’ with illustrations and precise calculations.

Bajaj Allianz Life Long-life Goal Plan Review: Is It Good or Bad?

- Bajaj Allianz Life Goal Assures vs Bajaj Allianz Life Assured Wealth Goal

‘Goal Assures’ is a ULIP plan whereas ‘Assured Wealth Goal’ is a non-linked, individual life insurance, savings plan.

While Bajaj Allianz Life Goal Assure focuses on market-linked wealth accumulation, Bajaj Allianz Life Assured Wealth Goal emphasizes structured savings and income benefits.

In ‘Life Assured Wealth Goal’, Lifetime income, second income, step-up income, additional income, and wealth development are the five variations.

Bajaj Allianz Life Assured Wealth Goal-An Insightful Review (2023)-Good or Bad?

- Bajaj Allianz Life Goal Assures Vs Other Investment Options – Review Conclusion

As we discussed earlier.

“PPF investments come with a guaranteed return that is completely tax-free. On the other hand, the return you will receive from your Bajaj Allianz Life Goal Assure policy is not guaranteed”.

“Even with the LTCG tax at 12.5%, ELSS mutual funds outperform the Bajaj Allianz Goal Assure policy by a factor of 13 lacs. Additionally, the risk is identical to the policy”.

After a thorough and detailed analysis of other alternative options for Bajaj Allianz Life Goal Assures, it is clear that Term Insurance + PPF or ELSS seem to be far more feasible investment options.

A comprehensive comparison of returns, charges, taxation, and flexibility can help investors identify the investment option best suited to their financial objectives.

10.) Who Should Consider Bajaj Allianz Life Goal Assure?

Bajaj Allianz Life Goal Assure may be suitable for investors who are comfortable with market-linked investments and are looking for the dual benefit of life insurance protection and long-term wealth creation through a ULIP.

It can also appeal to individuals with long investment horizons who are willing to stay invested through market fluctuations to maximize the power of compounding.

However, investors seeking guaranteed returns or complete capital protection should carefully evaluate the policy features, fund options, charges, and flexibility before investing.

Comparing the plan with mutual funds combined with term insurance can also help determine whether it aligns with individual financial goals and risk appetite.

The plan may also appeal to investors looking for a Bajaj Allianz life goal policy that combines insurance protection with the opportunity to participate in equity markets over the long term.

So, what is the verdict?

11.) Verdict Bajaj Allianz Life Goal PlanVerdict: Good or Bad?

Do not go for the Bajaj Allianz Life Goal Assure policy.

There is no guarantee of the amount of maturity benefit that you will get. It is to compensate those who pay high premiums for the disappointment of earning a less-than-expected maturity benefit that the policy offers a fund booster.

If your risk tolerance is low, you can get guaranteed and probably higher returns by investing in a mix of PPF and term life insurance.

If you have higher risk tolerance you can get a much higher return by investing in a mix of term life insurance and ELSS.

12.) How to Surrender your Bajaj Allianz Life Goal Assure Policy? An Analysis

To surrender your Bajaj Allianz Goal, Assure, you can directly contact any branch of Bajaj Allianz Life.

You may also call their customer service at 1-800-209-7272 (Toll-Free). Or you can send an email to customercare@bajajallianz.co.in with your query.

Before initiating a surrender request, policyholders should review the applicable surrender value, lock-in conditions, and tax implications mentioned in the policy document.

During the Free-look period: Analysis

- If you have just bought the policy, you have the 15-day free-look period—since the date of purchase—to surrender your policy.

- Submit a surrender request with the original policy documents at any branch of Bajaj Allianz Life.

- On surrendering your policy, your life cover will cease and you will receive your premium back minus any underwriting charges.

- The free-look period is 30 days if you bought the policy online or over telemarketing.

After the Free-look period: Analysis

- After the free-look period, you can surrender your Bajaj Allianz Goal Assure plan only after the completion of 5-year lock-in period.

- On surrendering, you will receive your fund value in the policy as of the surrender date.

- If you submit a surrender request during the lock-in period, your policy will become a paid-up policy.

- Your investments will be moved to the discontinued policy fund—earning a 4% return.

Here is a Cheat Sheet to Select the Best Term Insurance Plan.

13.)Conclusion:

You aim to achieve your financial goals—it’s not about who is paying the least amount of tax.

Long-term wealth creation depends on selecting investment products that balance returns, costs, liquidity, and risk according to individual financial goals.

The only edge ULIPs, like the Bajaj Allianz Goal Assure, had was severely reduced by the Finance Act 2021. And you know that ELSS mutual funds deliver far better post-tax returns.

But have you ever wondered why insurance agents try to sell you this plan? because like many policies in the bazaar, they get paid a high agent commission for selling you this plan, as simple as that.

Get insured with a term insurance plan, assess your risk tolerance, and invest accordingly. You can achieve your financial goals faster than you expect.

Separating insurance and investment decisions often provides greater flexibility and transparency while building a diversified financial portfolio.

Carefully reviewing the Bajaj Allianz Life Goal Assure brochure, policy charges, fund options, and expected returns can help investors make well-informed long-term investment decisions.

Do you think social media sites like Quora, Facebook, and Twitter can provide you with authentic information to plan your finances? A professional financial planner can do a far better job.

If you have any comments or questions, write them in the comment box below.

Or are you interested in creating a Comprehensive Financial Plan for your financial goals?

Skip the queue by registering for your 30-minute FREE Financial Plan Consultation. Click the ‘Register Now!’ button below.

The agents never discuss the hidden charges with customers. Moreover, hidden charges are not clearly mentioned in the policy in a manner that would be known to a layman. If this happens then no one will take the policy, this is what the policy sellers fear.

Give some idea about its past performance also.only by comparing its 8% return how we can judge because some time it may go beyond 8% and some time less than 8%.what is the average return till now of these policy. Either it is Hdfc click to wealth or Bajaj allianz life goal assure plan.

Please compare with its history also. And predict its future return also. It will be helpful to those people who are already customer of these plan.

Life Insurance policies usually project lower returns (~8%) because of higher fees and conservative growth strategies. In contrast, ELSS funds often target higher returns (~12%) due to their aggressive market exposure and lower expenses. Comparing them at equal returns can be misleading; ULIP NAVs are pre-expense and don’t reflect actual net gains. Mutual Funds provide better transparency and net returns by post-expenses NAV, making them more attractive for growth-focused investors.

Excellent article…well calculated comparisons between different investment avenues. This is the kind of article we need for making good investment decisions. Keep it up!